Investor Education

Here’s How to Become a 401(k) Millionaire

.container {

max-width: 1070px;

}

.button {

display: inline-block;

height: 45px;

color: #ffffff;

text-align: center;

font-family: helvetica;

letter-spacing: .01rem;

text-decoration: none;

white-space: nowrap;

border-radius: 0px;

line-height: 45px;

border: 1px;

font-size: em(13);

cursor: pointer;

box-sizing: border-box;

background: #353956;

transition-duration: 0.4s;

margin-bottom: 1px;

width: 16.6666%;

}

.button-group {

position: left;

width: 100%;

display: inline-block;

list-style: none;

padding: 0;

margin: 0;

/* IE hacks */

zoom: 1;

*display: inline;

}

.button-group li {

float: left;

padding: 0;

margin: 0;

}

.button-group .button {

display: inline-block;

box-sizing: border-box;

color: white;

}

.button-group > .button:not(:first-child):not(:last-child), .button-group li:not(:first-child):not(:last-child) .button {

border-radius: 0;

}

.button-group > .button:first-child, .button-group li:first-child .button {

margin-left: 0;

border-top-right-radius: 0;

border-bottom-right-radius: 0;

}

.button-group > .button:last-child, .button-group li:last-child > .button {

border-top-left-radius: 0;

border-bottom-left-radius: 0;

border-bottom-right-radius: 0;

}

.button:hover {

background-color: #8E8059;

}

.button.active {

background-color: #8E8059;

}

.button-group :not(:last-child) {

border-right: 1px solid white;

padding-right: 2px;

}

.button-group {

border-right: none;

margin-right: none;

}

@media (max-width: 600px) {

.button {

font-size: 13px;}

}

Here’s How to Become a 401(k) Millionaire

There’s nothing more definitive in the journey to financial freedom than hitting the $1 million mark in retirement savings.

A nest egg like that is a near-guarantee that you could surmount any curveball the world throws at you, whether it is an unexpected family emergency or anything else.

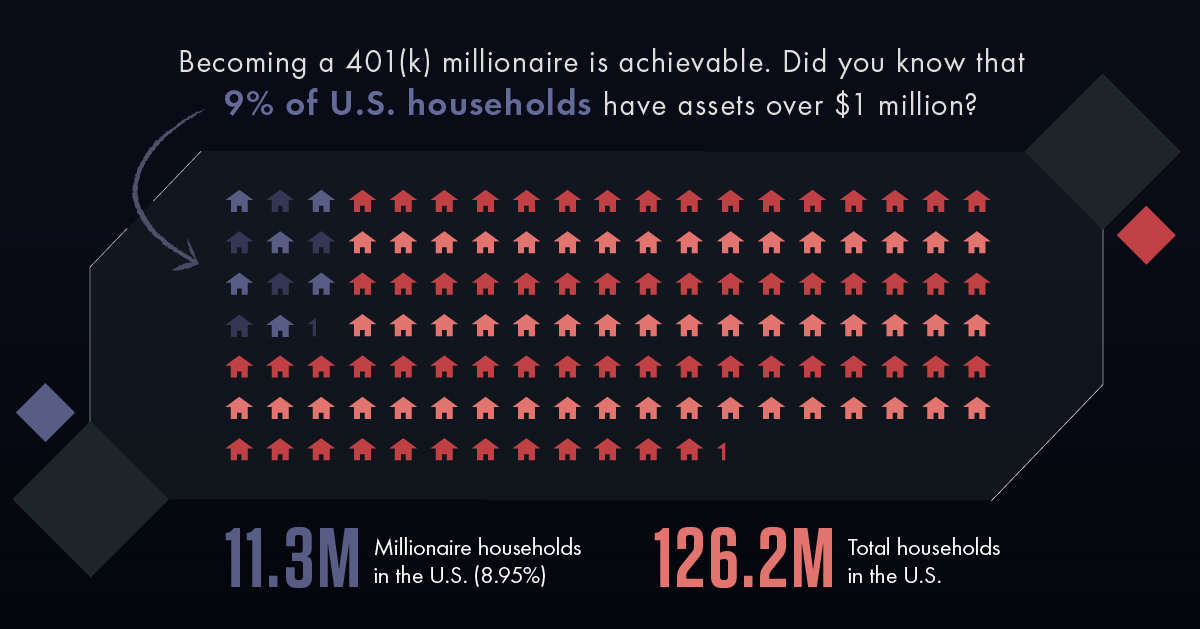

While $1 million certainly sounds like a lofty milestone to many, it’s actually quite a common achievement:

- Millionaire households in the U.S.: 11.3 million (8.95%)

- Total households in the U.S.: 126.2 million

And contrary to popular belief, to become a 401(k) millionaire, you don’t need to strike it rich with a lucky stock pick, or use a crystal ball to forecast the future of the market.

Your best bet is to simply focus only on the factors you can control.

What You Can Control

Today’s infographic is from Tony Robbins, and it covers key points from his #1 Best Selling book Unshakeable: Your Financial Freedom Playbook, which is now available on paperback.

It shows that the biggest winners in the financial game know that they can’t predict the future, and instead titans like Warren Buffett or Jack Bogle focus intently on the factors they can control, knowing that with the right approach they’ll thrive in almost any market.

What are these crucial factors?

| Factor | Description |

|---|---|

| Time | The force of compound interest is more powerful over longer periods of time. |

| Discipline | Staying calm and focused on the long term during periods of turmoil is key. |

| Diversification | Proper asset allocation and frequent re-balancing can position you to weather any storm. |

| Expenses | Expenses and taxes are silent killers, and must be minimized strategically. |

By diligently working to take control of these four factors, your odds of attaining financial freedom are extremely high. Here is each factor in more depth.

1. Time

The power of compound interest is extraordinary, making time your best friend when it comes to building a battle chest of retirement savings.

The current maximum contribution limit for 401(k)s is $18,500 per year, not including what is matched by your employer. If you maxed out on contributions and started investing early, you can hit $1 million before retirement even in sub-optimal market conditions:

| Starting age | Required returns for $1 million at age 65 |

|---|---|

| 30 | 2.20% |

| 35 | 3.45% |

| 40 | 5.40% |

| 45 | 8.55% |

| 50 | 14.50% |

Time can make up for a lack of investing acumen. Wait until later, and things get very difficult – by age 50, you need market beating returns!

2. Discipline

If you’re taking advantage of the power of compound interest over a long period of time, whether that is 20, 30, or 40 years, it is inevitable that there will be bumps in the road:

- Stock market corrections happen once a year, on average

- Bear markets happen once in every 3-5 years, on average

- Bear markets vary in length, but on average last one year

Through decades of investing, the fact is you are going to see bear markets – it is how you handle them that counts.

Even when it’s the most tempting to sell, remember these facts:

- Bear markets become bull markets

- The first 12 months of a new bull market can see crucial market gains

- Nobody can successfully time the market – not even the experts

In other words, having the discipline to hold through the turbulence can be the difference maker – and a key factor you can control in your journey to becoming a 401(k) millionaire.

3. Diversification

Another factor you control is portfolio diversification, and here are four ways diversification can minimize risk:

| Diversification Technique | Examples |

|---|---|

| Assets | Stocks, bonds, and alternative assets like real estate or gold. |

| Sectors | Consumer goods, tech, energy, financials, etc. |

| Markets | Domestic, international, emerging markets |

| Time | Add to investments regularly, because there is never a “right” time to buy |

A properly designed portfolio can weather any storm, and re-balancing it on a regular basis will force you to sell assets at market highs, while buying at low points.

4. Expenses

The fees on your 401(k) statement might not seem like much, but even 1% or 2% can make a big difference over the long term.

For example: the value of $1 compounding for 50 years at 5% will be worth $11.50, but if it averages 7% it will be worth $29.50. That’s almost three times more!

Expenses, both seen and hidden, can be a silent killer any portfolio, so keeping them to a necessary minimum can help you get to the promised land.

A Final Word

If becoming a 401(k) millionaire was easy, everyone could do it.

But to be successful, you need to take control over factors like time, diversification, discipline, and costs – ideally with a qualified and experienced financial advisor and partner. Then, you need to stick to the plan and let the market do its work.

Investing is a game of inches. If your returns improve by, say, 2 or 3 percentage points a year, the cumulative impact over decades is astounding, thanks to the power of compounding.

– Tony Robbins

Investor Education

How MSCI Builds Thematic Indexes: A Step-by-Step Guide

From developing an index objective to choosing relevant stocks, this graphic breaks down how MSCI builds thematic indexes using examples.

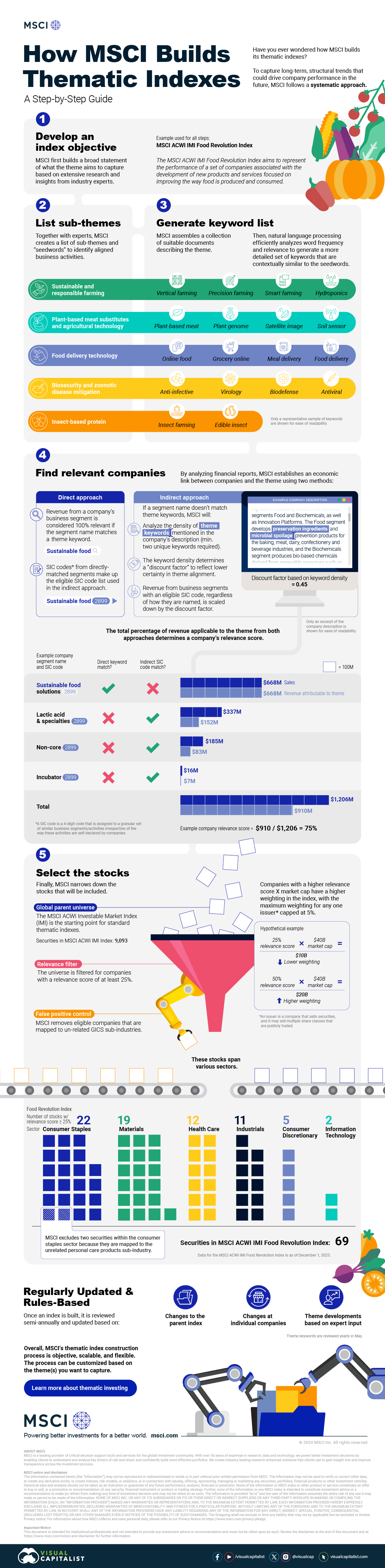

How MSCI Builds Thematic Indexes: A Step-by-Step Guide

Have you ever wondered how MSCI builds its thematic indexes?

To capture long-term, structural trends that could drive business performance in the future, the company follows a systematic approach. This graphic from MSCI breaks down each step in the process used to create its thematic indexes.

Step 1: Develop an Index Objective

MSCI first builds a broad statement of what the theme aims to capture based on extensive research and insights from industry experts.

Steps 2 and 3: List Sub-Themes, Generate Keyword List

Together with experts, MSCI creates a list of sub-themes or “seedwords” to identify aligned business activities.

The team then assembles a collection of suitable documents describing the theme. Natural language processing efficiently analyzes word frequency and relevance to generate a more detailed set of keywords contextually similar to the seedwords.

Step 4: Find Relevant Companies

By analyzing financial reports, MSCI picks companies relevant to the theme using two methods:

- Direct approach: Revenue from a company’s business segment is considered 100% relevant if the segment name matches a theme keyword. Standard Industrial Classification (SIC) codes from these directly-matched segments make up the eligible SIC code list used in the indirect approach.

- Indirect approach: If a segment name doesn’t match theme keywords, MSCI will:

- Analyze the density of theme keywords mentioned in the company’s description. A minimum of two unique keywords is required.

- The keyword density determines a “discount factor” to reflect lower certainty in theme alignment.

- Revenue from business segments with an eligible SIC code, regardless of how they are named, is scaled down by the discount factor.

The total percentage of revenue applicable to the theme from both approaches determines a company’s relevance score.

Step 5: Select the Stocks

Finally, MSCI narrows down the stocks that will be included:

- Global parent universe: The ACWI Investable Market Index (IMI) is the starting point for standard thematic indexes.

- Relevance filter: The universe is filtered for companies with a relevance score of at least 25%.

- False positive control: Eligible companies that are mapped to un-related GICS sub-industries are removed.

Companies with higher relevance scores and market caps have a higher weighting in the index, with the maximum weighting for any one issuer capped at 5%. The final selected stocks span various sectors.

MSCI Thematic Indexes: Regularly Updated and Rules-Based

Once an index is built, it is reviewed semi-annually and updated based on:

- Changes to the parent index

- Changes at individual companies

- Theme developments based on expert input

Theme keywords are reviewed yearly in May. Overall, MSCI’s thematic index construction process is objective, scalable, and flexible. The process can be customized based on the theme(s) you want to capture.

Learn more about MSCI’s thematic indexes.

-

Investor Education6 months ago

Investor Education6 months agoThe 20 Most Common Investing Mistakes, in One Chart

Here are the most common investing mistakes to avoid, from emotionally-driven investing to paying too much in fees.

-

Stocks10 months ago

Stocks10 months agoVisualizing BlackRock’s Top Equity Holdings

BlackRock is the world’s largest asset manager, with over $9 trillion in holdings. Here are the company’s top equity holdings.

-

Investor Education10 months ago

Investor Education10 months ago10-Year Annualized Forecasts for Major Asset Classes

This infographic visualizes 10-year annualized forecasts for both equities and fixed income using data from Vanguard.

-

Investor Education1 year ago

Investor Education1 year agoVisualizing 90 Years of Stock and Bond Portfolio Performance

How have investment returns for different portfolio allocations of stocks and bonds compared over the last 90 years?

-

Debt2 years ago

Debt2 years agoCountries with the Highest Default Risk in 2022

In this infographic, we examine new data that ranks the top 25 countries by their default risk.

-

Markets2 years ago

Markets2 years agoThe Best Months for Stock Market Gains

This infographic analyzes over 30 years of stock market performance to identify the best and worst months for gains.

-

Green1 week ago

Green1 week agoRanking the Top 15 Countries by Carbon Tax Revenue

-

Technology2 weeks ago

Technology2 weeks agoThe Stock Performance of U.S. Chipmakers So Far in 2024

-

Markets2 weeks ago

Markets2 weeks agoCharted: Big Four Market Share by S&P 500 Audits

-

Real Estate2 weeks ago

Real Estate2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Travel2 weeks ago

Travel2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Countries2 weeks ago

Countries2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075