Personal Finance

America’s Growing Financial Literacy Problem

America’s Growing Financial Literacy Problem

Making major personal finance decisions can be daunting for anyone.

Whether the decision is related to paying back student debt or how to invest for the first time, the outcomes of these decisions have a long-term impact on the quality of our lives. Smart decisions can lead to achieving financial independence, while bad decisions can lead to years of being stuck in the “hole”.

Even though it’s clear that financial literacy is important, there’s a big problem: it’s actually been dropping for years in the United States.

Diagnosing the Problem

Today’s infographic was done in conjunction with Next Gen Personal Finance, a non-profit that provides a free online curriculum of personal finance courses geared to students.

The graphic paints a troubling picture of the current financial literacy situation in the country, while demonstrating why personal finance is a crucial area of study for our youth.

Here are some of the indicators that show literacy is dropping:

- The U.S. ranks 14th globally in terms of financial literacy

- With a 57% literacy, the U.S. beats Botswana (52%) but gets edged out by countries like Germany (66%) or Canada (68%)

- Only 16.4% of U.S. students are required to take a personal finance class in schools

- 76% of millennials lack basic financial knowledge

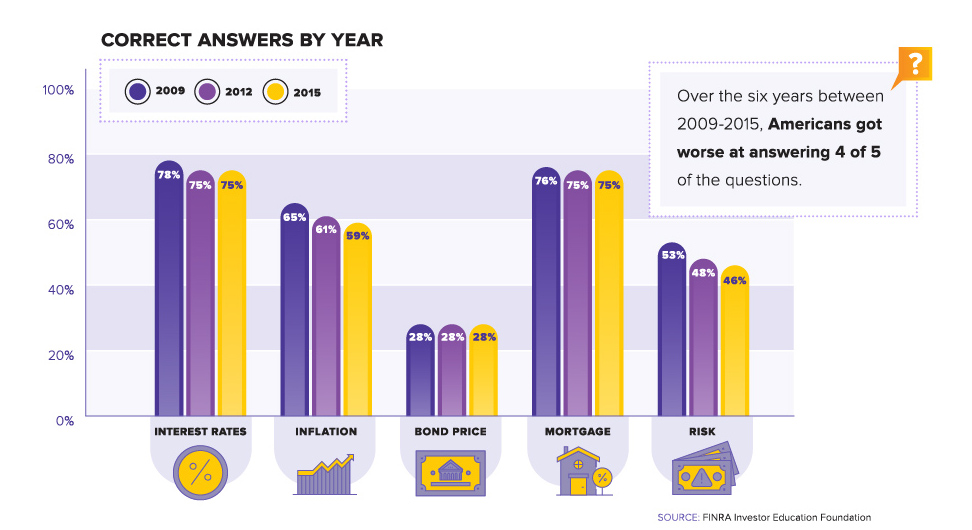

- Between 2009-2015, Americans got worse at answering five key personal finance questions posed by FINRA – a major U.S. financial regulator

And worse, this lack of knowledge is translating into anxiety and even fear.

- Four of five adults say they were never given the opportunity to learn about personal finance

- 70% of millennials are stressed and anxious about saving for retirement

- 22% of millennials feel overwhelmed about their finances

- 13% of millennials feel scared

Meanwhile, student debt is soaring to new highs – how do we put our students in a better spot to succeed?

The Road Ahead

As financial products continue to increase in complexity, the road ahead is not an easy one.

However, there is still a great case for optimism: 60% of Americans say they know someday they will need to be more financially secure – they just don’t know how to get there. This number increases to 70% for those between the ages of 18-39 years old.

This means there is actually a great thirst for financial education out there – the question is just how to best deliver that information in a compelling way.

Another good sign? The youngest generation, Gen Z, is already starting to think about money differently:

Gen Z saw millennials struggle with wage stagnation and huge college debt, so they took note and are making a conscious effort to approach money and debt differently.

