Markets

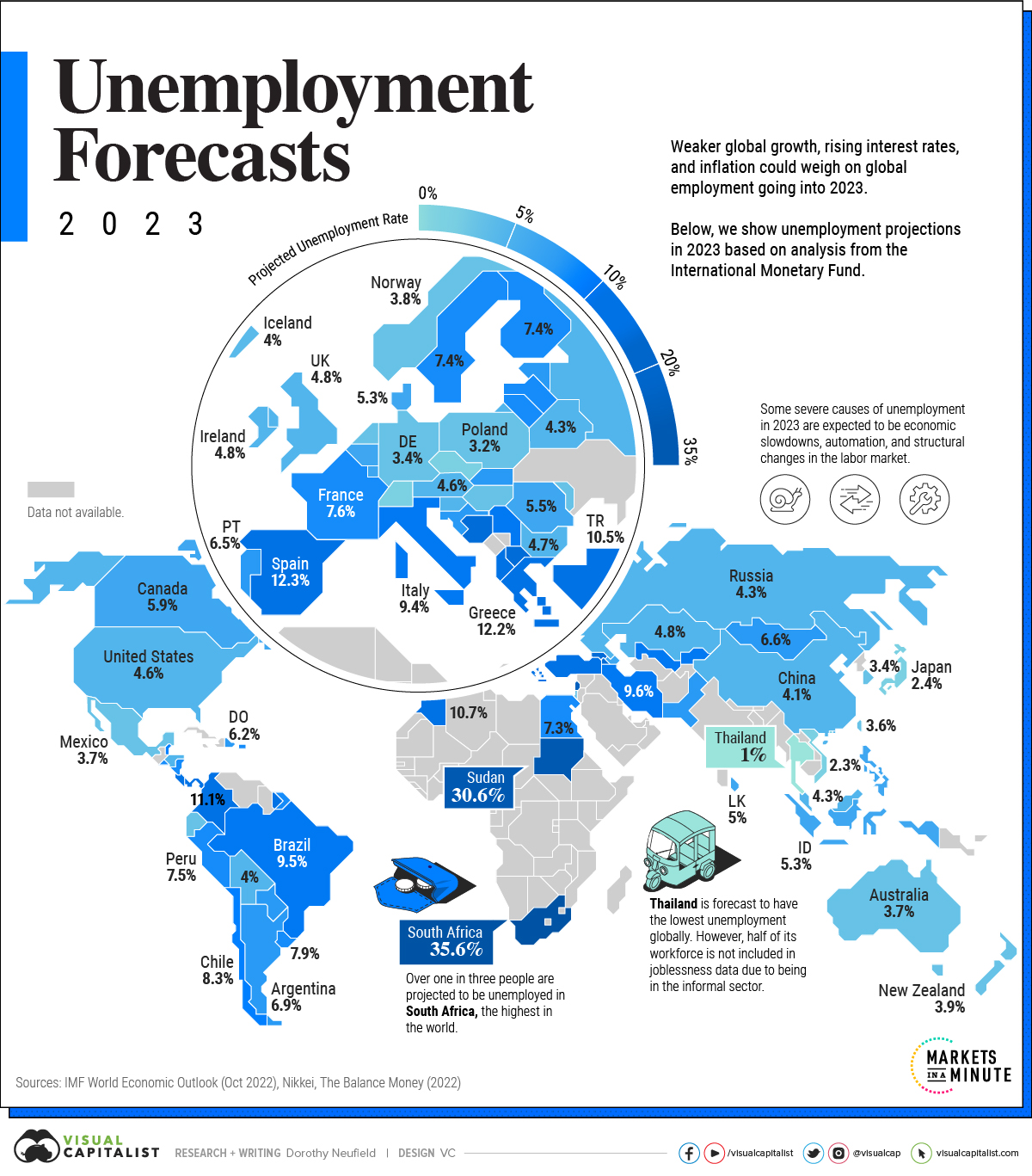

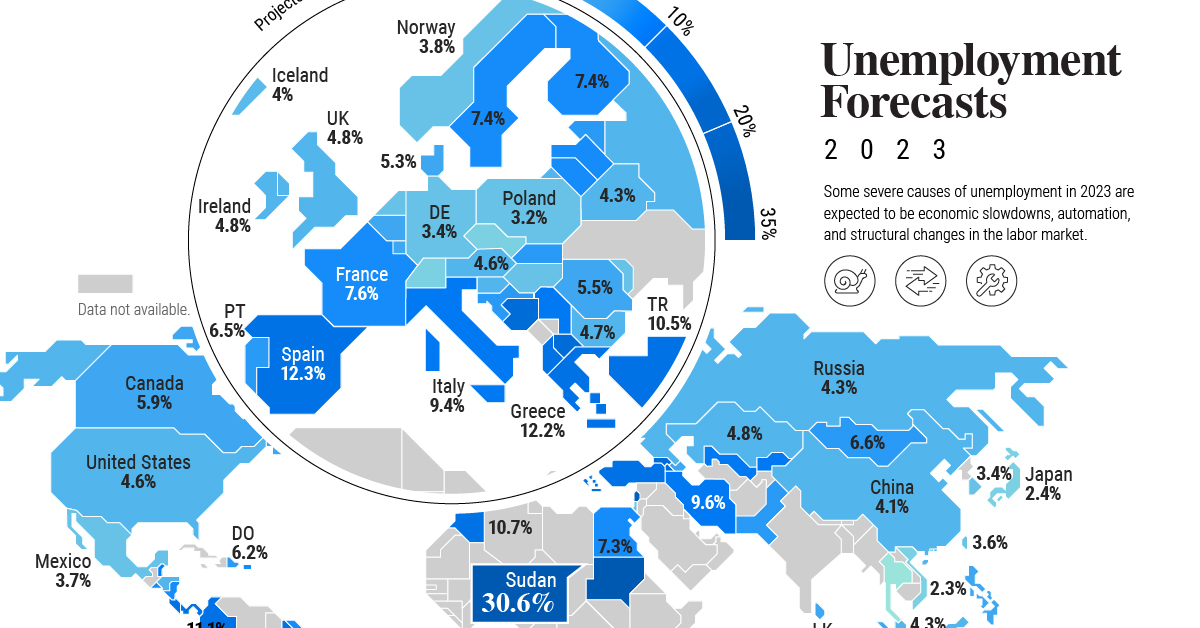

Mapped: Unemployment Forecasts, by Country in 2023

Mapped: Unemployment Forecasts, by Country in 2023

This was originally posted on Advisor Channel. Sign up to the free mailing list to get beautiful visualizations on financial markets that help advisors and their clients.

As 2022 clearly illustrated, the global job market can surprise expectations.

So far, this year is no different. The unemployment rate in six of the G7 countries hovers near the lowest in a century. With an unemployment rate of 3.4%, the U.S. jobless rate hasn’t fallen this low since 1969.

But as some economies navigate a strong labor market against high inflation and hawkish monetary policy, others are facing more challenging conditions. In the above graphic, we map unemployment forecasts in 2023 using data from the IMF’s World Economic Outlook.

Uncertainty Clouds the Surface

Across many countries, the pandemic has made entrenched labor trends worse. It has also altered job market conditions.

South Africa is projected to see the highest jobless rate globally. As the most industrialized nation on the continent, unemployment is estimated to hit 35.6% in 2023. Together, slow economic growth and stringent labor laws have prevented firms from hiring workers. Over the last two decades, unemployment has hovered around 20%.

| Country / Region | 2023 Unemployment Rate(Projected) |

|---|---|

| 🇿🇦 South Africa | 35.6% |

| 🇸🇩 Sudan | 30.6% |

| 🇵🇸 West Bank and Gaza | 25.0% |

| 🇬🇪 Georgia | 19.5% |

| 🇧🇦 Bosnia and Herzegovina | 17.2% |

| 🇦🇲 Armenia | 15.1% |

| 🇲🇰 North Macedonia | 15.0% |

| 🇨🇷 Costa Rica | 13.2% |

| 🇧🇸 The Bahamas | 12.7% |

| 🇪🇸 Spain | 12.3% |

| 🇬🇷 Greece | 12.2% |

| 🇨🇴 Colombia | 11.1% |

| 🇲🇦 Morocco | 10.7% |

| 🇸🇷 Suriname | 10.6% |

| 🇹🇷 Turkiye | 10.5% |

| 🇧🇧 Barbados | 10.0% |

| 🇦🇱 Albania | 10.0% |

| 🇵🇦 Panama | 10.0% |

| 🇷🇸 Serbia | 9.7% |

| 🇮🇷 Iran | 9.6% |

| 🇺🇿 Uzbekistan | 9.5% |

| 🇧🇷 Brazil | 9.5% |

| 🇮🇹 Italy | 9.4% |

| 🇰🇬 Kyrgyz Republic | 9.0% |

| 🇨🇻 Cabo Verde | 8.5% |

| 🇨🇱 Chile | 8.3% |

| 🇧🇿 Belize | 8.0% |

| 🇵🇷 Puerto Rico | 7.9% |

| 🇺🇾 Uruguay | 7.9% |

| 🇦🇼 Aruba | 7.7% |

| 🇫🇷 France | 7.6% |

| 🇵🇪 Peru | 7.5% |

| 🇸🇻 El Salvador | 7.5% |

| 🇸🇪 Sweden | 7.4% |

| 🇫🇮 Finland | 7.4% |

| 🇲🇺 Mauritius | 7.4% |

| 🇪🇬 Egypt | 7.3% |

| 🇱🇻 Latvia | 7.2% |

| 🇳🇮 Nicaragua | 7.2% |

| 🇱🇹 Lithuania | 7.0% |

| 🇦🇷 Argentina | 6.9% |

| 🇪🇪 Estonia | 6.8% |

| 🇧🇳 Brunei Darussalam | 6.8% |

| 🇲🇳 Mongolia | 6.6% |

| 🇭🇷 Croatia | 6.6% |

| 🇨🇾 Cyprus | 6.5% |

| 🇵🇹 Portugal | 6.5% |

| 🇵🇰 Pakistan | 6.4% |

| 🇵🇾 Paraguay | 6.4% |

| 🇸🇰 Slovak Republic | 6.2% |

| 🇩🇴 Dominican Republic | 6.2% |

| 🇨🇦 Canada | 5.9% |

| 🇦🇿 Azerbaijan | 5.8% |

| 🇸🇲 San Marino | 5.7% |

| 🇧🇪 Belgium | 5.6% |

| 🇷🇴 Romania | 5.5% |

| 🇫🇯 Fiji | 5.5% |

| 🇵🇭 Philippines | 5.4% |

| 🇮🇩 Indonesia | 5.3% |

| 🇩🇰 Denmark | 5.3% |

| 🇱🇰 Sri Lanka | 5.0% |

| 🇱🇺 Luxembourg | 5.0% |

| 🇮🇪 Ireland | 4.8% |

| 🇰🇿 Kazakhstan | 4.8% |

| 🇬🇧 United Kingdom | 4.8% |

| 🇧🇬 Bulgaria | 4.7% |

| 🇦🇹 Austria | 4.6% |

| 🇭🇳 Honduras | 4.6% |

| 🇺🇸 U.S. | 4.6% |

| 🇧🇭 Bahrain | 4.4% |

| 🇷🇺 Russia | 4.3% |

| 🇧🇾 Belarus | 4.3% |

| 🇸🇮 Slovenia | 4.3% |

| 🇲🇾 Malaysia | 4.3% |

| 🇨🇳 China | 4.1% |

| 🇮🇸 Iceland | 4.0% |

| 🇧🇴 Bolivia | 4.0% |

| 🇭🇰 Hong Kong SAR | 4.0% |

| 🇳🇱 Netherlands | 3.9% |

| 🇳🇿 New Zealand | 3.9% |

| 🇭🇺 Hungary | 3.8% |

| 🇳🇴 Norway | 3.8% |

| 🇮🇱 Israel | 3.8% |

| 🇪🇨 Ecuador | 3.8% |

| 🇦🇺 Australia | 3.7% |

| 🇲🇽 Mexico | 3.7% |

| 🇹🇼 Taiwan | 3.6% |

| 🇲🇩 Moldova | 3.5% |

| 🇰🇷 South Korea | 3.4% |

| 🇩🇪 Germany | 3.4% |

| 🇲🇹 Malta | 3.3% |

| 🇵🇱 Poland | 3.2% |

| 🇸🇨 Seychelles | 3.0% |

| 🇲🇴 Macao SAR | 2.7% |

| 🇯🇵 Japan | 2.4% |

| 🇨🇭 Switzerland | 2.4% |

| 🇻🇳 Vietnam | 2.3% |

| 🇨🇿 Czech Republic | 2.3% |

| 🇸🇬 Singapore | 2.1% |

| 🇹🇭 Thailand | 1.0% |

In Europe, Bosnia and Herzegovina is estimated to see the highest unemployment rate, at over 17%. It is followed by North Macedonia (15.0%) and Spain (12.7%). These jobless rates are more than double the projections for advanced economies in Europe.

The U.S. is forecast to see an unemployment rate of 4.6%, or 1.2% higher than current levels.

This suggests that today’s labor market strength will ease as U.S. economic indicators weaken. One marker is the Conference Board’s Leading Economic Index, which fell for its tenth straight month in December. Lower manufacturing orders, declining consumer expectations, and shorter work weeks are among the indicators it tracks.

Like the U.S., many advanced countries are witnessing labor market strength, especially in the United Kingdom, Asia, and Europe, although how long it will last is unknown.

A Closer Look at U.S. Numbers

Unlike some declining economic indicators mentioned above, the job market is one of the strongest areas of the global economy. Even as the tech sector reports mass layoffs, unemployment claims in the U.S. fall below recent averages. (It’s worth noting the tech sector makes up just 4% of the workforce).

In 2022, 4.8 million jobs were added, more than double the average seen between 2015-2019. Of course, the pandemic recovery has impacted these figures.

Some analysts suggest that despite a bleaker economic outlook, companies are hesitant to conduct layoffs. At the same time, the labor market is absorbing workers who have lost employment.

Consider the manufacturing sector. Even as the January ISM Purchasing Managers Index posted lower readings, hitting 47.4—a level of 48.7 and below generally indicates a recession—factories are not laying off many workers. Instead, manufacturers are saying they are confident conditions will improve in the second half of the year.

Containing Aftershocks

Today, strong labor markets pose a key challenge for central bankers globally.

This is because the robust job market is contributing to high inflation numbers. Yet despite recent rate increases, the impact has yet to prompt major waves in unemployment. Typically, monetary policy moves like these takes about a year to take peak effect. To combat inflation, monetary policy has been shown to take over three or even four years.

The good news is that inflation can potentially be tamed by other means. Fixing supply-side dynamics, such as preventing supply shortages and improving transportation systems and infrastructure could cool inflation.

As investors closely watch economic data, rising unemployment could come on the heels of higher interest rates, but so far this has yet to unravel.

Markets

The European Stock Market: Attractive Valuations Offer Opportunities

On average, the European stock market has valuations that are nearly 50% lower than U.S. valuations. But how can you access the market?

European Stock Market: Attractive Valuations Offer Opportunities

Europe is known for some established brands, from L’Oréal to Louis Vuitton. However, the European stock market offers additional opportunities that may be lesser known.

The above infographic, sponsored by STOXX, outlines why investors may want to consider European stocks.

Attractive Valuations

Compared to most North American and Asian markets, European stocks offer lower or comparable valuations.

| Index | Price-to-Earnings Ratio | Price-to-Book Ratio |

|---|---|---|

| EURO STOXX 50 | 14.9 | 2.2 |

| STOXX Europe 600 | 14.4 | 2 |

| U.S. | 25.9 | 4.7 |

| Canada | 16.1 | 1.8 |

| Japan | 15.4 | 1.6 |

| Asia Pacific ex. China | 17.1 | 1.8 |

Data as of February 29, 2024. See graphic for full index names. Ratios based on trailing 12 month financials. The price to earnings ratio excludes companies with negative earnings.

On average, European valuations are nearly 50% lower than U.S. valuations, potentially offering an affordable entry point for investors.

Research also shows that lower price ratios have historically led to higher long-term returns.

Market Movements Not Closely Connected

Over the last decade, the European stock market had low-to-moderate correlation with North American and Asian equities.

The below chart shows correlations from February 2014 to February 2024. A value closer to zero indicates low correlation, while a value of one would indicate that two regions are moving in perfect unison.

| EURO STOXX 50 | STOXX EUROPE 600 | U.S. | Canada | Japan | Asia Pacific ex. China |

|

|---|---|---|---|---|---|---|

| EURO STOXX 50 | 1.00 | 0.97 | 0.55 | 0.67 | 0.24 | 0.43 |

| STOXX EUROPE 600 | 1.00 | 0.56 | 0.71 | 0.28 | 0.48 | |

| U.S. | 1.00 | 0.73 | 0.12 | 0.25 | ||

| Canada | 1.00 | 0.22 | 0.40 | |||

| Japan | 1.00 | 0.88 | ||||

| Asia Pacific ex. China | 1.00 |

Data is based on daily USD returns.

European equities had relatively independent market movements from North American and Asian markets. One contributing factor could be the differing sector weights in each market. For instance, technology makes up a quarter of the U.S. market, but health care and industrials dominate the broader European market.

Ultimately, European equities can enhance portfolio diversification and have the potential to mitigate risk for investors.

Tracking the Market

For investors interested in European equities, STOXX offers a variety of flagship indices:

| Index | Description | Market Cap |

|---|---|---|

| STOXX Europe 600 | Pan-regional, broad market | €10.5T |

| STOXX Developed Europe | Pan-regional, broad-market | €9.9T |

| STOXX Europe 600 ESG-X | Pan-regional, broad market, sustainability focus | €9.7T |

| STOXX Europe 50 | Pan-regional, blue-chip | €5.1T |

| EURO STOXX 50 | Eurozone, blue-chip | €3.5T |

Data is as of February 29, 2024. Market cap is free float, which represents the shares that are readily available for public trading on stock exchanges.

The EURO STOXX 50 tracks the Eurozone’s biggest and most traded companies. It also underlies one of the world’s largest ranges of ETFs and mutual funds. As of November 2023, there were €27.3 billion in ETFs and €23.5B in mutual fund assets under management tracking the index.

“For the past 25 years, the EURO STOXX 50 has served as an accurate, reliable and tradable representation of the Eurozone equity market.”

— Axel Lomholt, General Manager at STOXX

Partnering with STOXX to Track the European Stock Market

Are you interested in European equities? STOXX can be a valuable partner:

- Comprehensive, liquid and investable ecosystem

- European heritage, global reach

- Highly sophisticated customization capabilities

- Open architecture approach to using data

- Close partnerships with clients

- Part of ISS STOXX and Deutsche Börse Group

With a full suite of indices, STOXX can help you benchmark against the European stock market.

Learn how STOXX’s European indices offer liquid and effective market access.

-

Economy2 days ago

Economy2 days agoEconomic Growth Forecasts for G7 and BRICS Countries in 2024

The IMF has released its economic growth forecasts for 2024. How do the G7 and BRICS countries compare?

-

Markets1 week ago

Markets1 week agoU.S. Debt Interest Payments Reach $1 Trillion

U.S. debt interest payments have surged past the $1 trillion dollar mark, amid high interest rates and an ever-expanding debt burden.

-

United States2 weeks ago

United States2 weeks agoRanked: The Largest U.S. Corporations by Number of Employees

We visualized the top U.S. companies by employees, revealing the massive scale of retailers like Walmart, Target, and Home Depot.

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

This graphic shows the states with the highest real GDP growth rate in 2023, largely propelled by the oil and gas boom.

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

In this graphic, we show the highest earning flight routes globally as air travel continued to rebound in 2023.

-

Markets3 weeks ago

Markets3 weeks agoRanked: The Most Valuable Housing Markets in America

The U.S. residential real estate market is worth a staggering $47.5 trillion. Here are the most valuable housing markets in the country.

-

Education1 week ago

Education1 week agoHow Hard Is It to Get Into an Ivy League School?

-

Technology2 weeks ago

Technology2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Ranked: The World’s Top Flight Routes, by Revenue

-

Demographics2 weeks ago

Demographics2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

The Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries

-

Economy2 weeks ago

Economy2 weeks agoWhere U.S. Inflation Hit the Hardest in March 2024

-

Green2 weeks ago

Green2 weeks agoTop Countries By Forest Growth Since 2001