Agriculture

Our Impact on Climate Change and Global Land Use in 5 Charts

Our Impact on Climate Change and Land Use in 5 Charts

As the world population approaches the eight billion mark, it’s becoming clear that we’re impacting the planet in unprecedented ways.

Humans have made such dramatic changes to Earth’s systems, from climate to geology, that many are suggesting we’ve entered into a new epoch – the Anthropocene.

To better understand the challenges of this era of wide-sweeping human impact on the planet, the Intergovernmental Panel on Climate Change (IPCC) has produced a massive report covering land use and climate change.

According to the IPCC, the situation is looking more dire by the year. Below are a few of the key insights buried within the 1,400+ pages of the massive report.

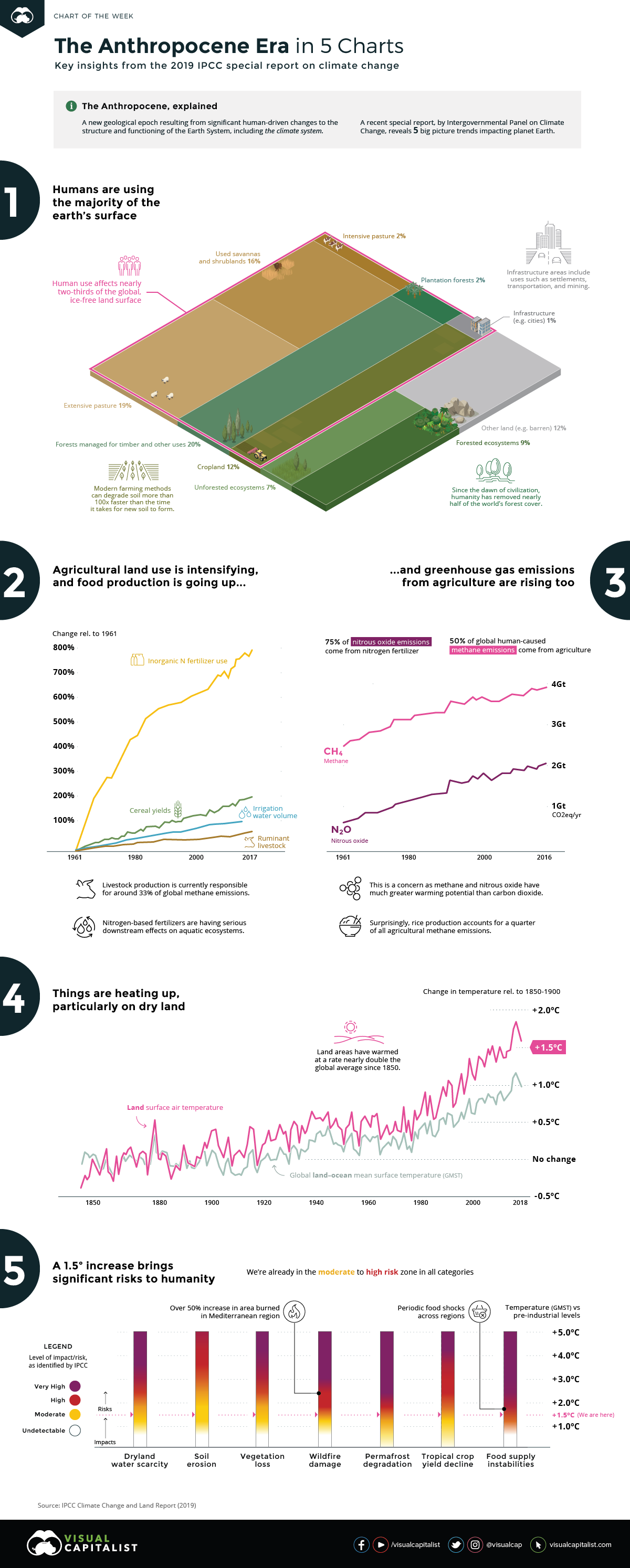

Shifting Global Land Use

The scale of land use and loss of biodiversity are unprecedented in human history.

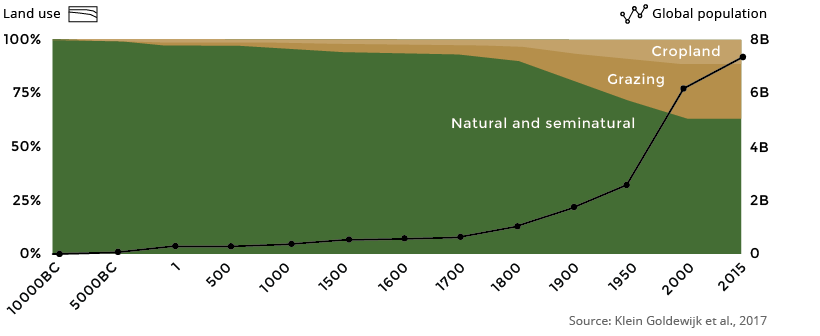

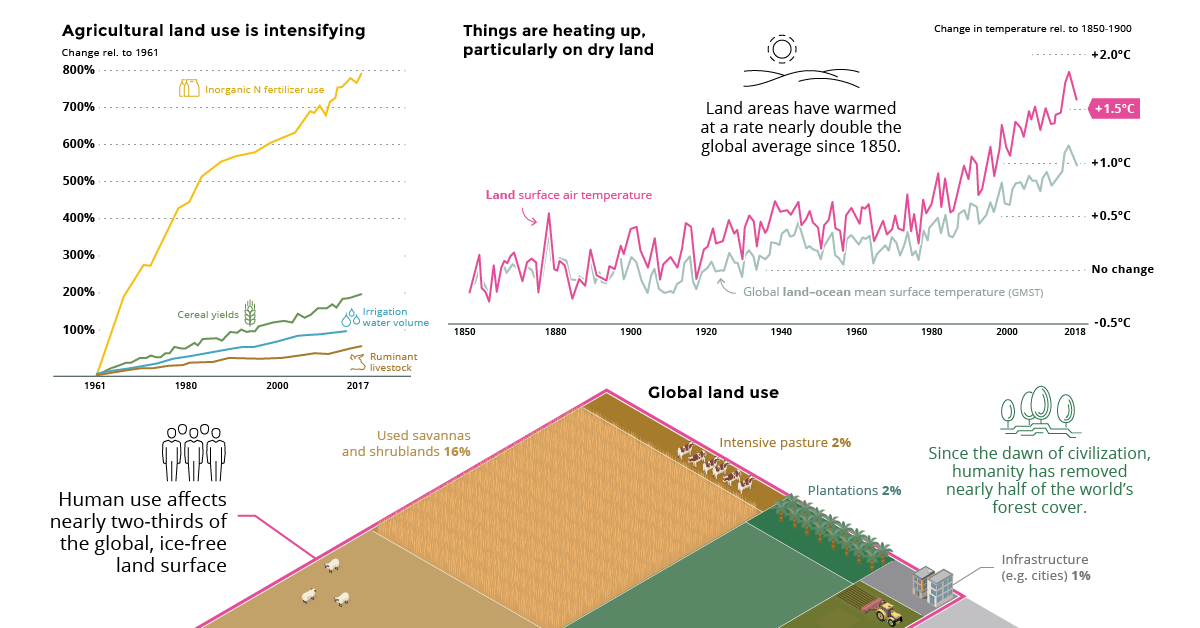

According to the report, roughly two-thirds of the world’s ice-free land is now devoted to human uses. Ecosystems, both forested and unforested, only account for about 16% of land today. Part of the reason for this dwindling supply of natural habitat is the rapid increase of agricultural activity around the world.

Since the dawn of the 20th century, global land use has shifted dramatically:

Not only has land use changed, but so has farming itself. In many parts of the world, increased yields will primarily come from existing agricultural land. For example, wheat yields are projected to increase 11% by the year 2026, despite the growing area only increasing by 1.8%. Rice production exhibits a similar trend, with 93% of the projected increase expected to come from increased yields rather than from area expansion. In some cases, intensive farming practices can degrade soil more than 100x faster than the time it takes for new soil to form, leaving fertilizers to pick up the slack.

One of the most dramatic changes highlighted in the report is the nearly eight-fold increase in the use of nitrogen-based fertilizers since the early 1960s. These types of fertilizers are having serious downstream effects on aquatic ecosystems, in some cases creating “dead zones” such as the one in the Gulf of Mexico.

In addition to the negative impacts outlined above, the simple act of feeding ourselves also accounts for one-third of our global greenhouse gas footprint.