– Jason Dorsey, Center for Generational Kinetics

Real World Benefits

Increased financial literacy translates into real world benefits for individuals, and to the economy as a whole.

People with strong financial skills are better at job planning and saving for retirement. Meanwhile, financial savvy investors are more likely to diversify risk, and students that take a personal finance course see up to a 5.2% increase in credit scores within two years.

Lastly, consumers that understand compound interest:

- Spend less on transaction fees

- Accrue less debt

- Incur lower interest rates on loans

- Save more money

And this is just scratching the surface of what could be possible.

Making the right financial decisions can help people meet their own personal goals, live a life of abundance, get out of debt, and become financially independent.

This infographic was originally published on the Wealth 101: A Crash Course in Personal Finance minisite, a collaboration between NGPF and Visual Capitalist

Money

Chart: The Declining Value of the U.S. Federal Minimum Wage

This graphic compares the nominal vs. inflation-adjusted value of the U.S. minimum wage, from 1940 to 2023.

The Declining Value of the U.S. Federal Minimum Wage

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

This graphic illustrates the history of the U.S. federal minimum wage using data compiled by Statista, in both nominal and real (inflation-adjusted) terms. The federal minimum wage was raised to $7.25 per hour in July 2009, where it has remained ever since.

Nominal vs. Real Value

The data we used to create this graphic can be found in the table below.

| Year | Nominal value ($/hour) | Real value ($/hour) |

|---|---|---|

| 1940 | 0.3 | 6.5 |

| 1945 | 0.4 | 6.82 |

| 1950 | 0.75 | 9.64 |

| 1955 | 0.75 | 8.52 |

| 1960 | 1 | 10.28 |

| 1965 | 1.25 | 12.08 |

| 1970 | 1.6 | 12.61 |

| 1975 | 2.1 | 12.04 |

| 1980 | 3.1 | 11.61 |

| 1985 | 3.35 | 9.51 |

| 1990 | 3.8 | 8.94 |

| 1995 | 4.25 | 8.49 |

| 2000 | 5.15 | 9.12 |

| 2005 | 5.15 | 8.03 |

| 2010 | 7.25 | 10.09 |

| 2015 | 7.25 | 9.3 |

| 2018 | 7.25 | 8.78 |

| 2019 | 7.25 | 8.61 |

| 2020 | 7.25 | 8.58 |

| 2021 | 7.25 | 8.24 |

| 2022 | 7.25 | 7.61 |

| 2023 | 7.25 | 7.25 |

What our graphic shows is how inflation has eroded the real value of the U.S. minimum wage over time, despite nominal increases.

For instance, consider the year 1960, when the federal minimum wage was $1 per hour. After accounting for inflation, this would be worth around $10.28 today!

The two lines converge at 2023 because the nominal and real value are identical in present day terms.

Many States Have Their Own Minimum Wage

According to the National Conference of State Legislatures (NCSL), 30 states and Washington, D.C. have implemented a minimum wage that is higher than $7.25.

The following states have adopted the federal minimum: Georgia, Idaho, Indiana, Iowa, Kansas, Kentucky, New Hampshire, North Carolina, North Dakota, Oklahoma, Pennsylvania, Texas, Utah, Wisconsin, and Wyoming.

Meanwhile, the states of Alabama, Louisiana, Mississippi, South Carolina, and Tennessee have no wage minimums, but have to follow the federal minimum.

How Does the U.S. Minimum Wage Rank Globally?

If you found this topic interesting, check out Mapped: Minimum Wage Around the World to see which countries have the highest minimum wage in monthly terms, as of January 2023.

-

Education1 week ago

Education1 week agoHow Hard Is It to Get Into an Ivy League School?

-

Technology2 weeks ago

Technology2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Demographics2 weeks ago

Demographics2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries

-

Economy2 weeks ago

Economy2 weeks agoWhere U.S. Inflation Hit the Hardest in March 2024

-

Environment2 weeks ago

Environment2 weeks agoTop Countries By Forest Growth Since 2001