Energy

Nickel: The Secret Driver of the Battery Revolution

Nickel: The Secret Driver of the Battery Revolution

Commodity markets are being turned upside down by the EV revolution.

But while lithium and cobalt deservedly get a lot of the press, there is another metal that will also be changed forever by increasing penetration rates of EVs in the automobile market: nickel.

Today’s infographic comes to us from North American Nickel and it dives into nickel’s rapidly increasing role in lithium-ion battery chemistries, as well as interesting developments on the supply end of the spectrum.

Nickel’s Vital Role

Nickel’s role in lithium-ion batteries may still be underappreciated for now, but certainly one person familiar with the situation has been vocal about the metal’s importance.

Our cells should be called Nickel-Graphite, because primarily the cathode is nickel and the anode side is graphite with silicon oxide.

– Elon Musk, Tesla CEO and co-founder

Indeed, nickel is the most important metal by mass in the lithium-ion battery cathodes used by EV manufacturers – it makes up about 80% of an NCA cathode, and about one-third of NMC or LMO-NMC cathodes. More importantly, as battery formulations evolve, it’s expected that we’ll use more nickel, not less.

According to UBS, in their recent report on tearing down a Chevy Bolt, here is how NMC cathodes are expected to evolve:

| Cathode | Year | Nickel | Manganese | Cobalt |

|---|---|---|---|---|

| NMC | Present | 33% | 33% | 33% |

| NMC | 2018 | 60% | 20% | 20% |

| NMC | 2020 | 80% | 10% | 10% |

The end result? In time, nickel will make up 80% of the mass in both NCA and NMC cathodes, used by companies like Tesla and Chevrolet.

Impact on the Nickel Market

Nickel, which is primarily used for the production of stainless steel, is already one of the world’s most important metal markets at over $20 billion in size. For this reason, how much the nickel market is affected by battery demand depends largely on EV penetration.

EVs currently constitute about 1% of auto demand – this translates to 70,000 tonnes of nickel demand, about 3% of the total market. However, as EV penetration goes up, nickel demand increases rapidly as well.

A shift of just 10% of the global car fleet to EVs would create demand for 400,000 tonnes of nickel, in a 2 million tonne market. Glencore sees nickel shortage as EV demand burgeons.

– Ivan Glasenberg, Glencore CEO

The Supply Kicker

Even though much more nickel will be needed for lithium-ion batteries, there is an interesting wrinkle in that equation: most nickel in the global supply chain is not actually suited for battery production.

Today’s nickel supply comes from two very different types of deposits:

- Nickel Laterites: Low grade, bulk-tonnage deposits that make up 62.4% of current production.

- Nickel Sulfides: Higher grade, but rarer deposits that make up 37.5% of current production.

Many laterite deposits are used to produce nickel pig iron and ferronickel, which are cheap inputs to make Chinese stainless steel. Meanwhile, nickel sulfide deposits are used to make nickel metal as well as nickel sulfate. The latter salt, nickel sulfate, is what’s used primarily for electroplating and lithium-ion cathode material, and less than 10% of nickel supply is in sulfate form.

Not surprisingly, major mining companies see this as an opportunity. In August 2017, mining giant BHP Billiton announced it would invest $43.2 million to build the world’s biggest nickel sulfate plant in Australia.

But even investments like this may not be enough to capture rising demand for nickel sulfate.

Although the capacity to produce nickel sulfate is expanding rapidly, we cannot yet identify enough nickel sulfate capacity to feed the projected battery forecasts.

– Wood Mackenzie

Energy

Charted: 4 Reasons Why Lithium Could Be the Next Gold Rush

Visual Capitalist has partnered with EnergyX to show why drops in prices and growing demand may make now the right time to invest in lithium.

4 Reasons Why You Should Invest in Lithium

Lithium’s importance in powering EVs makes it a linchpin of the clean energy transition and one of the world’s most precious minerals.

In this graphic, Visual Capitalist partnered with EnergyX to explore why now may be the time to invest in lithium.

