Money

Why Anti-Money Laundering Should Be a Top Priority for Financial Institutions

Why AML Should be a Top Priority for Financial Institutions

The to-do list for any financial executive is surely daunting. From navigating technology changes to managing talent effectively, there’s many initiatives competing for attention.

One issue that’s been in the headlines for many years is anti-money laundering (AML). When criminals are able to successfully hide the illicit origins of their cash, both the financial institution and society suffer. So, what makes AML more important now than it has been in the past?

Rising up the Priority Ladder

Today’s infographic from McKinsey & Company explains the factors which have brought anti-money laundering urgently to the forefront in recent years.

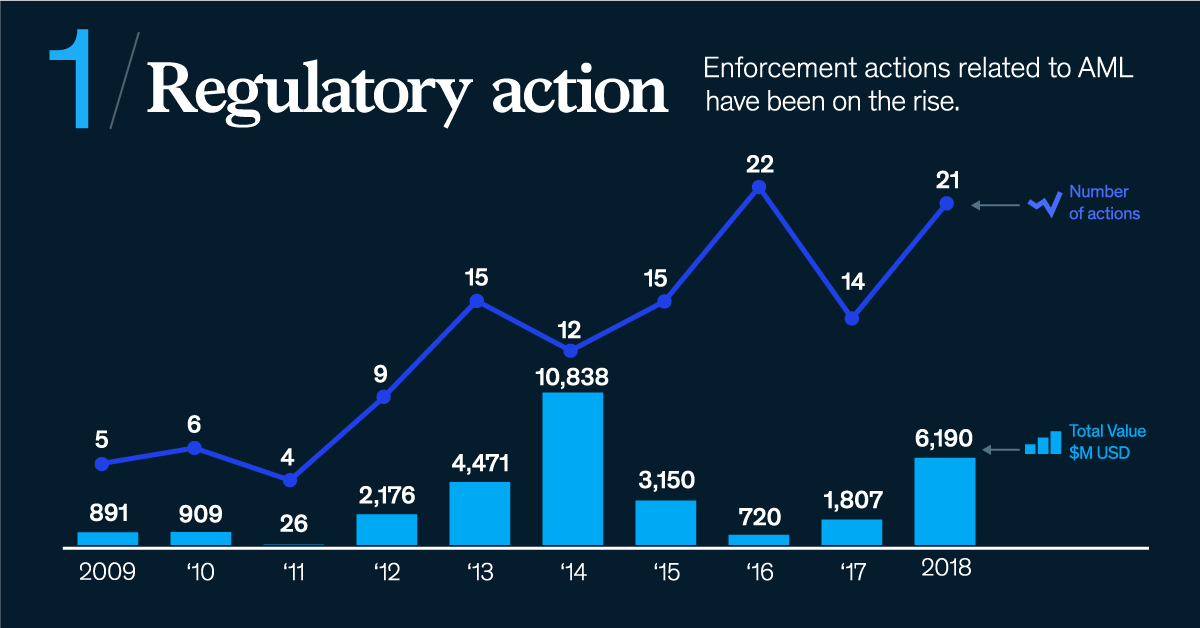

1. Regulatory Action

Enforcement actions related to AML have been on the rise. Since 2009, regulators have levied approximately $32 billion in AML-related fines globally.

2. Threat Evolution

Criminals are using more sophisticated means to remain undetected, including globally-coordinated technology, insider information, and e-commerce schemes.

3. Reputational Risk

AML incidents put a financial institution’s reputation on the line. There’s a lot at stake: today, the average value of each of the top 10 bank brands is $45B.

4. Rising Costs

Most AML activities require significant manual effort, making them inefficient and difficult to scale. In 2018, it cost U.S. financial services firms about $25.3B to manage money laundering risk.

5. Poor Customer Experience

Compliance staff must have multiple touch points with a customer to gather and verify information. Perhaps not surprisingly, one in three financial institutions have lost potential customers due to inefficient or slow onboarding processes.

It’s no wonder anti-money laundering has now become a top priority for many CEOs in the financial industry.

A Wave of Innovation

In the last five years, there has been an explosion of “RegTech” startups—companies that address regulatory requirements using technology.

Global RegTech Investments, 2014-2018

| Year | Amount Invested (USD) |

|---|---|

| 2014 | $923M |

| 2015 | $1,110M |

| 2016 | $1,150M |

| 2017 | $1,868M |

| 2018 | $4,485M |

Over 60% of these are focused on solving Know Your Customer (KYC) and AML issues. What does this technology look like in practice?

Customer onboarding

A hypothetical U.S. retail firm, ABC Electronics, applies online to open an account at AML Innovators Bank. Their information is verified and screened using a fully automated process.

If they are determined to be a lower-risk client, they will be fast-tracked through the approval process with decisioning in six hours or less. For high-risk clients, decisioning occurs within about 72 hours.

Transaction Monitoring

ABC Electronics requests to send multiple international wire payments to various beneficiaries. Each transaction is automatically screened based on various factors:

- A same name or subsidiary transfer carries the lowest risk

- Transfers to a known, similar industry in a high-risk jurisdiction carry medium risk

- Transfers to an unknown industry in a high-risk jurisdiction carry high risk

These transaction scores, combined with algorithms that track a client’s expected vs. actual transaction behavior, will update ABC Electronics’ risk rating in real time.

Management oversight

As risk updates occur, ABC Electronics’ rating is integrated into AML Innovator Bank’s overall portfolio risk.

Senior risk management teams will be able to view a heat map that highlights the highest risk areas of the business.

Structural Change, Big Gains

Just as financial crimes continue to evolve, so do AML schemes.

How can organizations stay ahead of the game? They can focus on actively managing risk, deliberately investing in technology and analytics, and prioritizing areas where RegTechs will have the highest near-term impact.

By investing in AML, financial institutions create competitive advantages:

- Improved efficiency

- Superior customer experience

- Scalability

- Readiness to adapt to new regulations

- Reduced reputational risk

- Ability to attract top talent

With such benefits on the table, one thing is clear: Anti-money laundering efforts are more important now than they have ever been.

Money

Charted: Which City Has the Most Billionaires in 2024?

Just two countries account for half of the top 20 cities with the most billionaires. And the majority of the other half are found in Asia.

Charted: Which Country Has the Most Billionaires in 2024?

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Some cities seem to attract the rich. Take New York City for example, which has 340,000 high-net-worth residents with investable assets of more than $1 million.

But there’s a vast difference between being a millionaire and a billionaire. So where do the richest of them all live?

Using data from the Hurun Global Rich List 2024, we rank the top 20 cities with the highest number of billionaires in 2024.

A caveat to these rich lists: sources often vary on figures and exact rankings. For example, in last year’s reports, Forbes had New York as the city with the most billionaires, while the Hurun Global Rich List placed Beijing at the top spot.

Ranked: Top 20 Cities with the Most Billionaires in 2024

The Chinese economy’s doldrums over the course of the past year have affected its ultra-wealthy residents in key cities.

Beijing, the city with the most billionaires in 2023, has not only ceded its spot to New York, but has dropped to #4, overtaken by London and Mumbai.

| Rank | City | Billionaires | Rank Change YoY |

|---|---|---|---|

| 1 | 🇺🇸 New York | 119 | +1 |

| 2 | 🇬🇧 London | 97 | +3 |

| 3 | 🇮🇳 Mumbai | 92 | +4 |

| 4 | 🇨🇳 Beijing | 91 | -3 |

| 5 | 🇨🇳 Shanghai | 87 | -2 |

| 6 | 🇨🇳 Shenzhen | 84 | -2 |

| 7 | 🇭🇰 Hong Kong | 65 | -1 |

| 8 | 🇷🇺 Moscow | 59 | No Change |

| 9 | 🇮🇳 New Delhi | 57 | +6 |

| 10 | 🇺🇸 San Francisco | 52 | No Change |

| 11 | 🇹🇭 Bangkok | 49 | +2 |

| 12 | 🇹🇼 Taipei | 45 | +2 |

| 13 | 🇫🇷 Paris | 44 | -2 |

| 14 | 🇨🇳 Hangzhou | 43 | -5 |

| 15 | 🇸🇬 Singapore | 42 | New to Top 20 |

| 16 | 🇨🇳 Guangzhou | 39 | -4 |

| 17T | 🇮🇩 Jakarta | 37 | +1 |

| 17T | 🇧🇷 Sao Paulo | 37 | No Change |

| 19T | 🇺🇸 Los Angeles | 31 | No Change |

| 19T | 🇰🇷 Seoul | 31 | -3 |

In fact all Chinese cities on the top 20 list have lost billionaires between 2023–24. Consequently, they’ve all lost ranking spots as well, with Hangzhou seeing the biggest slide (-5) in the top 20.

Where China lost, all other Asian cities—except Seoul—in the top 20 have gained ranks. Indian cities lead the way, with New Delhi (+6) and Mumbai (+3) having climbed the most.

At a country level, China and the U.S combine to make up half of the cities in the top 20. They are also home to about half of the world’s 3,200 billionaire population.

In other news of note: Hurun officially counts Taylor Swift as a billionaire, estimating her net worth at $1.2 billion.

-

Science1 week ago

Science1 week agoVisualizing the Average Lifespans of Mammals

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries

-

United States2 weeks ago

United States2 weeks agoWhere U.S. Inflation Hit the Hardest in March 2024

-

Green2 weeks ago

Green2 weeks agoTop Countries By Forest Growth Since 2001

-

United States2 weeks ago

United States2 weeks agoRanked: The Largest U.S. Corporations by Number of Employees

-

Maps2 weeks ago

Maps2 weeks agoThe Largest Earthquakes in the New York Area (1970-2024)

-

Green2 weeks ago

Green2 weeks agoRanked: The Countries With the Most Air Pollution in 2023

-

Green2 weeks ago

Green2 weeks agoRanking the Top 15 Countries by Carbon Tax Revenue