Energy

The Base Metal Boom: The Start of a New Bull Market?

Base metals are the most fundamental minerals produced for the modern economy, and metals such as copper, zinc, nickel, lead, and aluminum are the key components that support sustained economic growth.

During periods of economic expansion, these are the first materials to support a bustling economy, reducing inventory at metal warehouses and eventually their source, mines.

A Base Metal Boom?

Today’s infographic comes to us from Tartisan Nickel and it takes a look at the surging demand for base metals for use in renewable energy and EVs, and whether this could translate into a sustained bull market for base metals.

Over the last three years, prices of base metals have risen on the back of a growing economy and the anticipation of usage in new technologies such as lithium-ion batteries, green energy, and electric vehicles:

Cobalt: +232%

Zinc: +64%

Nickel: +59%

Copper: +45%

Lead: +34%

Tin: +36%

Aluminum: +42%

As goes the success and development of nations, so goes the production and consumption of base metals.

Why Higher Prices?

Development outside of the Western world has been the main driver of the base metal boom, and it will likely continue to push prices higher in the future.

China has been the primary consumer of metals due to the country’s rapid economic expansion – and with recent efforts to improve environmental standards, the country is simultaneously eliminating supplies of low quality and environmentally toxic metal production. India and Africa will also be emerging sources of base metal demand for the coming decades.

But this is not solely a story of developing nations, as there are some key developments that will include the developed world in the next wave of demand for base metals.

New Sources of Demand

Future demand for base metals will be driven by the onset of a more connected and sustainable world through the adoption of electronic devices and vehicles. This will require a turnover of established infrastructure and the obsolescence of traditional sources of energy, placing pressure on current sources of base metals.

The transformation will be global and will test the limits of current mineral supply.

Renewable Energy Technology

The power grids around the world will adapt to include renewable sources such as wind, solar and other technologies. According to the World Energy Outlook (IEA 2017), it is expected that between 2017 to 2040, a total of 160 GW of global power net additions will come from renewables each year.

Renewables will capture two-thirds of global investment in power plants to 2040 as they become, for many countries, the cheapest source of new power generation. Renewables rely heavily on base metals for their construction, and would not exist without them.

Electric Vehicles

Gasoline cars will be fossils. According to the International Energy Agency, the number of electric vehicles on the road around the world will hit 125 million by 2030. By this time, China will account for 39% of the global EV market.

Dwindling Supply

Currently, warehouse levels in the London Metals Exchange are sitting at five-year lows, with tin leading the pack with a decline of 400%.

According to the Commodity Markets Outlook (World Bank, April 2018), supply could be curtailed by slower ramp-up of new capacity, tighter environmental constraints, sanctions against commodity producers, and rising costs. If new supply does not come into the market, this could also drive prices for base metals higher.

New Supply?

There is only one source to replenish supply and fulfill future demand, and that is with mining.

New mines need to be discovered, developed and come online to meet demand. In the meantime, those that invest in the base metals could see scarcity drive prices up as the economy moves towards its electric future on a more populated planet.

An extended base metal boom may very well be on the horizon.

Energy

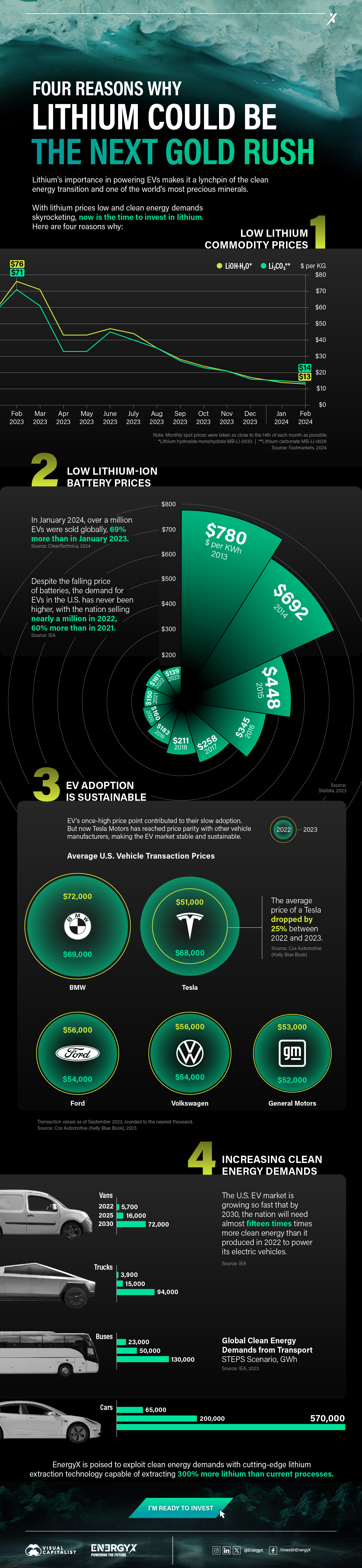

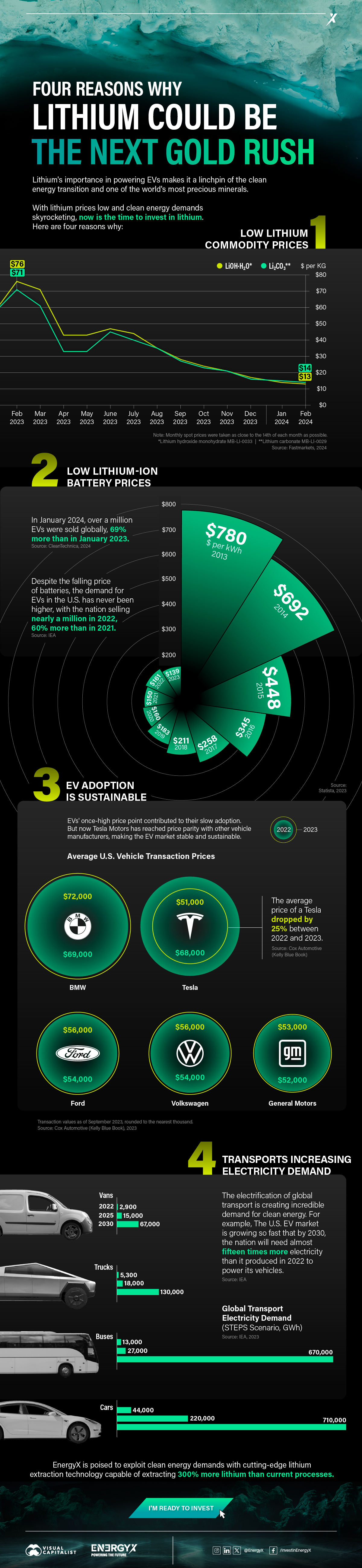

Charted: 4 Reasons Why Lithium Could Be the Next Gold Rush

Visual Capitalist has partnered with EnergyX to show why drops in prices and growing demand may make now the right time to invest in lithium.

4 Reasons Why You Should Invest in Lithium

Lithium’s importance in powering EVs makes it a linchpin of the clean energy transition and one of the world’s most precious minerals.

In this graphic, Visual Capitalist partnered with EnergyX to explore why now may be the time to invest in lithium.

1. Lithium Prices Have Dropped

One of the most critical aspects of evaluating an investment is ensuring that the asset’s value is higher than its price would indicate. Lithium is integral to powering EVs, and, prices have fallen fast over the last year:

| Date | LiOH·H₂O* | Li₂CO₃** |

|---|---|---|

| Feb 2023 | $76 | $71 |

| March 2023 | $71 | $61 |

| Apr 2023 | $43 | $33 |

| May 2023 | $43 | $33 |

| June 2023 | $47 | $45 |

| July 2023 | $44 | $40 |

| Aug 2023 | $35 | $35 |

| Sept 2023 | $28 | $27 |

| Oct 2023 | $24 | $23 |

| Nov 2023 | $21 | $21 |

| Dec 2023 | $17 | $16 |

| Jan 2024 | $14 | $15 |

| Feb 2024 | $13 | $14 |

Note: Monthly spot prices were taken as close to the 14th of each month as possible.

*Lithium hydroxide monohydrate MB-LI-0033

**Lithium carbonate MB-LI-0029

2. Lithium-Ion Battery Prices Are Also Falling

The drop in lithium prices is just one reason to invest in the metal. Increasing economies of scale, coupled with low commodity prices, have caused the cost of lithium-ion batteries to drop significantly as well.

In fact, BNEF reports that between 2013 and 2023, the price of a Li-ion battery dropped by 82%.

| Year | Price per KWh |

|---|---|

| 2023 | $139 |

| 2022 | $161 |

| 2021 | $150 |

| 2020 | $160 |

| 2019 | $183 |

| 2018 | $211 |

| 2017 | $258 |

| 2016 | $345 |

| 2015 | $448 |

| 2014 | $692 |

| 2013 | $780 |

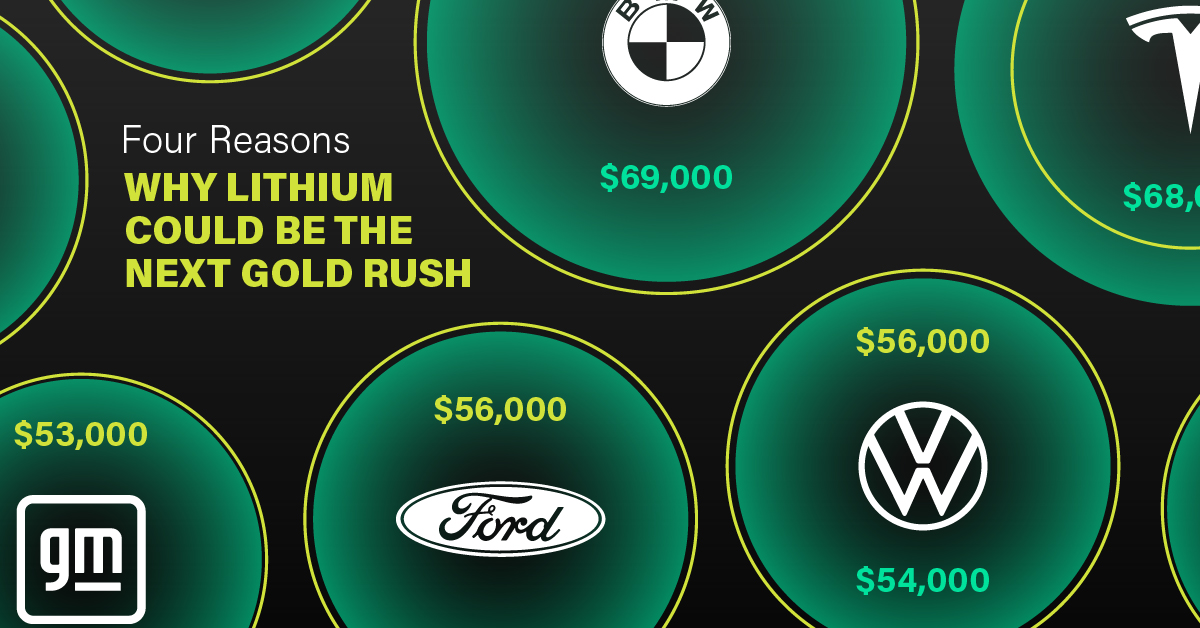

3. EV Adoption is Sustainable

One of the best reasons to invest in lithium is that EVs, one of the main drivers behind the demand for lithium, have reached a price point similar to that of traditional vehicle.

According to the Kelly Blue Book, Tesla’s average transaction price dropped by 25% between 2022 and 2023, bringing it in line with many other major manufacturers and showing that EVs are a realistic transport option from a consumer price perspective.

| Manufacturer | September 2022 | September 2023 |

|---|---|---|

| BMW | $69,000 | $72,000 |

| Ford | $54,000 | $56,000 |

| Volkswagon | $54,000 | $56,000 |

| General Motors | $52,000 | $53,000 |

| Tesla | $68,000 | $51,000 |

4. Electricity Demand in Transport is Growing

As EVs become an accessible transport option, there’s an investment opportunity in lithium. But possibly the best reason to invest in lithium is that the IEA reports global demand for the electricity in transport could grow dramatically by 2030:

| Transport Type | 2022 | 2025 | 2030 |

|---|---|---|---|

| Buses 🚌 | 23,000 GWh | 50,000 GWh | 130,000 GWh |

| Cars 🚙 | 65,000 GWh | 200,000 GWh | 570,000 GWh |

| Trucks 🛻 | 4,000 GWh | 15,000 GWh | 94,000 GWh |

| Vans 🚐 | 6,000 GWh | 16,000 GWh | 72,000 GWh |

The Lithium Investment Opportunity

Lithium presents a potentially classic investment opportunity. Lithium and battery prices have dropped significantly, and recently, EVs have reached a price point similar to other vehicles. By 2030, the demand for clean energy, especially in transport, will grow dramatically.

With prices dropping and demand skyrocketing, now is the time to invest in lithium.

EnergyX is poised to exploit lithium demand with cutting-edge lithium extraction technology capable of extracting 300% more lithium than current processes.

-

Lithium5 days ago

Lithium5 days agoRanked: The Top 10 EV Battery Manufacturers in 2023

Asia dominates this ranking of the world’s largest EV battery manufacturers in 2023.

-

Energy1 week ago

Energy1 week agoThe World’s Biggest Nuclear Energy Producers

China has grown its nuclear capacity over the last decade, now ranking second on the list of top nuclear energy producers.

-

Energy1 month ago

Energy1 month agoThe World’s Biggest Oil Producers in 2023

Just three countries accounted for 40% of global oil production last year.

-

Energy1 month ago

Energy1 month agoHow Much Does the U.S. Depend on Russian Uranium?

Currently, Russia is the largest foreign supplier of nuclear power fuel to the U.S.

-

Uranium2 months ago

Uranium2 months agoCharted: Global Uranium Reserves, by Country

We visualize the distribution of the world’s uranium reserves by country, with 3 countries accounting for more than half of total reserves.

-

Energy3 months ago

Energy3 months agoVisualizing the Rise of the U.S. as Top Crude Oil Producer

Over the last decade, the United States has established itself as the world’s top producer of crude oil, surpassing Saudi Arabia and Russia.

-

Science1 week ago

Science1 week agoVisualizing the Average Lifespans of Mammals

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries

-

United States2 weeks ago

United States2 weeks agoWhere U.S. Inflation Hit the Hardest in March 2024

-

Green2 weeks ago

Green2 weeks agoTop Countries By Forest Growth Since 2001

-

United States2 weeks ago

United States2 weeks agoRanked: The Largest U.S. Corporations by Number of Employees

-

Maps2 weeks ago

Maps2 weeks agoThe Largest Earthquakes in the New York Area (1970-2024)

-

Green2 weeks ago

Green2 weeks agoRanked: The Countries With the Most Air Pollution in 2023