Datastream

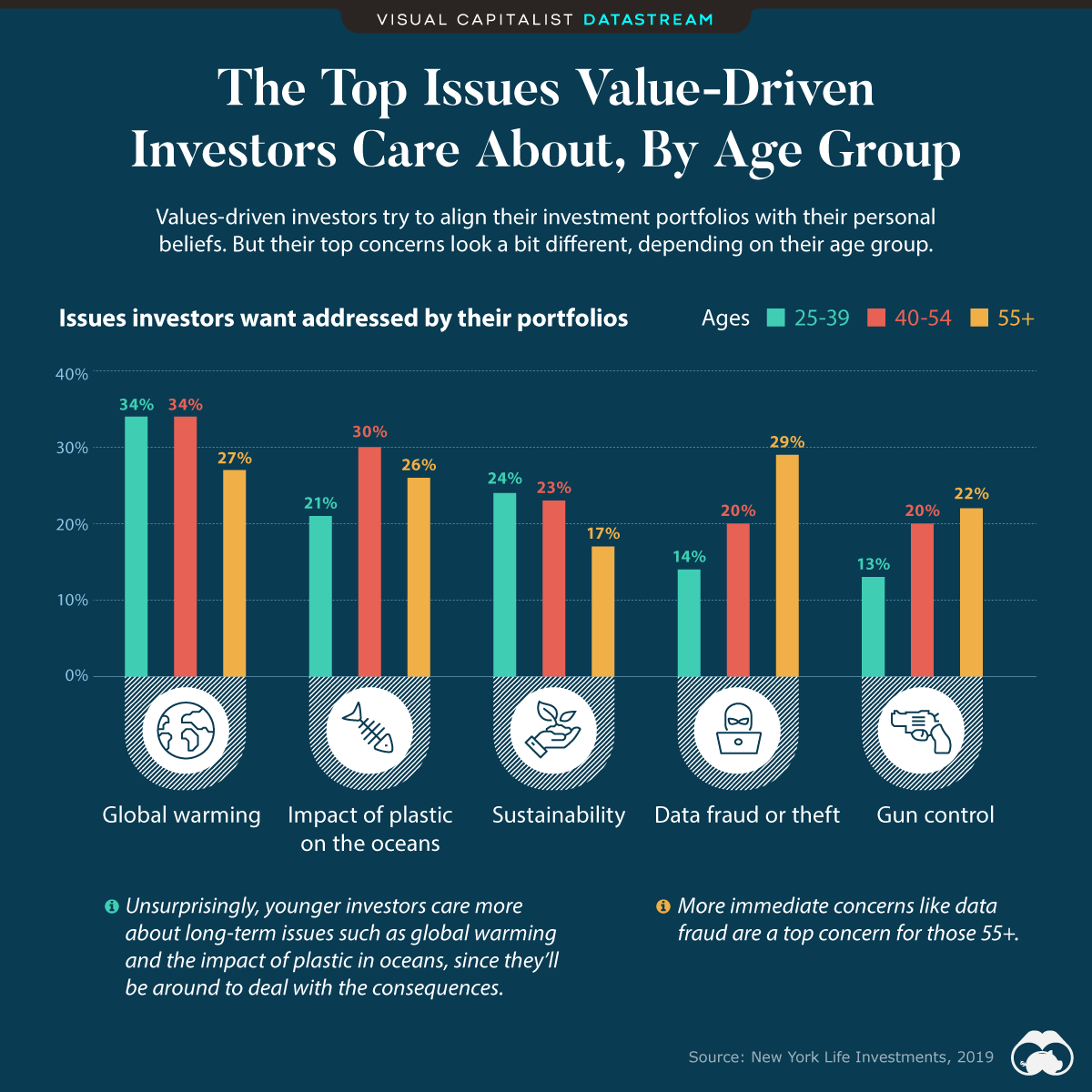

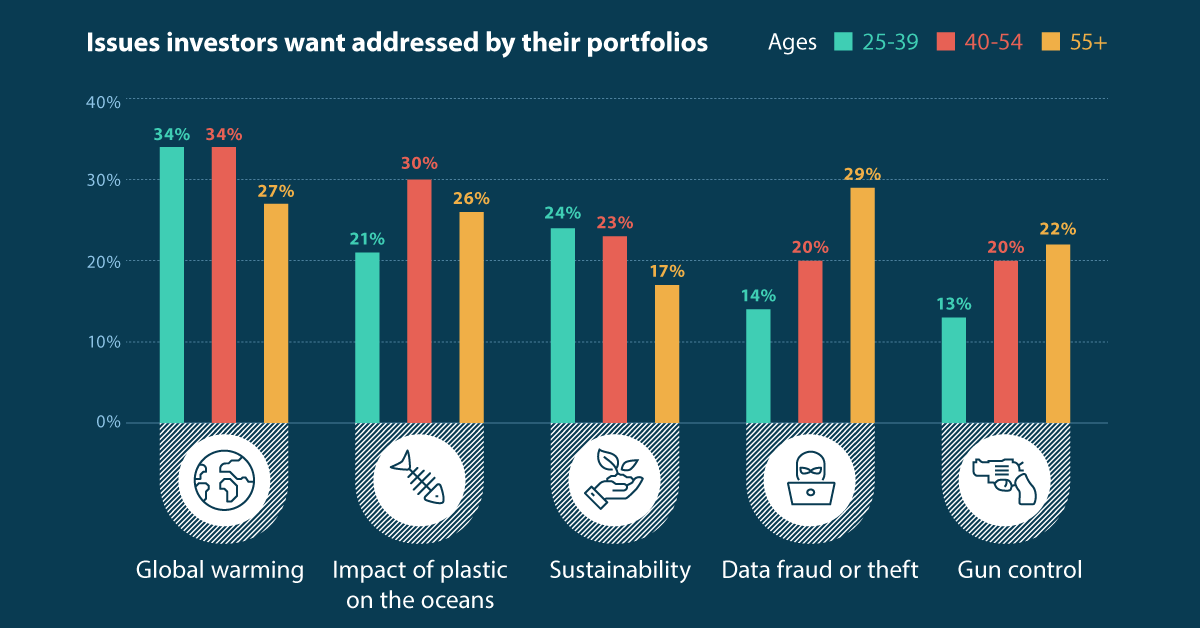

What Issues Do Values-Driven Investors Care About?

The Briefing

- Values-driven investing has become popular across a variety of age groups

- However, different age groups value different issues over others

- Young investors (age 25-39) are most concerned about climate change and plastic in the ocean

- In contrast, investors aged 55+ care more about data fraud and gun control

What Issues Do Values-Driven Investors Care About?

Contrary to popular belief, environmental, social, and governance (ESG) investing isn’t just for the younger generation.

In fact, more than 80% of investors aged 40+ are interested in aligning their investment portfolios with their personal values, which is only around 10 percentage points less than the younger demographic (aged 25-39).

However, while overall intent to invest in the greater good is consistent across the board, the top concerns among investors vary, depending on age.

Here’s a look at the top issues that investors want addressed in their portfolios, by age group:

| Age Group | |||

|---|---|---|---|

| Issues Investors Want Included in Their Portfolio | 25-39 years old | 40-54 years old | 55+ years old |

| Global warming/ climate change | 34% | 34% | 27% |

| Impact of plastic on the oceans | 21% | 30% | 26% |

| Sustainability | 24% | 23% | 17% |

| Data fraud or theft | 14% | 20% | 29% |

| Gun control | 13% | 20% | 22% |

Young Investors Care More About Long-Term Issues

As the table above shows, the top concern among investors aged 25-39 is climate change, followed by sustainability in general.

This makes sense, considering that younger investors will most likely be around to deal with the consequences of long-term issues like climate change and plastic pollution.

In contrast, investors with a shorter time horizon to retirement (aged 55+) are more concerned with immediate threats like gun control and data fraud.

How To Execute on Values-Driven Investments

It’s clear that investors of all ages are interested in values-driven investing—but how can investors take action to build a portfolio that reflects their beliefs?

There are two approaches to building a sustainable investment portfolio:

- Exclusionary investing

Also known as negative screening, or divesting. This is when investors screen out industries that go against their values, such as tobacco, gambling, or fossil fuels. - Inclusionary investing

Also knowns as positive screening. This is when investors formally consider ESG factors in their research process under the assumption that companies with strong sustainability practices can outperform their industry peers over time.

While exclusionary investing is the more common approach, research on the effectiveness of inclusionary investing has been overwhelmingly positive.

» For a more in-depth look on the top of values driven investing, read our full article The Rise of the Values-Driven Investor

Where does this data come from?

Source: New York Life, 2019.

Notes: Data was derived from a 2019 study conducted by New York Life Investments,

in partnership with RTi Research.

Datastream

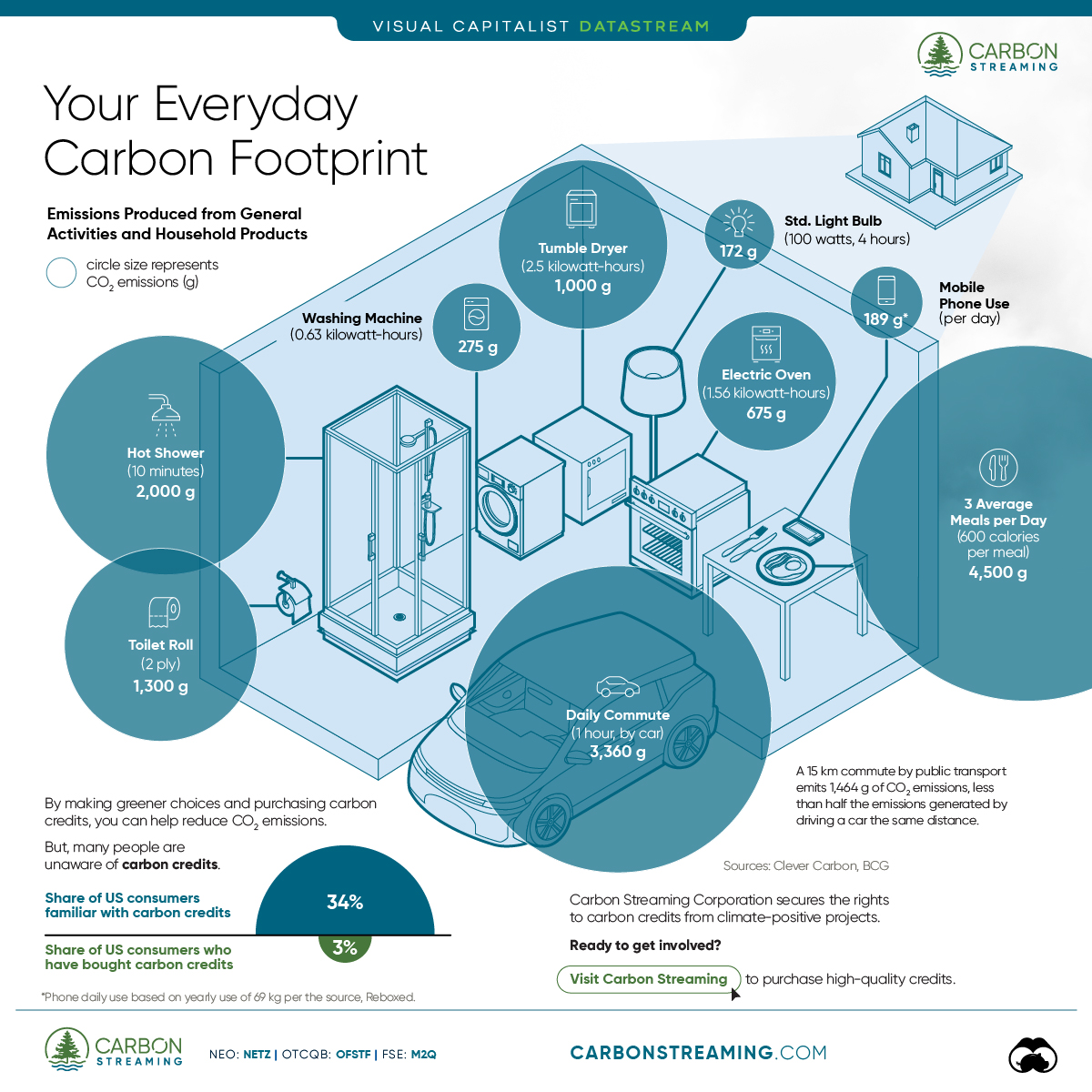

Can You Calculate Your Daily Carbon Footprint?

Discover how the average person’s carbon footprint impacts the environment and learn how carbon credits can offset your carbon footprint.

The Briefing

- A person’s carbon footprint is substantial, with activities such as food consumption creating as much as 4,500 g of CO₂ emissions daily.

- By purchasing carbon credits from Carbon Streaming Corporation, you can offset your own emissions and fund positive climate action.

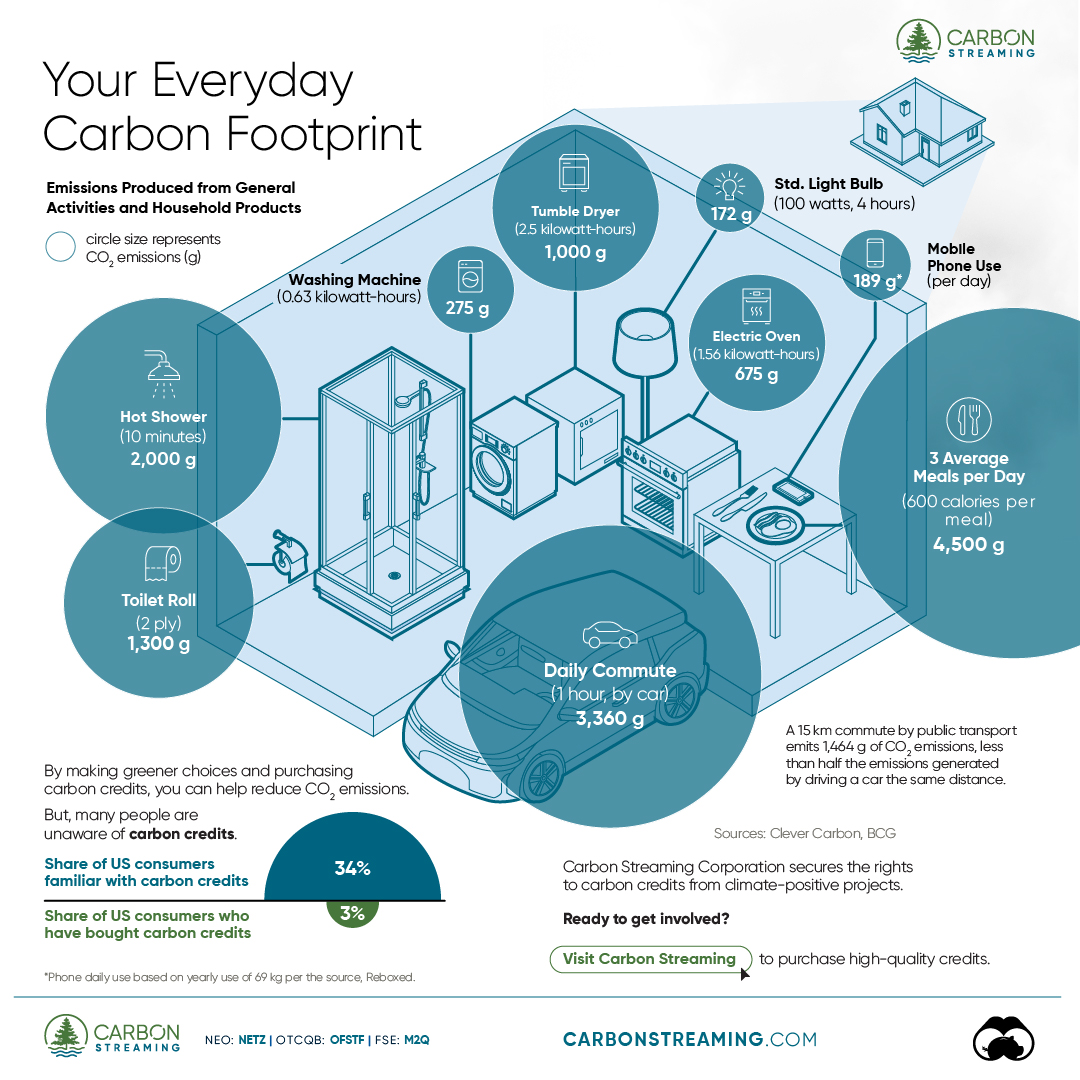

Your Everyday Carbon Footprint

While many large businesses and countries have committed to net-zero goals, it is essential to acknowledge that your everyday activities also contribute to global emissions.

In this graphic, sponsored by Carbon Streaming Corporation, we will explore how the choices we make and the products we use have a profound impact on our carbon footprint.

Carbon Emissions by Activity

Here are some of the daily activities and products of the average person and their carbon footprint, according to Clever Carbon.

| Household Activities & Products | CO2 Emissions (g) |

|---|---|

| 💡 Standard Light Bulb (100 watts, four hours) | 172 g |

| 📱 Mobile Phone Use (195 minutes per day)* | 189 g |

| 👕 Washing Machine (0.63 kWh) | 275 g |

| 🔥 Electric Oven (1.56 kWh) | 675 g |

| ♨️ Tumble Dryer (2.5 kWh) | 1,000 g |

| 🧻 Toilet Roll (2 ply) | 1,300 g |

| 🚿 Hot Shower (10 mins) | 2,000 g |

| 🚙 Daily Commute (one hour, by car) | 3,360 g |

| 🍽️ Average Daily Food Consumption (three meals of 600 calories) | 4,500 g |

| *Phone use based on yearly use of 69kg per the source, Reboxed | |

Your choice of transportation plays a crucial role in determining your carbon footprint. For instance, a 15 km daily commute to work on public transport generates an average of 1,464 g of CO₂ emissions. Compared to 3,360 g—twice the volume for a journey the same length by car.

By opting for more sustainable modes of transport, such as cycling, walking, or public transportation, you can significantly reduce your carbon footprint.

Addressing Your Carbon Footprint

One way to compensate for your emissions is by purchasing high-quality carbon credits.

Carbon credits are used to help fund projects that avoid, reduce or remove CO₂ emissions. This includes nature-based solutions such as reforestation and improved forest management, or technology-based solutions such as the production of biochar and carbon capture and storage (CCS).

While carbon credits offer a potential solution for individuals to help reduce global emissions, public awareness remains a significant challenge. A BCG-Patch survey revealed that only 34% of U.S. consumers are familiar with carbon credits, and only 3% have purchased them in the past.

About Carbon Streaming

By financing the creation or expansion of carbon projects, Carbon Streaming Corporation secures the rights to future carbon credits generated by these sustainable projects. You can then purchase these carbon credits to help fund climate solutions around the world and compensate for your own emissions.

Ready to get involved?

>> Learn more about purchasing carbon credits at Carbon Streaming

-

Mining1 week ago

Mining1 week agoGold vs. S&P 500: Which Has Grown More Over Five Years?

-

Markets2 weeks ago

Markets2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Countries2 weeks ago

Countries2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries