Visualizing the Global Demand for Lithium

The following content is sponsored by Scotch Creek Ventures.

Visualizing Global Demand for Lithium

Lithium is one of the most in-demand commodities in the world today.

With the ongoing shift to electric vehicles (EVs) and clean energy technologies, governments and EV manufacturers are rushing to secure their supply chains as demand for lithium soars.

But while China has a strong foothold in the lithium race, the U.S. is lagging behind. This infographic from our sponsor Scotch Creek Ventures highlights the rising demand for lithium and the need for a domestic supply chain in the United States.

What’s Driving the Demand for Lithium?

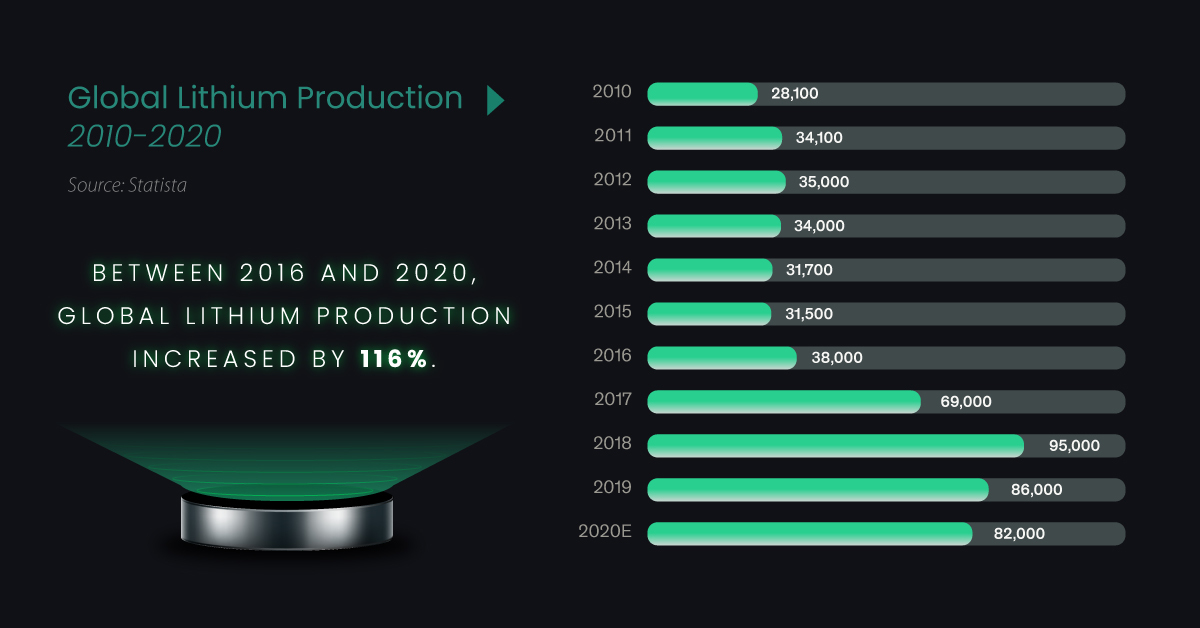

Global lithium production more than doubled in the last four years to 82,000 metric tons in 2020, up from 38,000 metric tons in 2016. Here are some of the factors driving the lithium rush:

- More EVs on the Road:

EV sales have been accelerating in recent years. Between 2016 and 2020, annual electric car sales increased by 297%, up from around 750,000 to nearly 2.9 million cars last year. - Falling Battery Prices:

Declining lithium-ion battery prices are allowing EVs to compete more aggressively with gas-powered cars. Since 2013, battery costs have fallen 80% with a volume-weighted average of $137/kWh in 2020. - Rise of the Battery Megafactories:

More battery manufacturing capacity means more demand for the critical minerals that go into batteries. As of March 2021, there were 200 battery megafactories in the pipeline to 2030, and 122 of those were already operational. According to Benchmark Mineral Intelligence, if all 200 battery megafactories were operating at full capacity, their annual demand for lithium would be 3 million tonnes. That’s almost 37 times the 82,000 tonnes produced in 2020.

Although the demand for lithium is rising globally, its supply chain from mines to batteries relies on a only few critical nations.

China’s Lithium Dominance

In 2020, Australia, Chile, and China collectively made up 88% of global lithium production. After mining, the lithium supply chain involves refining, processing, and packaging the lithium into batteries—and the majority of this occurs in China.

In 2019, China produced 80% of the world’s refined battery chemicals, in addition to 73% of lithium-ion battery cells. What’s more, of the 200 battery megafactories in the pipeline to 2030, 148 are in China. As a result, China is far ahead of other countries in the race for lithium and batteries.

On the other hand, the U.S. is heavily reliant on imports for its supply of lithium, with only one lithium-producing mine in the country. As demand increases, this lack of production could threaten U.S. energy independence in the future. To address this and gaps in the supply of other critical minerals, U.S. President Biden also signed an executive order aiming to build secure supply chains for strategic minerals.

But where is lithium in the United States?

Nevada: The Lithium State

Nevada is known as the Silver State for its rich history of silver mining. Today, it’s the only source of lithium production in the U.S.

Clayton Valley and Kings Valley, two of the country’s largest lithium deposits, are in Nevada. The country’s only producing mine, Albemarle’s Silver Peak Mine, produces around 5,000 tonnes of lithium every year in Clayton Valley. Furthermore, the region is among the world’s richest closed-basin brine deposits based on grade and tonnage.

In addition to a rich lithium deposit, mining companies in Clayton Valley can also reap the advantages of Nevada as a jurisdiction. These include access to infrastructure, a skilled mining workforce, and proximity to a battery manufacturing base with Tesla Gigafactory 1. But that’s not all—in 2020, the Fraser Institute gave Nevada the top spot for mining investment attractiveness globally.

Meeting Lithium Demand for Energy Independence

As countries work to expand EV adoption, critical battery metals like lithium are becoming geopolitically significant, and their supply could redefine energy independence going forward. For this reason, the U.S., EU, and Canada all have lithium on their list of minerals that are critical to national security.

The U.S. needs to build a domestic lithium supply chain from the ground up, and Nevada has the potential to support it with lithium in Clayton Valley. Scotch Creek Ventures is developing two lithium mining projects in Clayton Valley to supply lithium for the green future.

-

Sponsored3 years ago

Sponsored3 years agoMore Than Precious: Silver’s Role in the New Energy Era (Part 3 of 3)

Long known as a precious metal, silver in solar and EV technologies will redefine its role and importance to a greener economy.

-

Sponsored7 years ago

Sponsored7 years agoThe History and Evolution of the Video Games Market

Everything from Pong to the rise of mobile gaming and AR/VR. Learn about the $100 billion video games market in this giant infographic.

-

Sponsored8 years ago

Sponsored8 years agoThe Extraordinary Raw Materials in an iPhone 6s

Over 700 million iPhones have now been sold, but the iPhone would not exist if it were not for the raw materials that make the technology...

-

Sponsored8 years ago

Sponsored8 years agoThe Industrial Internet, and How It’s Revolutionizing Mining

The convergence of the global industrial sector with big data and the internet of things, or the Industrial Internet, will revolutionize how mining works.