Things are Heating Up

The past half-decade is likely to become the warmest five-year stretch in recorded history, underscoring the rapid pace of climate change. On a global scale, even a small increase in temperature can have a big impact on climate and our ecosystems.

For example, air can hold approximately 7% more moisture for every 1ºC increase, leading to an uptick in extreme rainfall events. These events can trigger landslides, increase the rate of soil erosion, and damage crops – just one example of how climate change can cause a chain reaction.

For the billions of people who live in “drylands”, climate change is serving up a completely different scenario:

“Heatwaves are projected to increase in frequency, intensity and duration in most parts of the world and drought frequency and intensity is projected to increase in some regions that are already drought prone.”

— IPCC report on Climate Change and Land, 2019

This is particularly worrisome as 90% of people in these arid or semiarid regions live in developing economies that are still very reliant on agriculture.

In addition to water scarcity, the IPCC has identified a number of other categories, including soil erosion and permafrost degradation. In all seven categories, our current global temperature puts us firmly in the moderate to high risk zone. These risks predict events with widespread societal impact, such as regional “food shocks” and millions of additional people exposed to wildfires.

This IPCC report makes one thing clear. In addition to tackling emissions in our cities and transportation networks, we’ll need to substantially change the way we use our land and rethink our entire agricultural system if we’re serious about mitigating the impact of climate change.

Agriculture

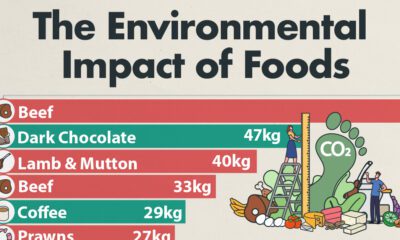

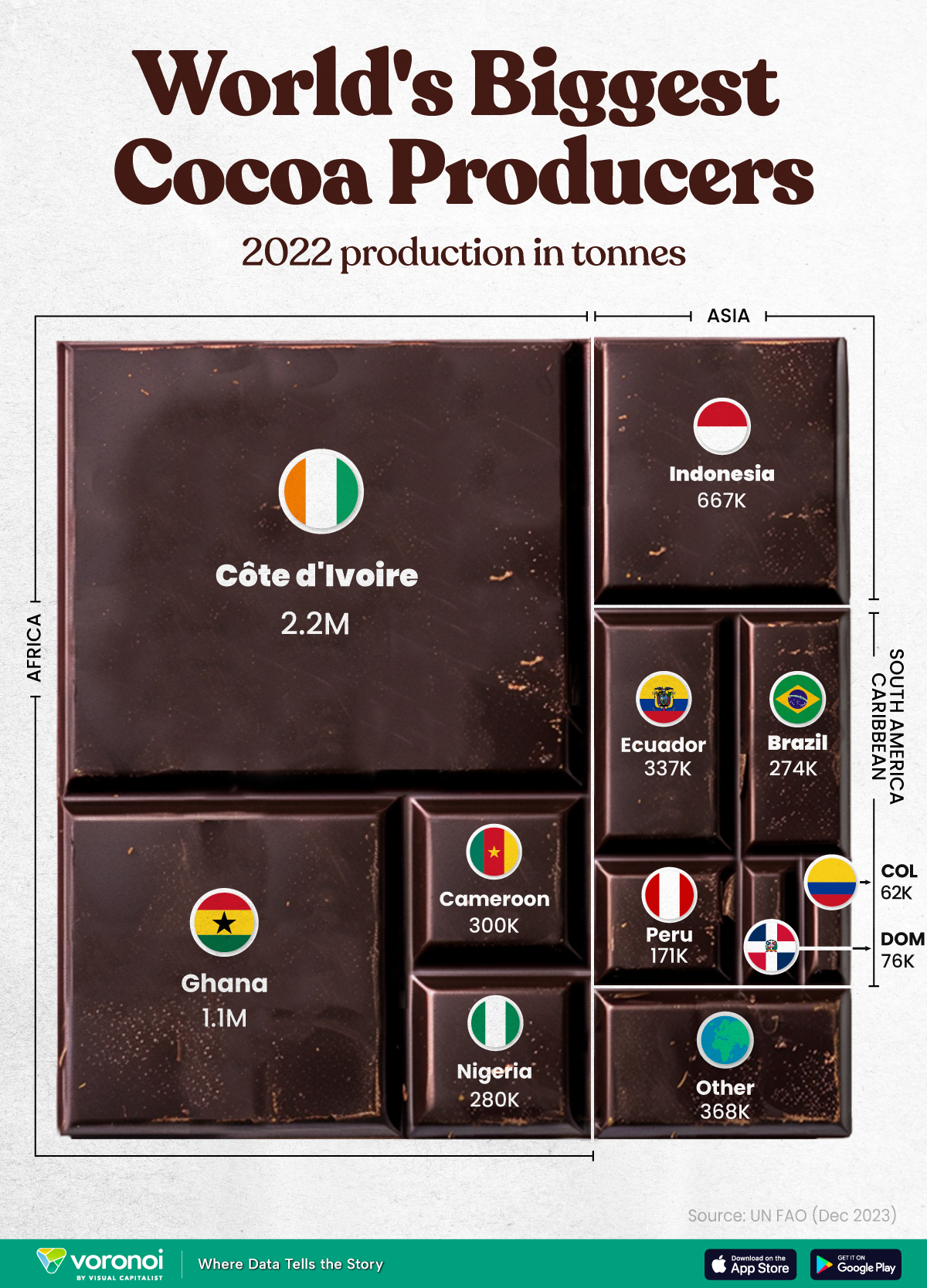

The World’s Top Cocoa Producing Countries

Here are the largest cocoa producing countries globally—from Côte d’Ivoire to Brazil—as cocoa prices hit record highs.

The World’s Top Cocoa Producing Countries

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

West Africa is home to the largest cocoa producing countries worldwide, with 3.9 million tonnes of production in 2022.

In fact, there are about one million farmers in Côte d’Ivoire supplying cocoa to key customers such as Nestlé, Mars, and Hershey. But the massive influence of this industry has led to significant forest loss to plant cocoa trees.

This graphic shows the leading producers of cocoa, based on data from the UN FAO.

Global Hotspots for Cocoa Production

Below, we break down the top cocoa producing countries as of 2022:

| Country | 2022 Production, Tonnes |

|---|---|

| 🇨🇮 Côte d'Ivoire | 2.2M |

| 🇬🇭 Ghana | 1.1M |

| 🇮🇩 Indonesia | 667K |

| 🇪🇨 Ecuador | 337K |

| 🇨🇲 Cameroon | 300K |

| 🇳🇬 Nigeria | 280K |

| 🇧🇷 Brazil | 274K |

| 🇵🇪 Peru | 171K |

| 🇩🇴 Dominican Republic | 76K |

| 🌍 Other | 386K |

With 2.2 million tonnes of cocoa in 2022, Côte d’Ivoire is the world’s largest producer, accounting for a third of the global total.

For many reasons, the cocoa trade in Côte d’Ivoire and Western Africa has been controversial. Often, farmers make about 5% of the retail price of a chocolate bar, and earn $1.20 each day. Adding to this, roughly a third of cocoa farms operate on forests that are meant to be protected.

As the third largest producer, Indonesia produced 667,000 tonnes of cocoa with the U.S., Malaysia, and Singapore as major importers. Overall, small-scale farmers produce 95% of cocoa in the country, but face several challenges such as low pay and unwanted impacts from climate change. Alongside aging trees in the country, these setbacks have led productivity to decline.

In South America, major producers include Ecuador and Brazil. In the early 1900s, Ecuador was the world’s largest cocoa producing country, however shifts in the global marketplace and crop disease led its position to fall. Today, the country is most known for its high-grade single-origin chocolate, with farms seen across the Amazon rainforest.

Altogether, global cocoa production reached 6.5 million tonnes, supported by strong demand. On average, the market has grown 3% annually over the last several decades.

-

Debt1 week ago

Debt1 week agoHow Debt-to-GDP Ratios Have Changed Since 2000

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Countries2 weeks ago

Countries2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries

-

United States2 weeks ago

United States2 weeks agoWhere U.S. Inflation Hit the Hardest in March 2024

-

Green2 weeks ago

Green2 weeks agoTop Countries By Forest Growth Since 2001

-

United States2 weeks ago

United States2 weeks agoRanked: The Largest U.S. Corporations by Number of Employees