Green

9 Things Cannabis Investors Should Know

9 Things Cannabis Investors Should Know

The swift regulatory changes taking place in the global cannabis sector are almost without modern precedent.

While some find the situation analogous to the repeal of Prohibition in the United States, it’s also fair to point out that such events happened 85 years ago in the midst of the Great Depression. It was a long time ago, and in a very different economic climate.

Today’s infographic comes to us from Evolve ETFs, and it shows what investors should know as the legal cannabis sector comes out of the dark.

What Cannabis Investors Should Know

Since there is so much happening at once with little precedent for what such a market will look like, it’s worth summing up the sector’s potential in broad strokes:

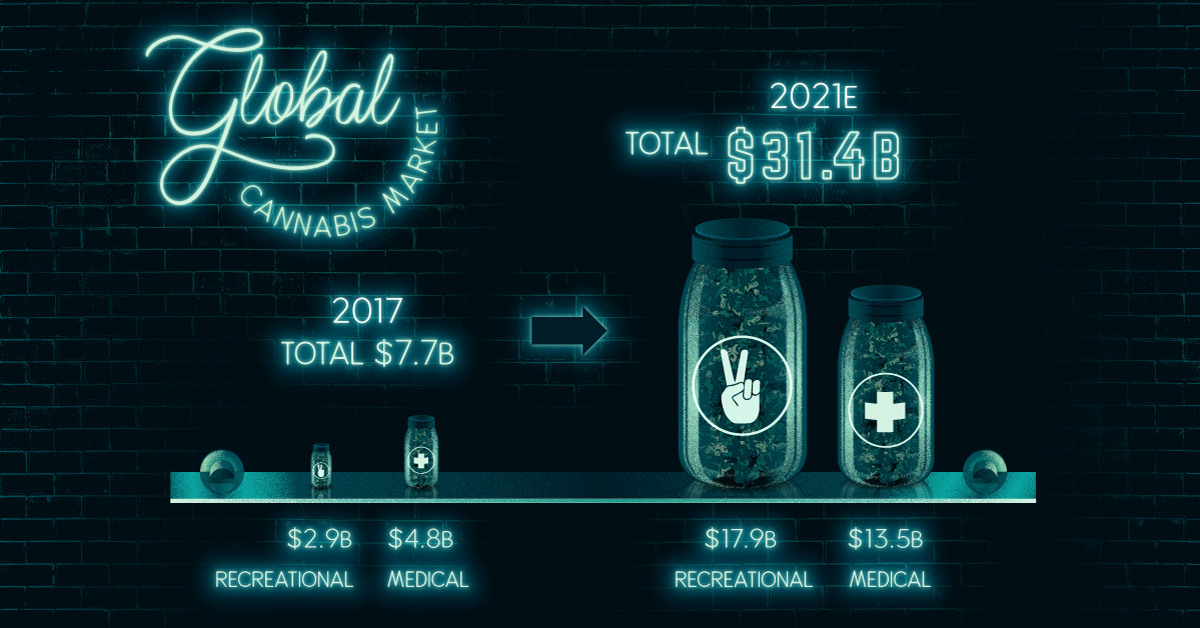

1. Global Size

According to research from The Brightfield Group, the size of the legal cannabis sector is expected to surge from $7.7 billion to $31.4 billion between 2017 and 2021.

Currently the recreational market makes up only 37% of the global total – but by 2021, that will rise to 57%.

2. Versatile Uses

Cannabis comes in different forms. One gram of dried cannabis is roughly equivalent to:

- 5g of fresh cannabis

- 15g of edible product

- 70g of liquid product

- 0.25g of concentrates

- 1 cannabis plant seed

These can be used in various medical applications, including to fight chronic pain, migraines, anxiety, multiple sclerosis, and nausea. Cannabis can also be used to treat Alzheimer’s, PTSD, and cancer.

3. North American Growth

By 2021, it’s estimated that North American sales will make up 86% of the global market. Specifically, the U.S. legal market is projected to hit $18.1 billion by that time, while the Canadian legal market is expected to be $8.9 billion in that same year.

4. A Shifting Legal Landscape

Canada will be the first G7 country to legalize cannabis at a federal level.

In the United States, recreational cannabis is already legalized in nine states – but this could change swiftly as various states undergo referendums.

5. European Markets

In 2017, the legal market for cannabis is estimated to be just $0.11 billion, but by 2021 it will have expanded to $3.8 billion.

According to The Brightfield Group, growth will be quite impressive in Western Europe: Germany’s market will grow at a 284% annual rate, the Netherlands at 364%, and Spain at 334%.

6. Rest of the World

Although markets outside of North America and Europe will not see the same growth in absolute dollar terms, the legal cannabis market will still expand from $80 million to $350 million, led by activity in Latin America.

7. Pharmaceutical Research

Israel has a special place in the cannabis world – the country is world leader in medical cannabis research, and industry expects that it will eventually translate into a $1 billion export opportunity. That said, export plans have hit a recent road bump.

8. Investment Activity

Compare the start of 2018 to that of 2017, and you’ll see an impressive difference in investment activity.

For this we use Canada with its impending recreational legalization as an example: in the first six weeks of 2018, investment was up nearly 7x over the previous year. Further, the average deal size increased from $5.6 million to $18.7 million.

Meanwhile, the Canadian Cannabis Index rose 201% between January 2017 and January 2018.

9. How to Invest?

There are a variety of ways to gain exposure to the sector, including:

- Licensed producer stocks

- Biotech stocks

- Ancillary services stocks

- Licensed retailer stocks

- Cannabis ETFs

Regardless of how you play it, the legal cannabis sector is coming out of the dark – and it will be interesting to see how the industry takes shape.

Green

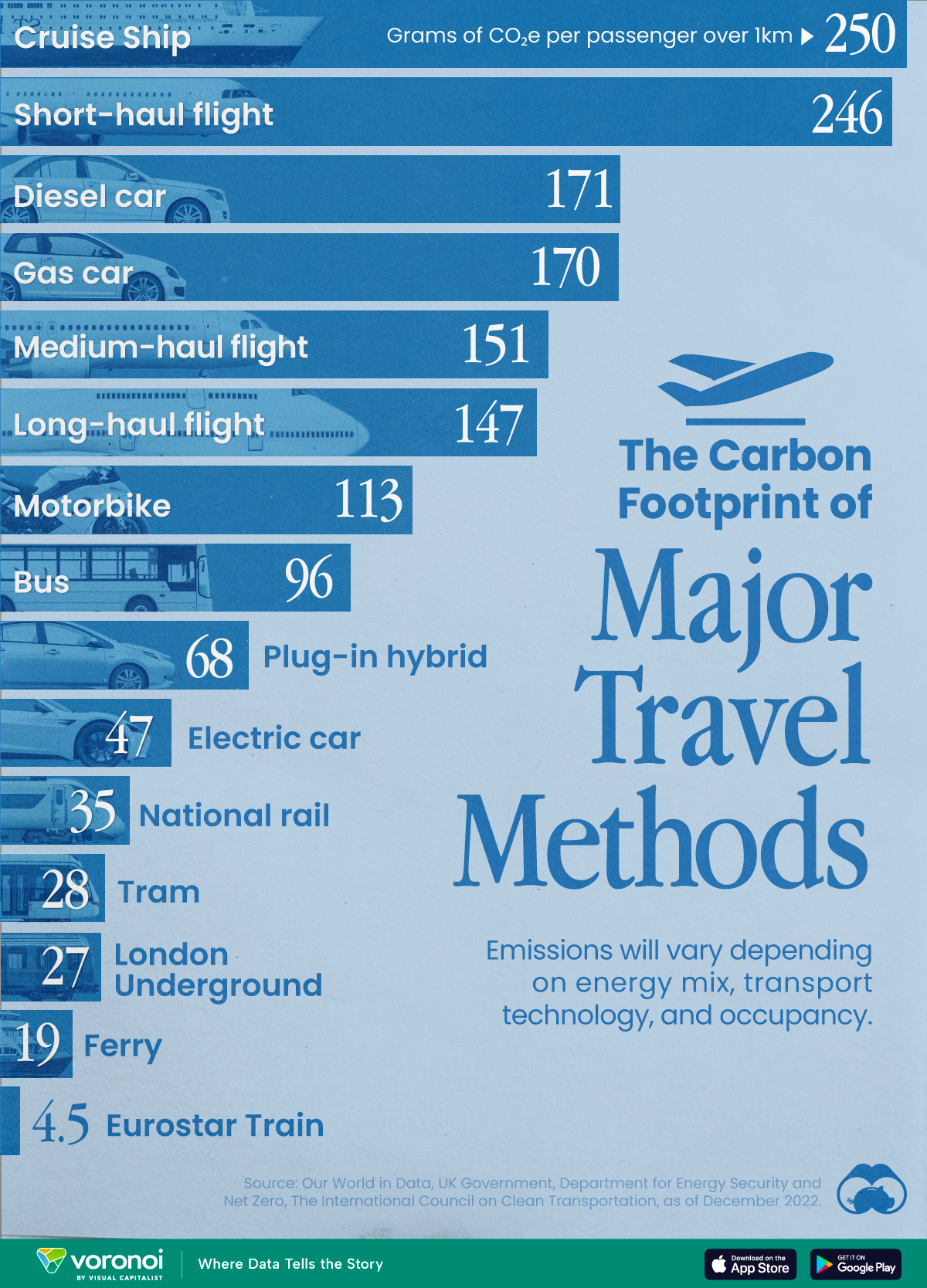

The Carbon Footprint of Major Travel Methods

Going on a cruise ship and flying domestically are the most carbon-intensive travel methods.

The Carbon Footprint of Major Travel Methods

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Did you know that transport accounts for nearly one-quarter of global energy-related carbon dioxide (CO₂) emissions?

This graphic illustrates the carbon footprints of major travel methods measured in grams of carbon dioxide equivalent (CO₂e) emitted per person to travel one kilometer. This includes both CO₂ and other greenhouse gases.

Data is sourced from Our World in Data, the UK Government’s Department for Energy Security and Net Zero, and The International Council on Clean Transportation, as of December 2022.

These figures should be interpreted as approximations, rather than exact numbers. There are many variables at play that determine the actual carbon footprint in any individual case, including vehicle type or model, occupancy, energy mix, and even weather.

Cruise Ships are the Most Carbon-Intensive Travel Method

According to these estimates, taking a cruise ship, flying domestically, and driving alone are some of the most carbon-intensive travel methods.

Cruise ships typically use heavy fuel oil, which is high in carbon content. The average cruise ship weighs between 70,000 to 180,000 metric tons, meaning they require large engines to get moving.

These massive vessels must also generate power for onboard amenities such as lighting, air conditioning, and entertainment systems.

Short-haul flights are also considered carbon-intensive due to the significant amount of fuel consumed during initial takeoff and climbing altitude, relative to a lower amount of cruising.

| Transportation method | CO₂ equivalent emissions per passenger km |

|---|---|

| Cruise Ship | 250 |

| Short-haul flight (i.e. within a U.S. state or European country) | 246 |

| Diesel car | 171 |

| Gas car | 170 |

| Medium-haul flight (i.e. international travel within Europe, or between U.S. states) | 151 |

| Long-haul flight (over 3,700 km, about the distance from LA to NY) | 147 |

| Motorbike | 113 |

| Bus (average) | 96 |

| Plug-in hybrid | 68 |

| Electric car | 47 |

| National rail | 35 |

| Tram | 28 |

| London Underground | 27 |

| Ferry (foot passenger) | 19 |

| Eurostar (International rail) | 4.5 |

Are EVs Greener?

Many experts agree that EVs produce a lower carbon footprint over time versus traditional internal combustion engine (ICE) vehicles.

However, the batteries in electric vehicles charge on the power that comes straight off the electrical grid—which in many places may be powered by fossil fuels. For that reason, the carbon footprint of an EV will depend largely on the blend of electricity sources used for charging.

There are also questions about how energy-intensive it is to build EVs compared to a comparable ICE vehicle.

-

Debt1 week ago

Debt1 week agoHow Debt-to-GDP Ratios Have Changed Since 2000

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Countries2 weeks ago

Countries2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries

-

United States2 weeks ago

United States2 weeks agoWhere U.S. Inflation Hit the Hardest in March 2024

-

Green2 weeks ago

Green2 weeks agoTop Countries By Forest Growth Since 2001

-

United States2 weeks ago

United States2 weeks agoRanked: The Largest U.S. Corporations by Number of Employees