Demographics

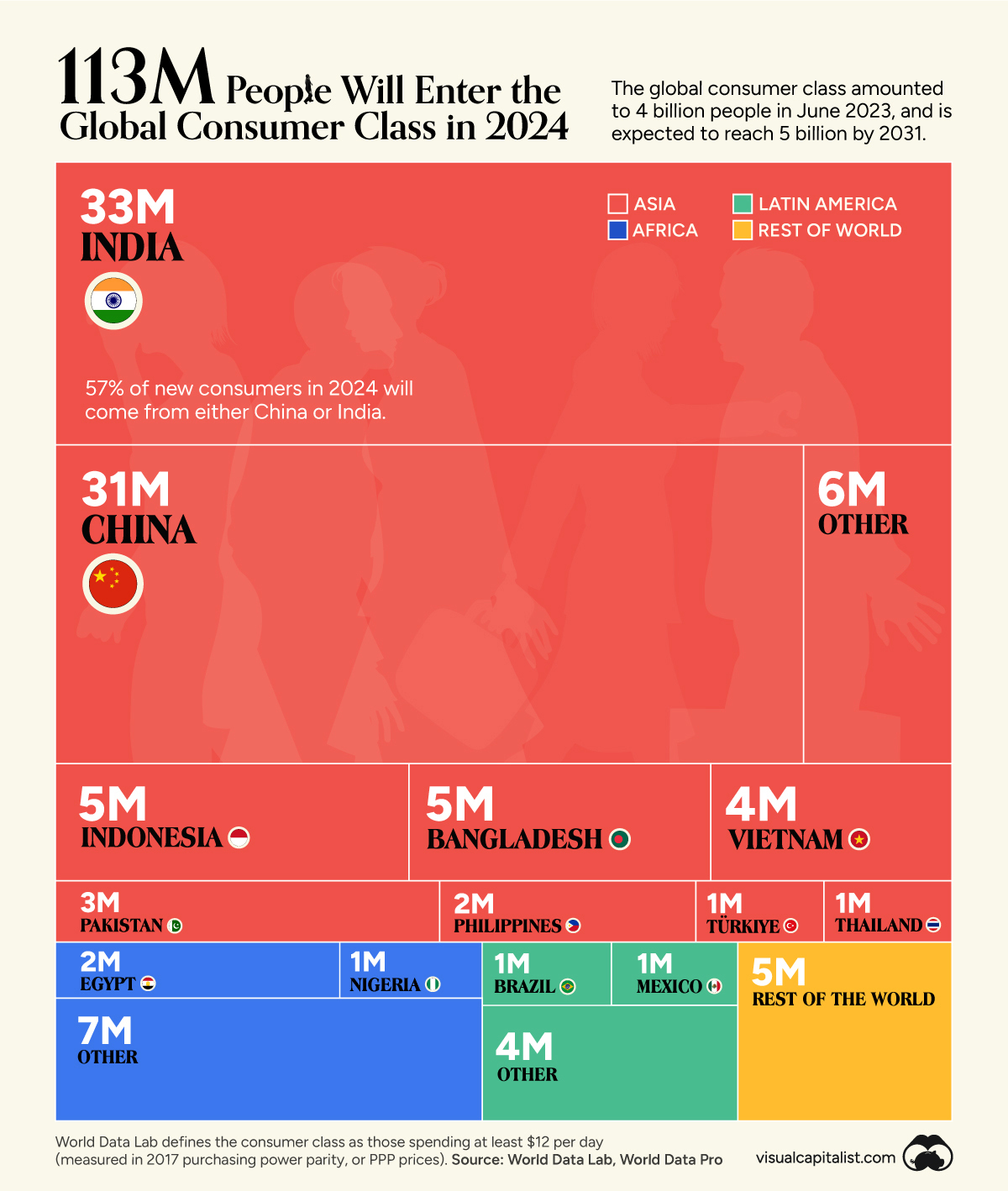

113 Million People Will Join the Global Middle Class in 2024

113 Million People Will Join the Global Middle Class in 2024

Every year, over 100 million people enter the global middle class.

Defined by the World Data Lab as someone who spends at least $12 per day (measured in 2017 purchasing power parity), these individuals are typically rising up in developing regions like Asia and Africa.

In this graphic, we’ve created a treemap diagram that shows where the new entrants to this consumer class in 2024 will originate from.

Where are Millions of New Consumers Coming From?

World Data Lab expects 113 million people to join the global middle class in 2024, with the vast majority coming from Asia.

The following table includes the data we used to create this graphic, at a regional level (figures rounded).

| Region | New Consumers (millions) |

|---|---|

| 🌏 Asia | 91 |

| 🌍 Africa | 10 |

| 🌎 Latin America | 6 |

| 🗺️ Rest of World | 5 |

Based on these figures, we can conclude that Asia will contribute 81% of new consumers in 2024.

Highlights from Asia

The following table breaks down Asia’s 91 million new consumers for 2024, by country. Note that only countries which contribute at least 1 million consumers were broken out, with the rest grouped into “Other”.

| Country | New Consumers (millions) |

|---|---|

| 🇨🇳 China | 31 |

| 🇮🇳 India | 33 |

| 🇮🇩 Indonesia | 5 |

| 🇧🇩 Bangladesh | 5 |

| 🇻🇳 Vietnam | 4 |

| 🇵🇰 Pakistan | 3 |

| 🇵🇭 Philippines | 2 |

| 🇹🇷 Türkiye | 1 |

| 🇹🇭 Thailand | 1 |

| 🗺️ Other | 6 |

As expected, China and India are projected to be the two biggest sources of additions to the global middle class in 2024. Both countries have massive populations, rising income levels, and high rates of urbanization.

Further down the list we can see Indonesia and Bangladesh adding 5 million consumers each. Both of these countries have an expansive population pyramid, meaning they have a relatively young average age and growing labor forces.

It’s interesting to note that many of the countries listed above, including Vietnam, Philippines, and Thailand, also happen to be some of the fastest growing e-commerce markets in the world.

Highlights from Africa

Egypt and Nigeria are the only countries from the Africa region that will contribute more than 1 million consumers in 2024. Once again, both countries are characterized by their high growth potential and above-average birth rates.

In fact, by 2075, Goldman Sachs believes that Egypt and Nigeria could become the fifth and seventh largest economies in the world, surpassing traditional economic leaders like Japan, Germany, and the UK.

Demographics

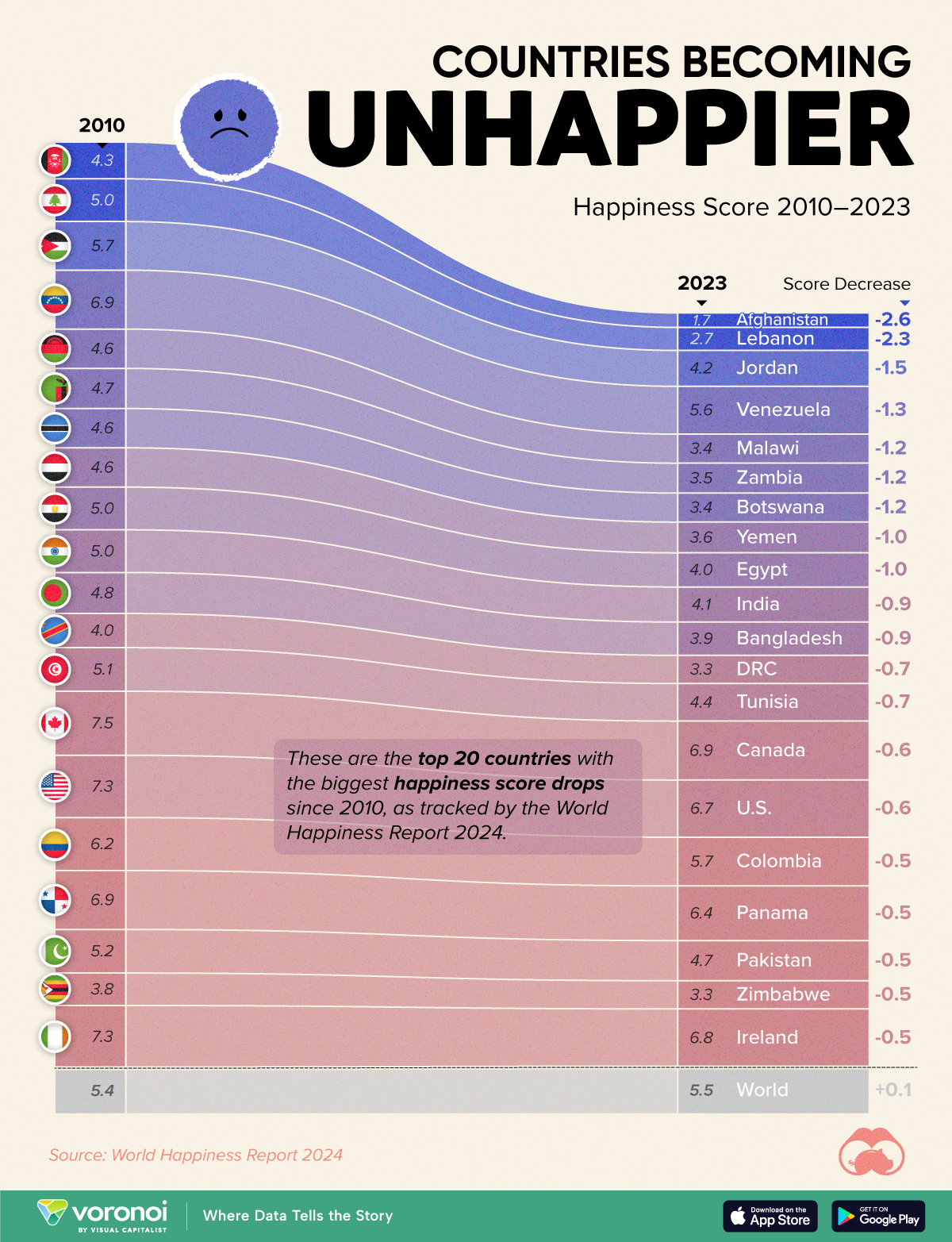

The Countries That Have Become Sadder Since 2010

Tracking Gallup survey data for more than a decade reveals some countries are witnessing big happiness declines, reflecting their shifting socio-economic conditions.

The Countries That Have Become Sadder Since 2010

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Can happiness be quantified?

Some approaches that try to answer this question make a distinction between two differing components of happiness: a daily experience part, and a more general life evaluation (which includes how people think about their life as a whole).

The World Happiness Report—first launched in 2012—has been making a serious go at quantifying happiness, by examining Gallup poll data that asks respondents in nearly every country to evaluate their life on a 0–10 scale. From this they extrapolate a single “happiness score” out of 10 to compare how happy (or unhappy) countries are.

More than a decade later, the 2024 World Happiness Report continues the mission. Its latest findings also include how some countries have become sadder in the intervening years.

Which Countries Have Become Unhappier Since 2010?

Afghanistan is the unhappiest country in the world right now, and is also 60% unhappier than over a decade ago, indicating how much life has worsened since 2010.

In 2021, the Taliban officially returned to power in Afghanistan, after nearly two decades of American occupation in the country. The Islamic fundamentalist group has made life harder, especially for women, who are restricted from pursuing higher education, travel, and work.

On a broader scale, the Afghan economy has suffered post-Taliban takeover, with various consequent effects: mass unemployment, a drop in income, malnutrition, and a crumbling healthcare system.

| Rank | Country | Happiness Score Loss (2010–24) | 2024 Happiness Score (out of 10) |

|---|---|---|---|

| 1 | 🇦🇫 Afghanistan | -2.6 | 1.7 |

| 2 | 🇱🇧 Lebanon | -2.3 | 2.7 |

| 3 | 🇯🇴 Jordan | -1.5 | 4.2 |

| 4 | 🇻🇪 Venezuela | -1.3 | 5.6 |

| 5 | 🇲🇼 Malawi | -1.2 | 3.4 |

| 6 | 🇿🇲 Zambia | -1.2 | 3.5 |

| 7 | 🇧🇼 Botswana | -1.2 | 3.4 |

| 8 | 🇾🇪 Yemen | -1.0 | 3.6 |

| 9 | 🇪🇬 Egypt | -1.0 | 4.0 |

| 10 | 🇮🇳 India | -0.9 | 4.1 |

| 11 | 🇧🇩 Bangladesh | -0.9 | 3.9 |

| 12 | 🇨🇩 DRC | -0.7 | 3.3 |

| 13 | 🇹🇳 Tunisia | -0.7 | 4.4 |

| 14 | 🇨🇦 Canada | -0.6 | 6.9 |

| 15 | 🇺🇸 U.S. | -0.6 | 6.7 |

| 16 | 🇨🇴 Colombia | -0.5 | 5.7 |

| 17 | 🇵🇦 Panama | -0.5 | 6.4 |

| 18 | 🇵🇰 Pakistan | -0.5 | 4.7 |

| 19 | 🇿🇼 Zimbabwe | -0.5 | 3.3 |

| 20 | 🇮🇪 Ireland | -0.5 | 6.8 |

| N/A | 🌍 World | +0.1 | 5.5 |

Nine countries in total saw their happiness score drop by a full point or more, on the 0–10 scale.

Noticeably, many of them have seen years of social and economic upheaval. Lebanon, for example, has been grappling with decades of corruption, and a severe liquidity crisis since 2019 that has resulted in a banking system collapse, sending poverty levels skyrocketing.

In Jordan, unprecedented population growth—from refugees leaving Iraq and Syria—has aggravated unemployment rates. A somewhat abrupt change in the line of succession has also raised concerns about political stability in the country.

-

Education1 week ago

Education1 week agoHow Hard Is It to Get Into an Ivy League School?

-

Technology2 weeks ago

Technology2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Demographics2 weeks ago

Demographics2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries

-

Economy2 weeks ago

Economy2 weeks agoWhere U.S. Inflation Hit the Hardest in March 2024

-

Green2 weeks ago

Green2 weeks agoTop Countries By Forest Growth Since 2001