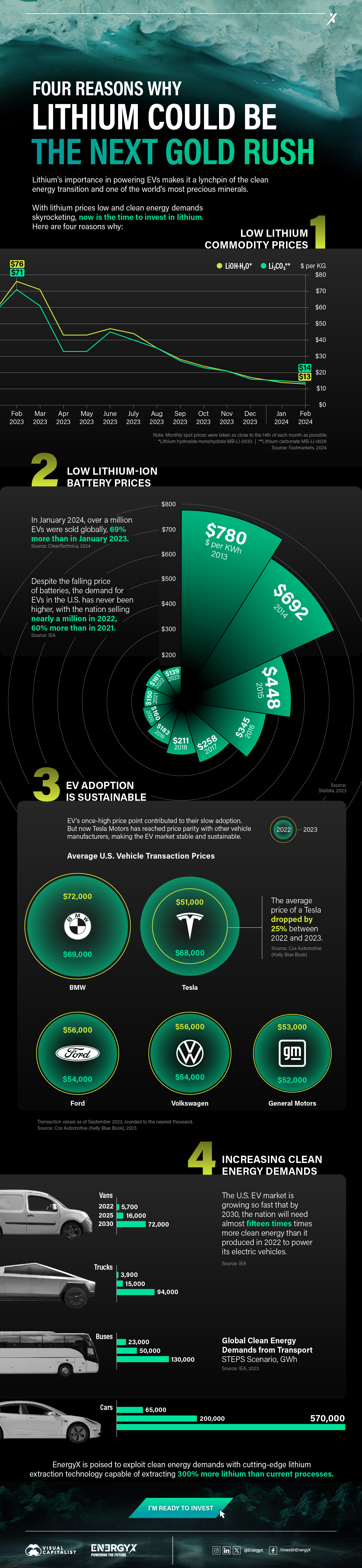

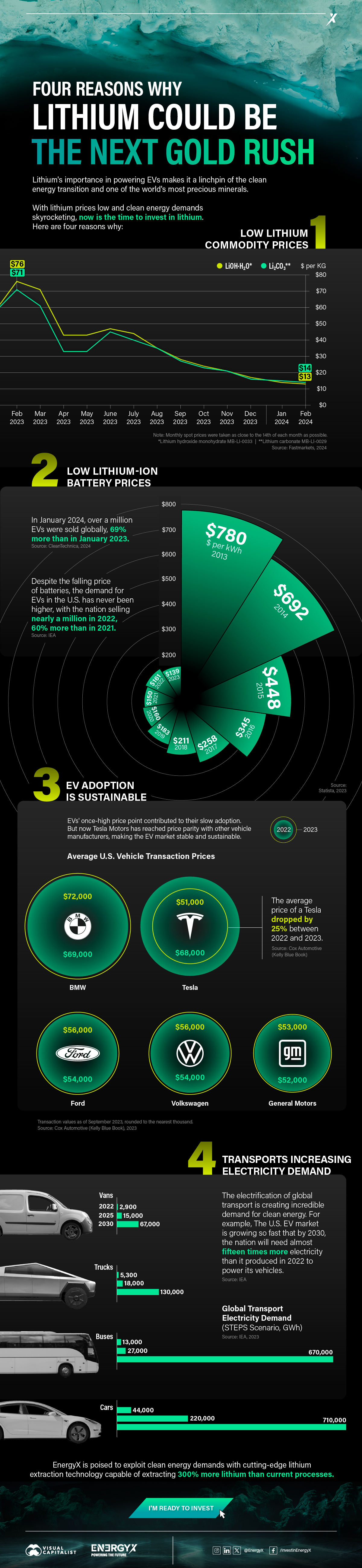

1. Lithium Prices Have Dropped

One of the most critical aspects of evaluating an investment is ensuring that the asset’s value is higher than its price would indicate. Lithium is integral to powering EVs, and, prices have fallen fast over the last year:

| Date | LiOH·H₂O* | Li₂CO₃** |

|---|---|---|

| Feb 2023 | $76 | $71 |

| March 2023 | $71 | $61 |

| Apr 2023 | $43 | $33 |

| May 2023 | $43 | $33 |

| June 2023 | $47 | $45 |

| July 2023 | $44 | $40 |

| Aug 2023 | $35 | $35 |

| Sept 2023 | $28 | $27 |

| Oct 2023 | $24 | $23 |

| Nov 2023 | $21 | $21 |

| Dec 2023 | $17 | $16 |

| Jan 2024 | $14 | $15 |

| Feb 2024 | $13 | $14 |

Note: Monthly spot prices were taken as close to the 14th of each month as possible.

*Lithium hydroxide monohydrate MB-LI-0033

**Lithium carbonate MB-LI-0029

2. Lithium-Ion Battery Prices Are Also Falling

The drop in lithium prices is just one reason to invest in the metal. Increasing economies of scale, coupled with low commodity prices, have caused the cost of lithium-ion batteries to drop significantly as well.

In fact, BNEF reports that between 2013 and 2023, the price of a Li-ion battery dropped by 82%.

| Year | Price per KWh |

|---|---|

| 2023 | $139 |

| 2022 | $161 |

| 2021 | $150 |

| 2020 | $160 |

| 2019 | $183 |

| 2018 | $211 |

| 2017 | $258 |

| 2016 | $345 |

| 2015 | $448 |

| 2014 | $692 |

| 2013 | $780 |

3. EV Adoption is Sustainable

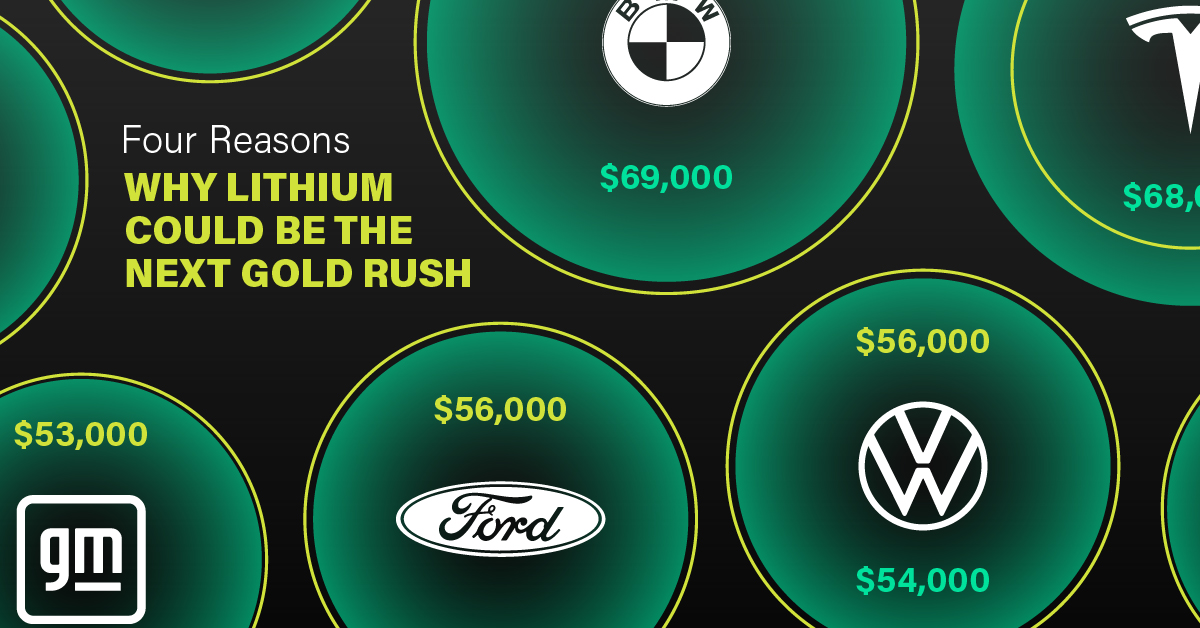

One of the best reasons to invest in lithium is that EVs, one of the main drivers behind the demand for lithium, have reached a price point similar to that of traditional vehicle.

According to the Kelly Blue Book, Tesla’s average transaction price dropped by 25% between 2022 and 2023, bringing it in line with many other major manufacturers and showing that EVs are a realistic transport option from a consumer price perspective.

| Manufacturer | September 2022 | September 2023 |

|---|---|---|

| BMW | $69,000 | $72,000 |

| Ford | $54,000 | $56,000 |

| Volkswagon | $54,000 | $56,000 |

| General Motors | $52,000 | $53,000 |

| Tesla | $68,000 | $51,000 |

4. Electricity Demand in Transport is Growing

As EVs become an accessible transport option, there’s an investment opportunity in lithium. But possibly the best reason to invest in lithium is that the IEA reports global demand for the electricity in transport could grow dramatically by 2030:

| Transport Type | 2022 | 2025 | 2030 |

|---|---|---|---|

| Buses 🚌 | 23,000 GWh | 50,000 GWh | 130,000 GWh |

| Cars 🚙 | 65,000 GWh | 200,000 GWh | 570,000 GWh |

| Trucks 🛻 | 4,000 GWh | 15,000 GWh | 94,000 GWh |

| Vans 🚐 | 6,000 GWh | 16,000 GWh | 72,000 GWh |

The Lithium Investment Opportunity

Lithium presents a potentially classic investment opportunity. Lithium and battery prices have dropped significantly, and recently, EVs have reached a price point similar to other vehicles. By 2030, the demand for clean energy, especially in transport, will grow dramatically.

With prices dropping and demand skyrocketing, now is the time to invest in lithium.

EnergyX is poised to exploit lithium demand with cutting-edge lithium extraction technology capable of extracting 300% more lithium than current processes.

-

Lithium4 days ago

Lithium4 days agoRanked: The Top 10 EV Battery Manufacturers in 2023

Asia dominates this ranking of the world’s largest EV battery manufacturers in 2023.

-

Energy1 week ago

Energy1 week agoThe World’s Biggest Nuclear Energy Producers

China has grown its nuclear capacity over the last decade, now ranking second on the list of top nuclear energy producers.

-

Energy1 month ago

Energy1 month agoThe World’s Biggest Oil Producers in 2023

Just three countries accounted for 40% of global oil production last year.

-

Energy1 month ago

Energy1 month agoHow Much Does the U.S. Depend on Russian Uranium?

Currently, Russia is the largest foreign supplier of nuclear power fuel to the U.S.

-

Uranium2 months ago

Uranium2 months agoCharted: Global Uranium Reserves, by Country

We visualize the distribution of the world’s uranium reserves by country, with 3 countries accounting for more than half of total reserves.

-

Energy3 months ago

Energy3 months agoVisualizing the Rise of the U.S. as Top Crude Oil Producer

Over the last decade, the United States has established itself as the world’s top producer of crude oil, surpassing Saudi Arabia and Russia.

-

Energy1 week ago

The World’s Biggest Nuclear Energy Producers

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

Technology2 weeks ago

Technology2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Countries2 weeks ago

Countries2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries

-

United States2 weeks ago

United States2 weeks agoWhere U.S. Inflation Hit the Hardest in March 2024