Anticipating the Driverless Future of Vehicles

The following content is sponsored by eToro

Anticipating the Driverless Future of Vehicles

With the rapid rise of electric vehicles (EVs) and increased investments in autonomous driving, what was once the future of vehicles is quickly becoming a present day reality.

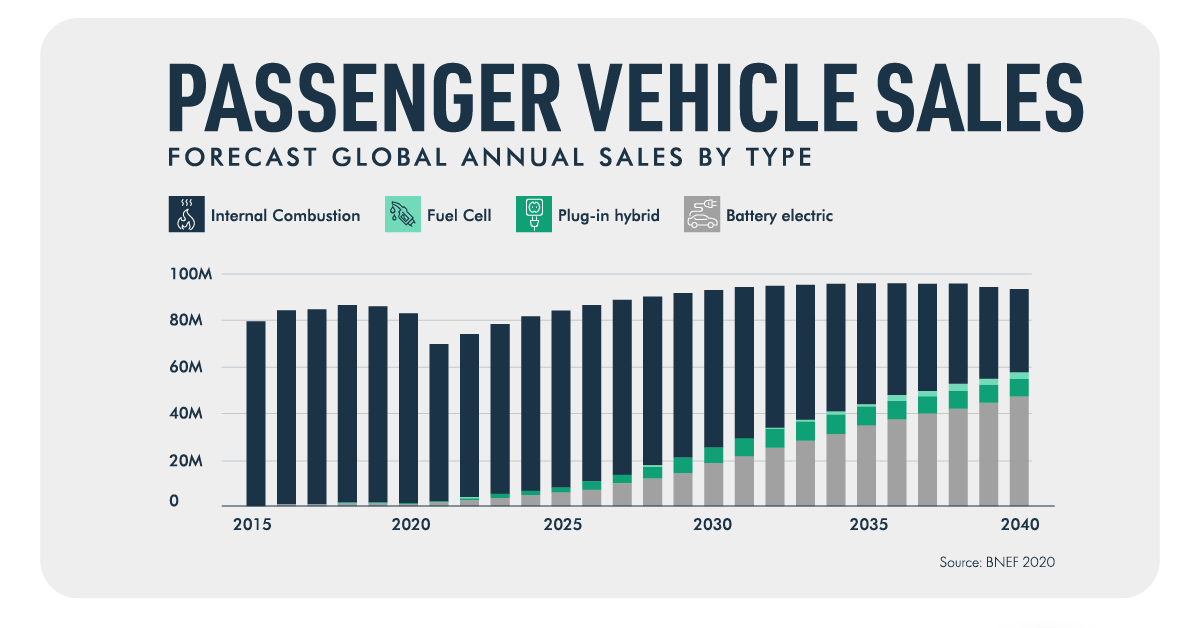

By 2040, EVs are forecast to account for more than half of global annual car sales. A 2020 Consumer Reports survey showed that 31% of U.S. consumers said they are interested in an EV for their next car purchase, with another 40% saying they’re interested in EVs for a future purchase.

And the drive is no longer fueled by just a few players like Tesla. Every major automaker and several Silicon Valley giants are investing billions in the future of vehicles.

This infographic from eToro takes a detailed look at how a driverless future is taking shape right before our eyes.

Driverless Developments in Electric and Autonomous Vehicles

Investments in future-friendly cars are now commonplace—as are new vehicle releases—but for a long time, automakers hesitated to make the electric transition.

With the meteoric rise of Tesla, now a household name in EVs and self-driving vehicles, it’s now clear to the world’s automakers that the pivot to EVs could pay off. As of June 2021, two 100% electric car companies make it onto a list of the highest valued automakers in the world.

| Rank | Company | Market Cap (June 2021) |

|---|---|---|

| #1 | Tesla (100% Electric) | $662.1B |

| #2 | Toyota | $247.0B |

| #3 | Volkswagen | $149.9B |

| #4 | BYD | $102.1B |

| #5 | Daimler | $96.9B |

| #6 | General Motors | $85.1B |

| #7 | NIO (100% Electric) | $80.8B |

| #8 | BMW | $70.4B |

| #9 | Stellantis | $63.1B |

| #10 | Ford | $59.7B |

And as electric car companies started to climb in value, traditional automakers ramped up their EV investments.

In 2019, automakers invested at least $300 billion in EVs and batteries, primarily those based in Germany ($139.5 billion) and China ($57.0 billion). In 2021, American companies have also stepped up their EV investments, with Ford and GM committing $22 billion and $27 billion respectively to EV investments through 2025.

Autonomous, A.I. piloted vehicles are also on the cusp of further investment breakthroughs. Driverless companies Cruise (backed by GM) and Waymo (backed by Alphabet) completed more than 600,000 miles of autonomous driving testing in 2020 in California alone.

Over the next five years, the autonomous vehicle market is forecast to grow to $557 billion by 2026 from just $53 billion in 2019. It’s no surprise that other companies like Toyota, Amazon, SoftBank, Lyft, and Daimler are all investing in driverless companies.

What The Driverless Future Will Look Like

Over the next decade, the speed and visibility of vehicle evolution will depend largely on location.

In the U.S. and Europe, the current trajectory is towards reduction of impact. As consumers shift from combustion engines to EVs, many are also looking to reduce the need for a vehicle in the first place. The total number of cars in the U.S. and Europe is actually expected to drop by more than 100 million by 2030.

That contrasts with China, where car inventory is expected to surge to 276 million in 2030 from just 180 million in 2017. The country is a leader in EV rollouts, with Tesla even building a factory in Shanghai. China is also leaning heavily on autonomous driving —by 2040, driverless vehicles are expected to account for 66% of total passenger KM driven in China.

In fact, driverless vehicles and shared mobility is a leading driver in modern vehicle investment. An analysis of vehicle investments by more than 1000 companies since 2010 found that e-hailing is the leading cluster of investment, followed closely by semiconductors and sensors required by smart cars.

| Vehicle Tech Cluster | Total Disclosed Investment (2010–19) |

|---|---|

| E-hailing | $56.2B |

| Semiconductors | $38.1B |

| AV sensors and ADAS components | $29.9B |

| Connectivity/infotainment | $20.8B |

| EVs and charging | $19.0B |

| Batteries | $14.3B |

| AV software and mapping | $13.5B |

| Telematics and intelligent traffic | $12.4B |

| Back end/cybersecurity | $9.0B |

| HMI and voice recognition | $7.4B |

As investments in future-friendly smart cars continue to ramp up, countries already prepared for EVs are likely to benefit the quickest.

A 2020 assessment of countries by readiness for autonomous vehicles found that Singapore leads the world with driverless-ready policies and high road quality. It was closely followed by the Netherlands and Norway, with EVs already accounting for more than 56% of vehicles purchased in Norway.

Though the full rollout of EVs and driverless vehicles will look different depending on the country, it’s certain that the future of vehicles is on the horizon.

How Can Investors Take Part?

eToro’s Driverless CopyPortfolio* gives investors direct access to the driverless and electric megatrend.

Curated by experienced and proven investment teams, the thematic portfolio offers exposure to a broad range of automakers and innovators in transportation, with no management fees.

*Your capital is at risk.

CopyPortfolios is a portfolio management product, provided by eToro Europe Ltd., which is authorised and regulated by the Cyprus Securities and Exchange Commission.

CopyPortfolios should not be considered as exchange traded funds, nor as hedge funds.

-

Sponsored3 years ago

Sponsored3 years agoMore Than Precious: Silver’s Role in the New Energy Era (Part 3 of 3)

Long known as a precious metal, silver in solar and EV technologies will redefine its role and importance to a greener economy.

-

Sponsored7 years ago

Sponsored7 years agoThe History and Evolution of the Video Games Market

Everything from Pong to the rise of mobile gaming and AR/VR. Learn about the $100 billion video games market in this giant infographic.

-

Sponsored8 years ago

Sponsored8 years agoThe Extraordinary Raw Materials in an iPhone 6s

Over 700 million iPhones have now been sold, but the iPhone would not exist if it were not for the raw materials that make the technology...

-

Sponsored8 years ago

Sponsored8 years agoThe Industrial Internet, and How It’s Revolutionizing Mining

The convergence of the global industrial sector with big data and the internet of things, or the Industrial Internet, will revolutionize how mining works.