Datastream

How Does the Bill and Melinda Gates Foundation Invest Its Money?

The Briefing

- The Bill and Melinda Gates Foundation Trust has a total portfolio value of over $25 billion

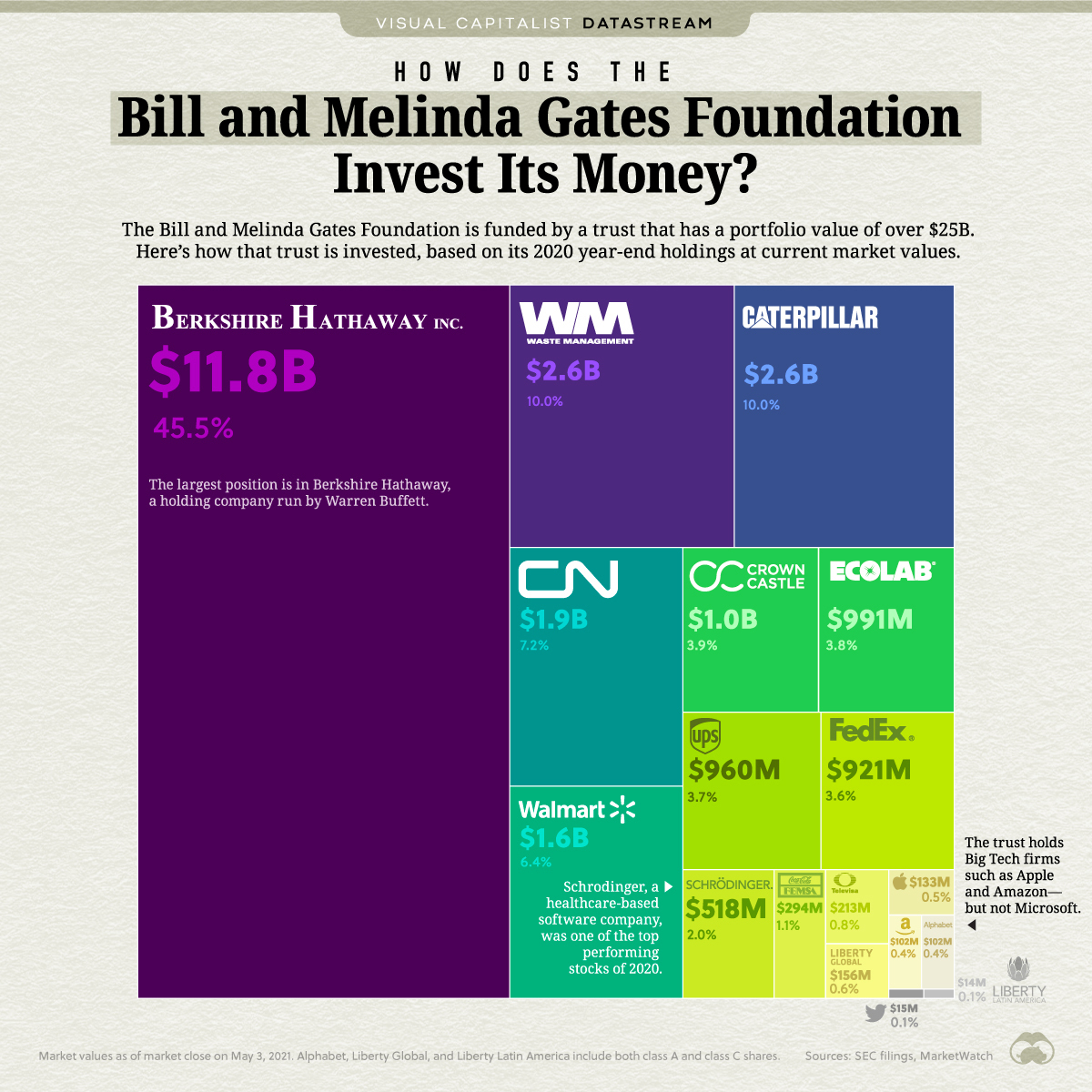

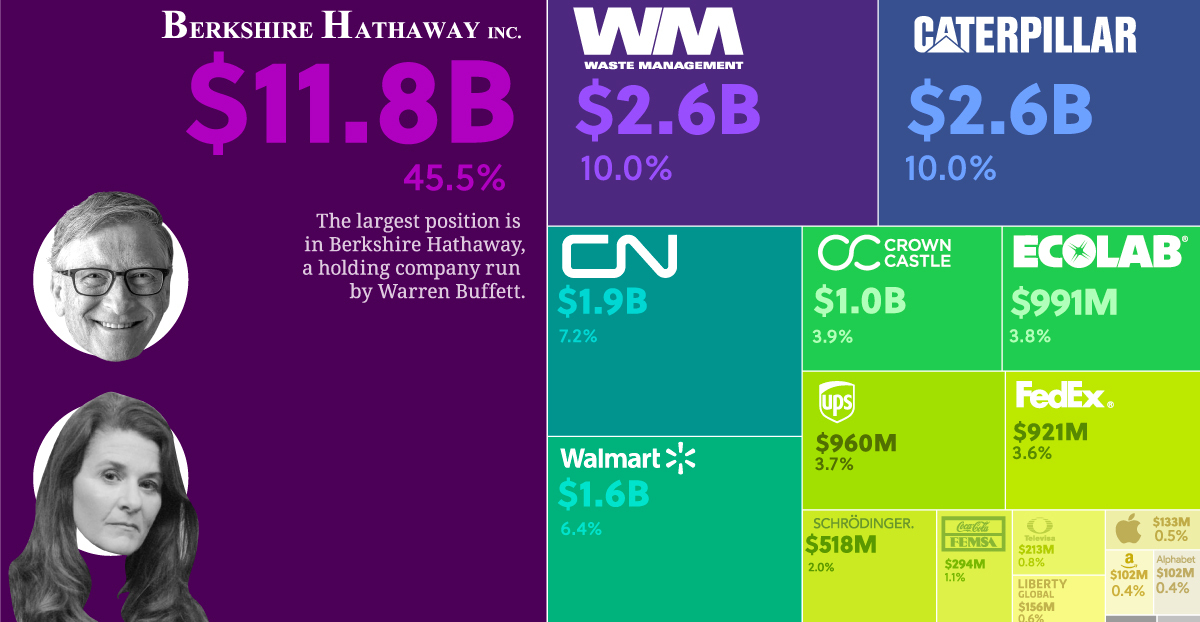

- Almost half of the money is invested in Berkshire Hathaway, a holding company run by chairman and CEO Warren Buffett

- The trust favors industrial stocks, with a 34% weighting in the sector

How Does the Bill and Melinda Gates Foundation Invest Its Money?

Bill and Melinda Gates have announced they are ending their marriage, but will continue to work together at their foundation.

The Bill and Melinda Gates Foundation, launched in 2000, is the largest private philanthropic organization in the United States. It has spent over $50 billion on global public health over the last two decades, including $1.75 billion on COVID-19 relief.

Of course, the foundation’s assets are managed by a trust until they are ready to be distributed to grantees. Here’s a look at how the Bill and Melinda Gates Foundation Trust invests its assets.

The Portfolio Breakdown

The trust has invested 100% of its holdings in stocks. It holds almost half of its value in Berkshire Hathaway, the holding company run by Warren Buffett.

| Stock | Value | % of Portfolio |

|---|---|---|

| Berkshire Hathaway | $11.8B | 45.5% |

| Waste Management | $2.6B | 10.0% |

| Caterpillar | $2.6B | 10.0% |

| Canadian National Railway | $1.9B | 7.2% |

| Walmart | $1.6B | 6.4% |

| Crown Castle | $1.0B | 3.9% |

| Ecolab | $991M | 3.8% |

| UPS | $960M | 3.7% |

| FedEx | $921M | 3.6% |

| Schrodinger | $518M | 2.0% |

| Coca-Cola FEMSA | $294M | 1.1% |

| Grupo Televisa | $213M | 0.8% |

| Liberty Global | $156M | 0.6% |

| Apple | $133M | 0.5% |

| Amazon | $102M | 0.4% |

| Alphabet (Google) | $102M | 0.4% |

| $15M | 0.1% | |

| Liberty Latin America | $14M | 0.1% |

However, the portfolio is more diversified than initially meets the eye—Berkshire Hathaway itself is invested in almost 50 stocks.

Shrodinger, a healthcare-focused software company that makes up 2% of the trust’s total portfolio, was one of the best performing stocks of 2020 by price returns. The portfolio has also been boosted by delivery companies UPS and FedEx, both of which saw their share prices more than double over the last year as online shopping took off.

While the trust is dominated by U.S.-domiciled companies, a few foreign names do make the list. For example, Canadian National Railway makes up over 7% of the portfolio, while the Latin American bottler Coca-Cola FEMSA makes up just over 1%.

The Future of the Foundation

The trust continues to be managed by a team of outside investment managers, whose decisions have a critical impact on the amount of money the Bill and Melinda Gates Foundation has to fund its initiatives. For example, if Berkshire Hathaway were to dip 10%, this would drop the portfolio value by more than $1 billion.

In addition, the foundation is funded in part by the Gates’ personal donations—more than $36 billion from 1994 to 2018. Should Bill and Melinda go on to create their own separate philanthropic efforts post-divorce, the foundation may have a smaller portfolio to pull from going forward.

» Like this? Then you might also like The Warren Buffett Empire in One Giant Chart

Where does this data come from?

Source: SEC filings and MarketWatch

Notes: Portfolio holdings are as of December 31, 2020. Stock values are as of market close on May 3, 2021.

Datastream

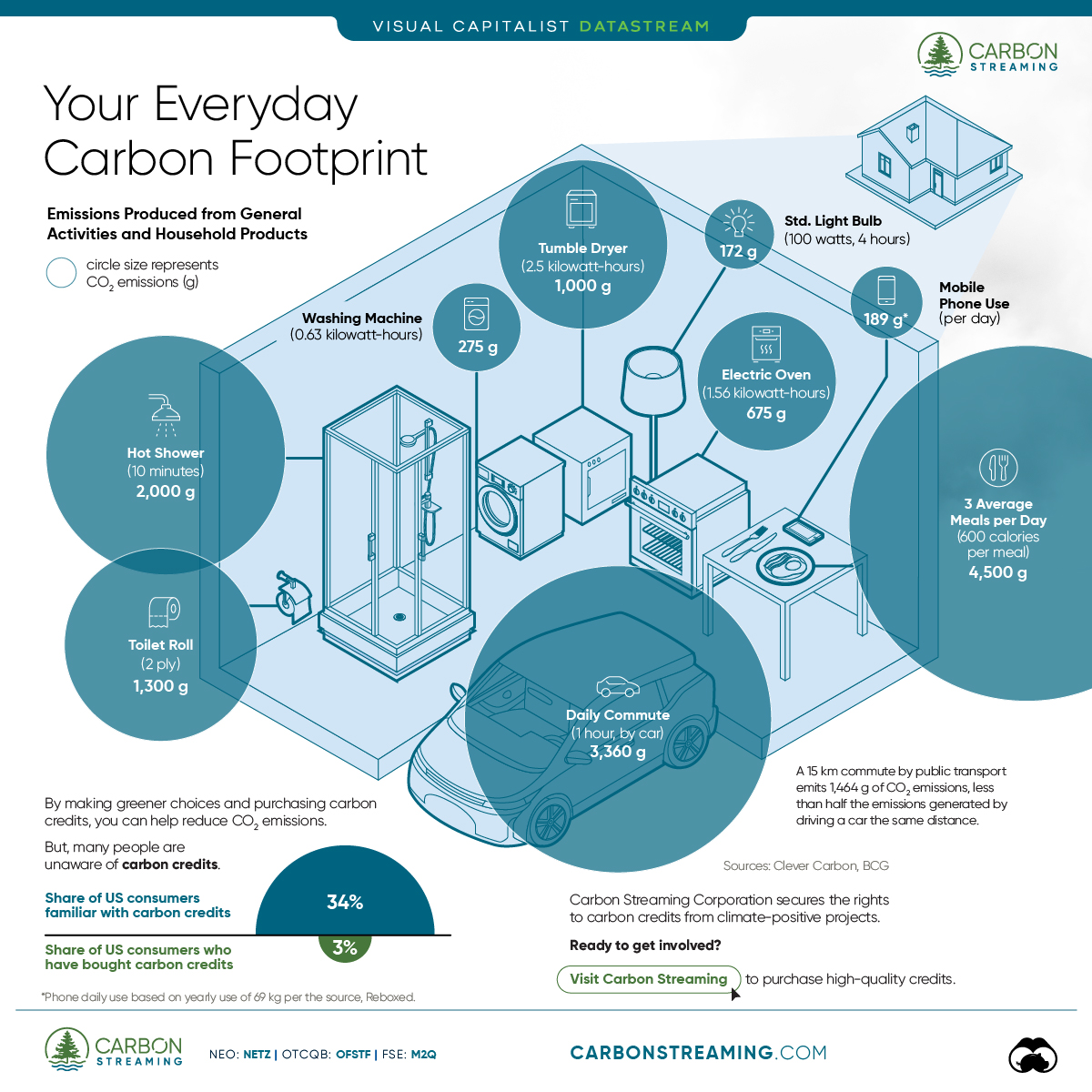

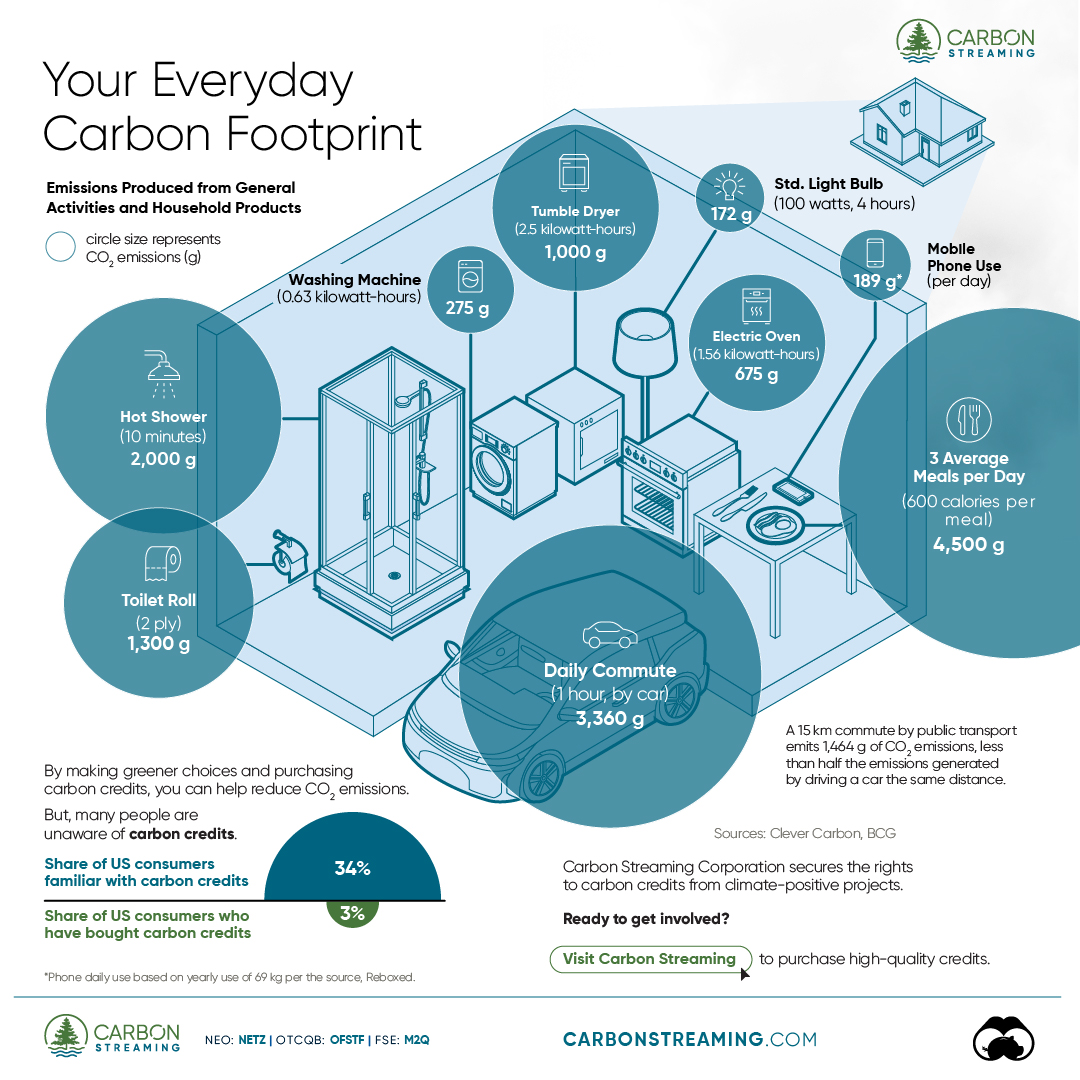

Can You Calculate Your Daily Carbon Footprint?

Discover how the average person’s carbon footprint impacts the environment and learn how carbon credits can offset your carbon footprint.

The Briefing

- A person’s carbon footprint is substantial, with activities such as food consumption creating as much as 4,500 g of CO₂ emissions daily.

- By purchasing carbon credits from Carbon Streaming Corporation, you can offset your own emissions and fund positive climate action.

Your Everyday Carbon Footprint

While many large businesses and countries have committed to net-zero goals, it is essential to acknowledge that your everyday activities also contribute to global emissions.

In this graphic, sponsored by Carbon Streaming Corporation, we will explore how the choices we make and the products we use have a profound impact on our carbon footprint.

Carbon Emissions by Activity

Here are some of the daily activities and products of the average person and their carbon footprint, according to Clever Carbon.

| Household Activities & Products | CO2 Emissions (g) |

|---|---|

| 💡 Standard Light Bulb (100 watts, four hours) | 172 g |

| 📱 Mobile Phone Use (195 minutes per day)* | 189 g |

| 👕 Washing Machine (0.63 kWh) | 275 g |

| 🔥 Electric Oven (1.56 kWh) | 675 g |

| ♨️ Tumble Dryer (2.5 kWh) | 1,000 g |

| 🧻 Toilet Roll (2 ply) | 1,300 g |

| 🚿 Hot Shower (10 mins) | 2,000 g |

| 🚙 Daily Commute (one hour, by car) | 3,360 g |

| 🍽️ Average Daily Food Consumption (three meals of 600 calories) | 4,500 g |

| *Phone use based on yearly use of 69kg per the source, Reboxed | |

Your choice of transportation plays a crucial role in determining your carbon footprint. For instance, a 15 km daily commute to work on public transport generates an average of 1,464 g of CO₂ emissions. Compared to 3,360 g—twice the volume for a journey the same length by car.

By opting for more sustainable modes of transport, such as cycling, walking, or public transportation, you can significantly reduce your carbon footprint.

Addressing Your Carbon Footprint

One way to compensate for your emissions is by purchasing high-quality carbon credits.

Carbon credits are used to help fund projects that avoid, reduce or remove CO₂ emissions. This includes nature-based solutions such as reforestation and improved forest management, or technology-based solutions such as the production of biochar and carbon capture and storage (CCS).

While carbon credits offer a potential solution for individuals to help reduce global emissions, public awareness remains a significant challenge. A BCG-Patch survey revealed that only 34% of U.S. consumers are familiar with carbon credits, and only 3% have purchased them in the past.

About Carbon Streaming

By financing the creation or expansion of carbon projects, Carbon Streaming Corporation secures the rights to future carbon credits generated by these sustainable projects. You can then purchase these carbon credits to help fund climate solutions around the world and compensate for your own emissions.

Ready to get involved?

>> Learn more about purchasing carbon credits at Carbon Streaming

-

Mining1 week ago

Mining1 week agoGold vs. S&P 500: Which Has Grown More Over Five Years?

-

Markets2 weeks ago

Markets2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Countries2 weeks ago

Countries2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries