Markets

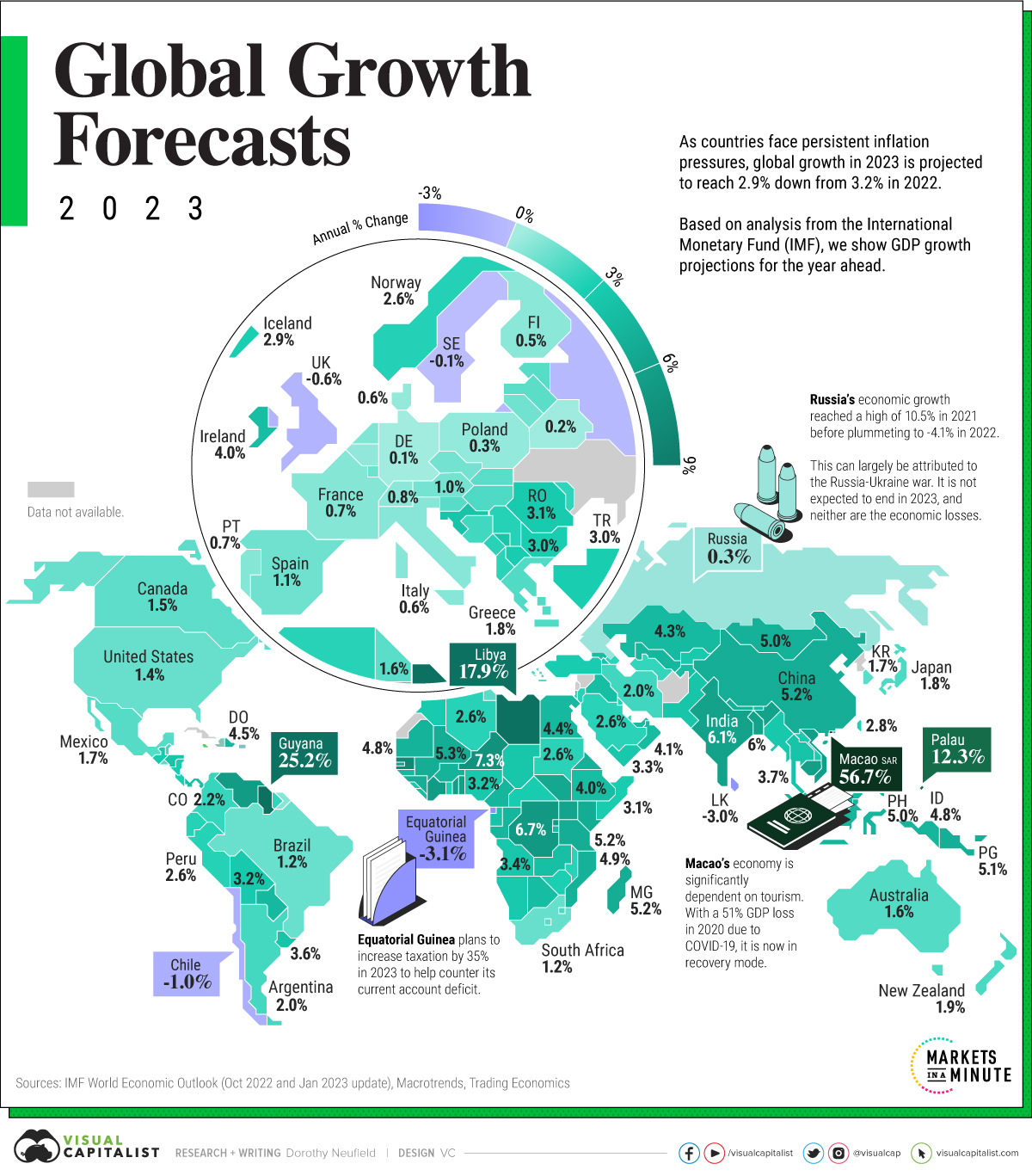

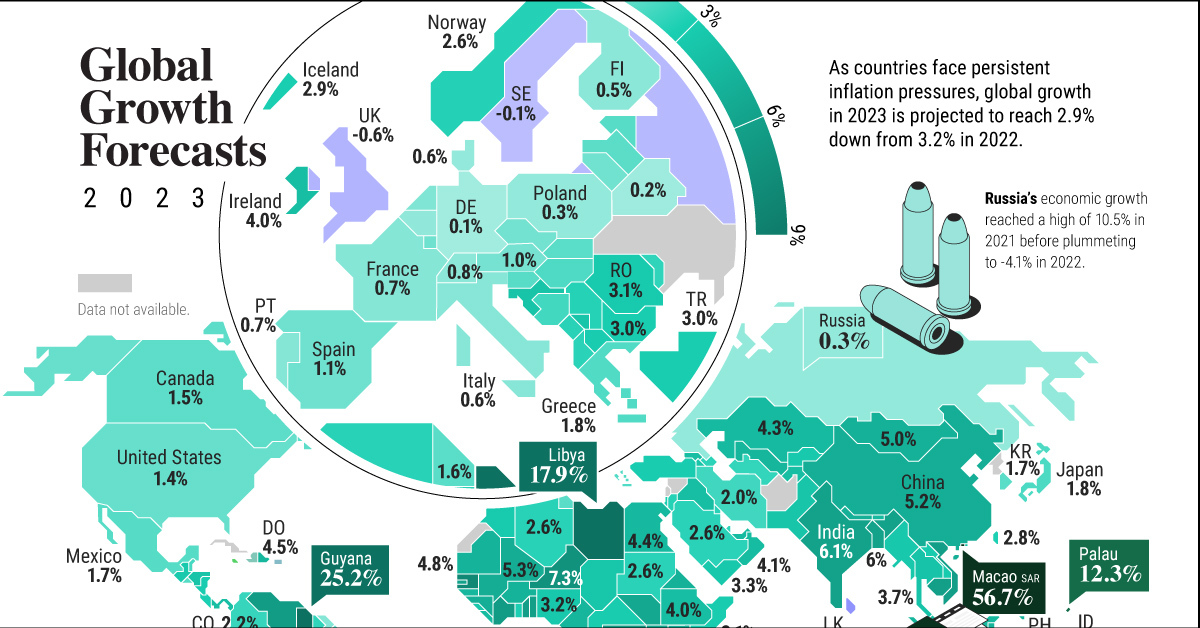

Mapped: GDP Growth Forecasts by Country, in 2023

Mapped: GDP Growth Forecasts by Country, in 2023

This was originally posted on Advisor Channel. Sign up to the free mailing list to get beautiful visualizations on financial markets that help advisors and their clients.

Since Russia’s invasion of Ukraine early last year, talk of global recession has dominated the outlook for 2023.

High inflation, spurred by rising energy costs, has tested GDP growth. Tightening monetary policy in the U.S., with interest rates jumping from roughly 0% to over 4% in 2022, has historically preceded a downturn about one to two years later.

For European economies, energy prices are critical. The good news is that prices have fallen recently since March highs, but the continent remains on shaky ground.

The above infographic maps GDP growth forecasts by country for the year ahead, based on projections from the International Monetary Fund (IMF) October 2022 Outlook and January 2023 update.

2023 GDP Growth Outlook

The world economy is projected to see just 2.9% GDP growth in 2023, down from 3.2% projected for 2022.

This is a 0.2% increase since the October 2022 Outlook thanks in part to China’s reopening, higher global demand, and slowing inflation projected across certain countries in the year ahead.

With this in mind, we show GDP growth forecasts for 191 jurisdictions given multiple economic headwinds—and a few emerging bright spots in 2023.

| Country / Region | 2023 Real GDP % Change (Projected) |

|---|---|

| 🇦🇱 Albania | 2.5% |

| 🇩🇿 Algeria | 2.6% |

| 🇦🇴 Angola | 3.4% |

| 🇦🇬 Antigua and Barbuda | 5.6% |

| 🇦🇷 Argentina* | 2.0% |

| 🇦🇲 Armenia | 3.5% |

| 🇦🇼 Aruba | 2.0% |

| 🇦🇺 Australia* | 1.6% |

| 🇦🇹 Austria | 1.0% |

| 🇦🇿 Azerbaijan | 2.5% |

| 🇧🇭 Bahrain | 3.0% |

| 🇧🇩 Bangladesh | 6.0% |

| 🇧🇧 Barbados | 5.0% |

| 🇧🇾 Belarus | 0.2% |

| 🇧🇪 Belgium | 0.4% |

| 🇧🇿 Belize | 2.0% |

| 🇧🇯 Benin | 6.2% |

| 🇧🇹 Bhutan | 4.3% |

| 🇧🇴 Bolivia | 3.2% |

| 🇧🇦 Bosnia and Herzegovina | 2.0% |

| 🇧🇼 Botswana | 4.0% |

| 🇧🇷 Brazil* | 1.2% |

| 🇧🇳 Brunei Darussalam | 3.3% |

| 🇧🇬 Bulgaria | 3.0% |

| 🇧🇫 Burkina Faso | 4.8% |

| 🇧🇮 Burundi | 4.1% |

| 🇨🇻 Cabo Verde | 4.8% |

| 🇨🇲 Cameroon | 4.6% |

| 🇰🇭 Cambodia | 6.2% |

| 🇨🇦 Canada* | 1.5% |

| 🇨🇫 Central African Republic | 3.0% |

| 🇹🇩 Chad | 3.4% |

| 🇨🇱 Chile | -1.0% |

| 🇨🇳 China* | 5.3% |

| 🇨🇴 Colombia | 2.2% |

| 🇰🇲 Comoros | 3.4% |

| 🇨🇷 Costa Rica | 2.9% |

| 🇨🇮 Côte d'Ivoire | 6.5% |

| 🇭🇷 Croatia | 3.5% |

| 🇨🇾 Cyprus | 2.5% |

| 🇨🇿 Czech Republic | 1.5% |

| 🇨🇩 Democratic Republic of the Congo | 6.7% |

| 🇩🇰 Denmark | 0.6% |

| 🇩🇯 Djibouti | 5.0% |

| 🇩🇲 Dominica | 4.9% |

| 🇩🇴 Dominican Republic | 4.5% |

| 🇪🇨 Ecuador | 2.7% |

| 🇪🇬 Egypt* | 4.0% |

| 🇸🇻 El Salvador | 1.7% |

| 🇬🇶 Equatorial Guinea | -3.1% |

| 🇪🇷 Eritrea | 2.9% |

| 🇪🇪 Estonia | 1.8% |

| 🇸🇿 Eswatini | 1.8% |

| 🇪🇹 Ethiopia | 5.3% |

| 🇫🇯 Fiji | 6.9% |

| 🇫🇮 Finland | 0.5% |

| 🇫🇷 France* | 0.7% |

| 🇲🇰 North Macedonia | 3.0% |

| 🇬🇦 Gabon | 3.7% |

| Georgia | 4.0% |

| Germany* | 0.1% |

| Ghana | 2.8% |

| Greece | 1.8% |

| Grenada | 3.6% |

| Guatemala | 3.2% |

| Guinea | 5.1% |

| Guinea-Bissau | 4.5% |

| Guyana | 25.2% |

| Haiti | 0.5% |

| Honduras | 3.5% |

| Hong Kong SAR | 3.9% |

| Hungary | 1.8% |

| Iceland | 2.9% |

| India* | 6.1% |

| Indonesia* | 4.8% |

| Iraq | 4.0% |

| Ireland | 4.0% |

| Iran* | 2.0% |

| Israel | 3.0% |

| Italy* | 0.6% |

| Jamaica | 3.0% |

| Japan* | 1.8% |

| Jordan | 2.7% |

| Kazakhstan* | 4.3% |

| Kenya | 5.1% |

| Kiribati | 2.4% |

| South Korea* | 1.7% |

| Kosovo | 3.5% |

| Kuwait | 2.6% |

| Kyrgyz Republic | 3.2% |

| Lao P.D.R. | 3.1% |

| Latvia | 1.6% |

| Lesotho | 1.6% |

| Liberia | 4.2% |

| Libya | 17.9% |

| Lithuania | 1.1% |

| Luxembourg | 1.1% |

| Macao SAR | 56.7% |

| Madagascar | 5.2% |

| 🇲🇼 Malawi | 2.5% |

| 🇲🇾 Malaysia* | 4.4% |

| 🇲🇻 Maldives | 6.1% |

| 🇲🇱 Mali | 5.3% |

| 🇲🇹 Malta | 3.3% |

| 🇲🇭 Marshall Islands | 3.2% |

| 🇲🇷 Mauritania | 4.8% |

| 🇲🇺 Mauritius | 5.4% |

| 🇲🇽 Mexico* | 1.7% |

| 🇫🇲 Micronesia | 2.9% |

| 🇲🇩 Moldova | 2.3% |

| 🇲🇳 Mongolia | 5.0% |

| 🇲🇪 Montenegro | 2.5% |

| 🇲🇦 Morocco | 3.1% |

| 🇲🇿 Mozambique | 4.9% |

| 🇲🇲 Myanmar | 3.3% |

| 🇳🇦 Namibia | 3.2% |

| 🇳🇷 Nauru | 2.0% |

| 🇳🇵 Nepal | 5.0% |

| 🇳🇱 Netherlands* | 0.6% |

| 🇳🇿 New Zealand | 1.9% |

| 🇳🇮 Nicaragua | 3.0% |

| 🇳🇪 Niger | 7.3% |

| 🇳🇬 Nigeria* | 3.2% |

| 🇳🇴 Norway | 2.6% |

| 🇴🇲 Oman | 4.1% |

| 🇵🇰 Pakistan* | 2.0% |

| 🇵🇼 Palau | 12.3% |

| 🇵🇦 Panama | 4.0% |

| 🇵🇬 Papua New Guinea | 5.1% |

| 🇵🇾 Paraguay | 4.3% |

| 🇵🇪 Peru | 2.6% |

| 🇵🇭 Philippines* | 5.0% |

| 🇵🇱 Poland* | 0.3% |

| 🇵🇹 Portugal | 0.7% |

| 🇵🇷 Puerto Rico | 0.4% |

| 🇶🇦 Qatar | 2.4% |

| 🇨🇬 Republic of Congo | 4.6% |

| 🇷🇴 Romania | 3.1% |

| 🇷🇺 Russia* | 0.3% |

| 🇷🇼 Rwanda | 6.7% |

| 🇼🇸 Samoa | 4.0% |

| 🇸🇲 San Marino | 0.8% |

| 🇸🇹 São Tomé and Príncipe | 2.6% |

| 🇸🇦 Saudi Arabia* | 2.6% |

| 🇸🇳 Senegal | 8.1% |

| 🇷🇸 Serbia | 2.7% |

| 🇸🇨 Seychelles | 5.2% |

| 🇸🇱 Sierra Leone | 3.3% |

| 🇸🇬 Singapore | 2.3% |

| 🇸🇰 Slovak Republic | 1.5% |

| 🇸🇮 Slovenia | 1.7% |

| 🇸🇧 Solomon Islands | 2.6% |

| 🇸🇴 Somalia | 3.1% |

| 🇿🇦 South Africa* | 1.2% |

| 🇸🇸 South Sudan | 5.6% |

| 🇪🇸 Spain* | 1.1% |

| 🇱🇰 Sri Lanka | -3.0% |

| 🇰🇳 St. Kitts and Nevis | 4.8% |

| 🇱🇨 St. Lucia | 5.8% |

| 🇻🇨 St. Vincent and the Grenadines | 6.0% |

| 🇸🇩 Sudan | 2.6% |

| 🇸🇷 Suriname | 2.3% |

| 🇸🇪 Sweden | -0.1% |

| 🇨🇭 Switzerland | 0.8% |

| 🇹🇼 Taiwan | 2.8% |

| 🇹🇯 Tajikistan | 4.0% |

| 🇹🇿 Tanzania | 5.2% |

| 🇹🇭 Thailand* | 3.7% |

| 🇧🇸 The Bahamas | 4.1% |

| 🇬🇲 The Gambia | 6.0% |

| 🇹🇱 Timor-Leste | 4.2% |

| 🇹🇬 Togo | 6.2% |

| 🇹🇴 Tonga | 2.9% |

| 🇹🇹 Trinidad and Tobago | 3.5% |

| 🇹🇳 Tunisia | 1.6% |

| 🇹🇷 Turkey* | 3.0% |

| 🇹🇲 Turkmenistan | 2.3% |

| 🇹🇻 Tuvalu | 3.5% |

| 🇺🇬 Uganda | 5.9% |

| 🇺🇦 Ukraine | N/A |

| 🇦🇪 United Arab Emirates | 4.2% |

| 🇬🇧 United Kingdom* | -0.6% |

| 🇺🇲 U.S.* | 1.4% |

| 🇺🇾 Uruguay | 3.6% |

| 🇺🇿 Uzbekistan | 4.7% |

| 🇻🇺 Vanuatu | 3.1% |

| 🇻🇪 Venezuela | 6.5% |

| 🇻🇳 Vietnam | 6.2% |

| West Bank and Gaza | 3.5% |

| 🇾🇪 Yemen | 3.3% |

| 🇿🇲 Zambia | 4.0% |

| 🇿🇼 Zimbabwe | 2.8% |

*Reflect updated figures from the January 2023 IMF Update.

The U.S. is forecast to see 1.4% GDP growth in 2023, up from 1.0% seen in the last October projection.

Still, signs of economic weakness can be seen in the growing wave of tech layoffs, foreshadowed as a white-collar or ‘Patagonia-vest’ recession. Last year, 88,000 tech jobs were cut and this trend has continued into 2023. Major financial firms have also followed suit. Still, unemployment remains fairly steadfast, at 3.5% as of December 2022. Going forward, concerns remain around inflation and the path of interest rate hikes, though both show signs of slowing.

Across Europe, the average projected GDP growth rate is 0.7% for 2023, a sharp decline from the 2.1% forecast for last year.

Both Germany and Italy are forecast to see slight growth, at 0.1% and 0.6%, respectively. Growth forecasts were revised upwards since the IMF’s October release. However, an ongoing energy crisis exposes the manufacturing sector to vulnerabilities, with potential spillover effects to consumers and businesses, and overall Euro Area growth.

China remains an open question. In 2023, growth is predicted to rise 5.2%, higher than many large economies. While its real estate sector has shown signs of weakness, the recent opening on January 8th, following 1,016 days of zero-Covid policy, could boost demand and economic activity.

A Long Way to Go

The IMF has stated that 2023 will feel like a recession for much of the global economy. But whether it is headed for a recovery or a sharper decline remains unknown.

Today, two factors propping up the global economy are lower-than-expected energy prices and resilient private sector balance sheets. European natural gas prices have sunk to levels seen before the war in Ukraine. During the height of energy shocks, firms showed a notable ability to withstand astronomical energy prices squeezing their finances. They are also sitting on significant cash reserves.

On the other hand, inflation is far from over. To counter this effect, many central banks will have to use measures to rein in prices. This may in turn have a dampening effect on economic growth and financial markets, with unknown consequences.

As economic data continues to be released over the year, there may be a divergence between consumer sentiment and whether things are actually changing in the economy. Where the economy is heading in 2023 will be anyone’s guess.

Markets

The European Stock Market: Attractive Valuations Offer Opportunities

On average, the European stock market has valuations that are nearly 50% lower than U.S. valuations. But how can you access the market?

European Stock Market: Attractive Valuations Offer Opportunities

Europe is known for some established brands, from L’Oréal to Louis Vuitton. However, the European stock market offers additional opportunities that may be lesser known.

The above infographic, sponsored by STOXX, outlines why investors may want to consider European stocks.

Attractive Valuations

Compared to most North American and Asian markets, European stocks offer lower or comparable valuations.

| Index | Price-to-Earnings Ratio | Price-to-Book Ratio |

|---|---|---|

| EURO STOXX 50 | 14.9 | 2.2 |

| STOXX Europe 600 | 14.4 | 2 |

| U.S. | 25.9 | 4.7 |

| Canada | 16.1 | 1.8 |

| Japan | 15.4 | 1.6 |

| Asia Pacific ex. China | 17.1 | 1.8 |

Data as of February 29, 2024. See graphic for full index names. Ratios based on trailing 12 month financials. The price to earnings ratio excludes companies with negative earnings.

On average, European valuations are nearly 50% lower than U.S. valuations, potentially offering an affordable entry point for investors.

Research also shows that lower price ratios have historically led to higher long-term returns.

Market Movements Not Closely Connected

Over the last decade, the European stock market had low-to-moderate correlation with North American and Asian equities.

The below chart shows correlations from February 2014 to February 2024. A value closer to zero indicates low correlation, while a value of one would indicate that two regions are moving in perfect unison.

| EURO STOXX 50 | STOXX EUROPE 600 | U.S. | Canada | Japan | Asia Pacific ex. China |

|

|---|---|---|---|---|---|---|

| EURO STOXX 50 | 1.00 | 0.97 | 0.55 | 0.67 | 0.24 | 0.43 |

| STOXX EUROPE 600 | 1.00 | 0.56 | 0.71 | 0.28 | 0.48 | |

| U.S. | 1.00 | 0.73 | 0.12 | 0.25 | ||

| Canada | 1.00 | 0.22 | 0.40 | |||

| Japan | 1.00 | 0.88 | ||||

| Asia Pacific ex. China | 1.00 |

Data is based on daily USD returns.

European equities had relatively independent market movements from North American and Asian markets. One contributing factor could be the differing sector weights in each market. For instance, technology makes up a quarter of the U.S. market, but health care and industrials dominate the broader European market.

Ultimately, European equities can enhance portfolio diversification and have the potential to mitigate risk for investors.

Tracking the Market

For investors interested in European equities, STOXX offers a variety of flagship indices:

| Index | Description | Market Cap |

|---|---|---|

| STOXX Europe 600 | Pan-regional, broad market | €10.5T |

| STOXX Developed Europe | Pan-regional, broad-market | €9.9T |

| STOXX Europe 600 ESG-X | Pan-regional, broad market, sustainability focus | €9.7T |

| STOXX Europe 50 | Pan-regional, blue-chip | €5.1T |

| EURO STOXX 50 | Eurozone, blue-chip | €3.5T |

Data is as of February 29, 2024. Market cap is free float, which represents the shares that are readily available for public trading on stock exchanges.

The EURO STOXX 50 tracks the Eurozone’s biggest and most traded companies. It also underlies one of the world’s largest ranges of ETFs and mutual funds. As of November 2023, there were €27.3 billion in ETFs and €23.5B in mutual fund assets under management tracking the index.

“For the past 25 years, the EURO STOXX 50 has served as an accurate, reliable and tradable representation of the Eurozone equity market.”

— Axel Lomholt, General Manager at STOXX

Partnering with STOXX to Track the European Stock Market

Are you interested in European equities? STOXX can be a valuable partner:

- Comprehensive, liquid and investable ecosystem

- European heritage, global reach

- Highly sophisticated customization capabilities

- Open architecture approach to using data

- Close partnerships with clients

- Part of ISS STOXX and Deutsche Börse Group

With a full suite of indices, STOXX can help you benchmark against the European stock market.

Learn how STOXX’s European indices offer liquid and effective market access.

-

Economy2 days ago

Economy2 days agoEconomic Growth Forecasts for G7 and BRICS Countries in 2024

The IMF has released its economic growth forecasts for 2024. How do the G7 and BRICS countries compare?

-

Markets1 week ago

Markets1 week agoU.S. Debt Interest Payments Reach $1 Trillion

U.S. debt interest payments have surged past the $1 trillion dollar mark, amid high interest rates and an ever-expanding debt burden.

-

United States2 weeks ago

United States2 weeks agoRanked: The Largest U.S. Corporations by Number of Employees

We visualized the top U.S. companies by employees, revealing the massive scale of retailers like Walmart, Target, and Home Depot.

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

This graphic shows the states with the highest real GDP growth rate in 2023, largely propelled by the oil and gas boom.

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

In this graphic, we show the highest earning flight routes globally as air travel continued to rebound in 2023.

-

Markets3 weeks ago

Markets3 weeks agoRanked: The Most Valuable Housing Markets in America

The U.S. residential real estate market is worth a staggering $47.5 trillion. Here are the most valuable housing markets in the country.

-

Education1 week ago

Education1 week agoHow Hard Is It to Get Into an Ivy League School?

-

Technology2 weeks ago

Technology2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Ranked: The World’s Top Flight Routes, by Revenue

-

Demographics2 weeks ago

Demographics2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

The Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries

-

Economy2 weeks ago

Economy2 weeks agoWhere U.S. Inflation Hit the Hardest in March 2024

-

Green2 weeks ago

Green2 weeks agoTop Countries By Forest Growth Since 2001