Markets

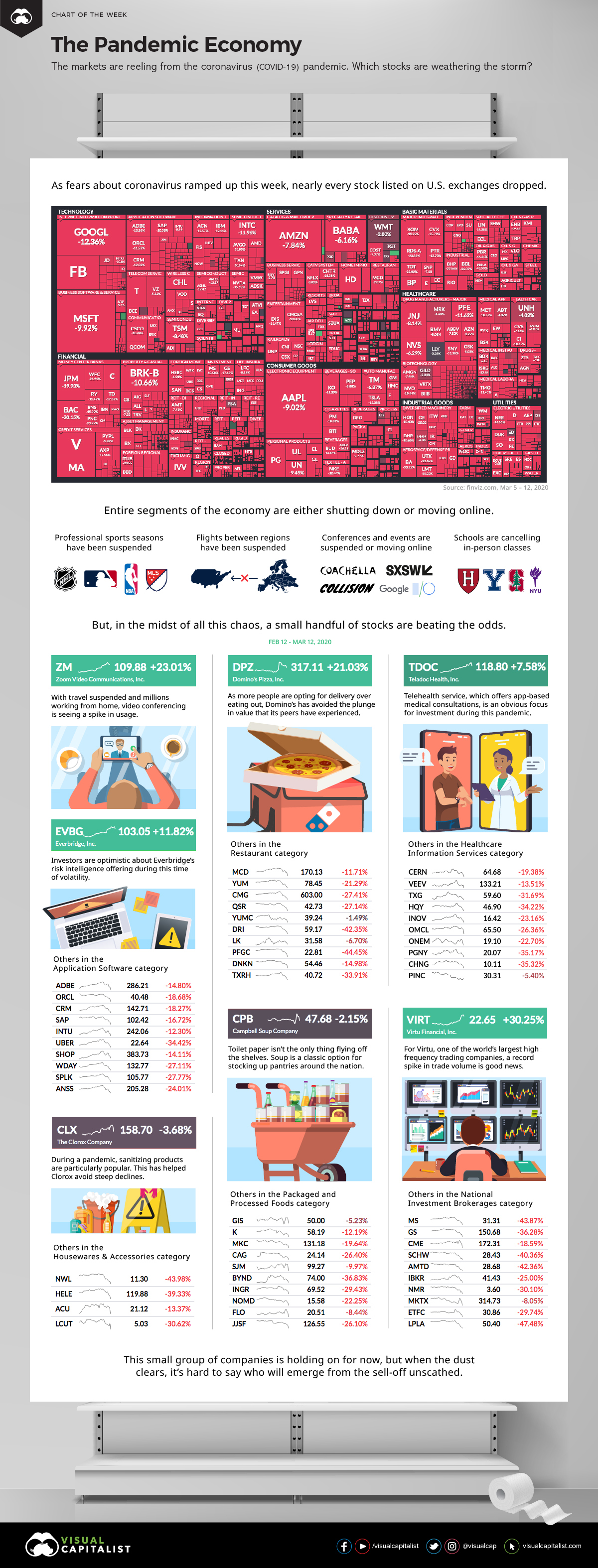

The Pandemic Economy: Which Stocks are Weathering the Storm?

The Pandemic Economy: The Stocks Weathering the Storm

When markets get wacky, even the best companies can’t avoid the maelstrom.

Investors were already tiptoeing on broken glass, knowing that the longest U.S. stock market bull run in history was getting long in the tooth.

Then, when the market foresaw the potential damage that could be caused by the COVID-19 pandemic, it quickly created a vortex that would suck almost everything into it.

Bizarro Market

In the last week, markets flipped into an alternate universe. Every major stock got crushed, while suddenly those holding onto stockpiles of toilet paper and soup reigned supreme.

In such unique circumstances, we wondered which companies were weathering the storm of volatility. To do this, we used Finviz to pull up a visualization of S&P 500 performance, then investigating the segments of the market that were doing well in spite of the recent plunge.

| Stock selection | Performance (Mar 5-12) | Components |

|---|---|---|

| S&P 500 | -18.0% 📉 | The 500 largest U.S. companies by market cap |

| The Pandemic Economy | +12.7% 📈 | Soup, bleach, pizza, and telecommuting stocks |

A few companies not only avoided the chaos — they actually thrived over the last week.

Let’s look at why!

Not Getting Bugged Down

With global travel, events, and social gatherings screeching to a halt, it’s obvious that this is not a winning situation for any typical economy.

However, it’s hard for everyone to simultaneously be a loser, and it’s always inevitable that some stocks will benefit from any crisis — or at least not get hit as hard as their peers.

- Zoom Video Communications (ZM)

There’s no doubt a pandemic is tough on brick-and-mortar companies, but for most white collar workers the show must go on. As a pure play stock in the video conferencing category, Zoom is uniquely positioned as companies shift to more remote work. - Domino’s Pizza (DPZ)

With people wanting to avoid crowds because of COVID-19, it’s natural to want to order in. Domino’s, as well as other companies that focus on food delivery, stand to benefit in the short term from the virus. - Campbell Soup Company (CPB)

Campbell is the quintessential counter-cyclical stock, and even more so in a prepping environment. When the global outlook is gloomy, people want to stockpile — and soup is a major pantry staple. - Teladoc Health, Inc. (TDOC)

If sitting in a doctor’s office with dozens of other sick people can be avoided, it seems it would be regarded as a prudent decision. For this reason, remote health services are an obvious focus for investors during the pandemic. - The Clorox Company (CLX)

Wash your hands. Wash your hands. Have you heard that you should wash your hands to avoid the spread of the coronavirus? Clorox benefits from this sudden interest in sanitation and cleanliness. - Everbridge, Inc. (EVBG)

When times are uncertain, global decision-makers want to get as much quality information as possible. Everbridge offers a risk intelligence platform that provides this service. - Virtu Financial, Inc. (VIRT)

Whether markets are going up or down, large amounts of volume and volatility are a good thing for financial services companies that make money from high frequency trading.

Not all of these companies are in the green — some have simply traded sideways — but on average, they’ve seen a 12.7% bump in price over the last week.

Whether that will last in a fast-changing news environment is another story.

Markets

The European Stock Market: Attractive Valuations Offer Opportunities

On average, the European stock market has valuations that are nearly 50% lower than U.S. valuations. But how can you access the market?

European Stock Market: Attractive Valuations Offer Opportunities

Europe is known for some established brands, from L’Oréal to Louis Vuitton. However, the European stock market offers additional opportunities that may be lesser known.

The above infographic, sponsored by STOXX, outlines why investors may want to consider European stocks.

Attractive Valuations

Compared to most North American and Asian markets, European stocks offer lower or comparable valuations.

| Index | Price-to-Earnings Ratio | Price-to-Book Ratio |

|---|---|---|

| EURO STOXX 50 | 14.9 | 2.2 |

| STOXX Europe 600 | 14.4 | 2 |

| U.S. | 25.9 | 4.7 |

| Canada | 16.1 | 1.8 |

| Japan | 15.4 | 1.6 |

| Asia Pacific ex. China | 17.1 | 1.8 |

Data as of February 29, 2024. See graphic for full index names. Ratios based on trailing 12 month financials. The price to earnings ratio excludes companies with negative earnings.

On average, European valuations are nearly 50% lower than U.S. valuations, potentially offering an affordable entry point for investors.

Research also shows that lower price ratios have historically led to higher long-term returns.

Market Movements Not Closely Connected

Over the last decade, the European stock market had low-to-moderate correlation with North American and Asian equities.

The below chart shows correlations from February 2014 to February 2024. A value closer to zero indicates low correlation, while a value of one would indicate that two regions are moving in perfect unison.

| EURO STOXX 50 | STOXX EUROPE 600 | U.S. | Canada | Japan | Asia Pacific ex. China |

|

|---|---|---|---|---|---|---|

| EURO STOXX 50 | 1.00 | 0.97 | 0.55 | 0.67 | 0.24 | 0.43 |

| STOXX EUROPE 600 | 1.00 | 0.56 | 0.71 | 0.28 | 0.48 | |

| U.S. | 1.00 | 0.73 | 0.12 | 0.25 | ||

| Canada | 1.00 | 0.22 | 0.40 | |||

| Japan | 1.00 | 0.88 | ||||

| Asia Pacific ex. China | 1.00 |

Data is based on daily USD returns.

European equities had relatively independent market movements from North American and Asian markets. One contributing factor could be the differing sector weights in each market. For instance, technology makes up a quarter of the U.S. market, but health care and industrials dominate the broader European market.

Ultimately, European equities can enhance portfolio diversification and have the potential to mitigate risk for investors.

Tracking the Market

For investors interested in European equities, STOXX offers a variety of flagship indices:

| Index | Description | Market Cap |

|---|---|---|

| STOXX Europe 600 | Pan-regional, broad market | €10.5T |

| STOXX Developed Europe | Pan-regional, broad-market | €9.9T |

| STOXX Europe 600 ESG-X | Pan-regional, broad market, sustainability focus | €9.7T |

| STOXX Europe 50 | Pan-regional, blue-chip | €5.1T |

| EURO STOXX 50 | Eurozone, blue-chip | €3.5T |

Data is as of February 29, 2024. Market cap is free float, which represents the shares that are readily available for public trading on stock exchanges.

The EURO STOXX 50 tracks the Eurozone’s biggest and most traded companies. It also underlies one of the world’s largest ranges of ETFs and mutual funds. As of November 2023, there were €27.3 billion in ETFs and €23.5B in mutual fund assets under management tracking the index.

“For the past 25 years, the EURO STOXX 50 has served as an accurate, reliable and tradable representation of the Eurozone equity market.”

— Axel Lomholt, General Manager at STOXX

Partnering with STOXX to Track the European Stock Market

Are you interested in European equities? STOXX can be a valuable partner:

- Comprehensive, liquid and investable ecosystem

- European heritage, global reach

- Highly sophisticated customization capabilities

- Open architecture approach to using data

- Close partnerships with clients

- Part of ISS STOXX and Deutsche Börse Group

With a full suite of indices, STOXX can help you benchmark against the European stock market.

Learn how STOXX’s European indices offer liquid and effective market access.

-

Economy2 days ago

Economy2 days agoEconomic Growth Forecasts for G7 and BRICS Countries in 2024

The IMF has released its economic growth forecasts for 2024. How do the G7 and BRICS countries compare?

-

Markets1 week ago

Markets1 week agoU.S. Debt Interest Payments Reach $1 Trillion

U.S. debt interest payments have surged past the $1 trillion dollar mark, amid high interest rates and an ever-expanding debt burden.

-

United States2 weeks ago

United States2 weeks agoRanked: The Largest U.S. Corporations by Number of Employees

We visualized the top U.S. companies by employees, revealing the massive scale of retailers like Walmart, Target, and Home Depot.

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

This graphic shows the states with the highest real GDP growth rate in 2023, largely propelled by the oil and gas boom.

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

In this graphic, we show the highest earning flight routes globally as air travel continued to rebound in 2023.

-

Markets2 weeks ago

Markets2 weeks agoRanked: The Most Valuable Housing Markets in America

The U.S. residential real estate market is worth a staggering $47.5 trillion. Here are the most valuable housing markets in the country.

-

Mining1 week ago

Mining1 week agoGold vs. S&P 500: Which Has Grown More Over Five Years?

-

Markets2 weeks ago

Ranked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Ranked: The World’s Top Flight Routes, by Revenue

-

Demographics2 weeks ago

Demographics2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

The Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries