Money

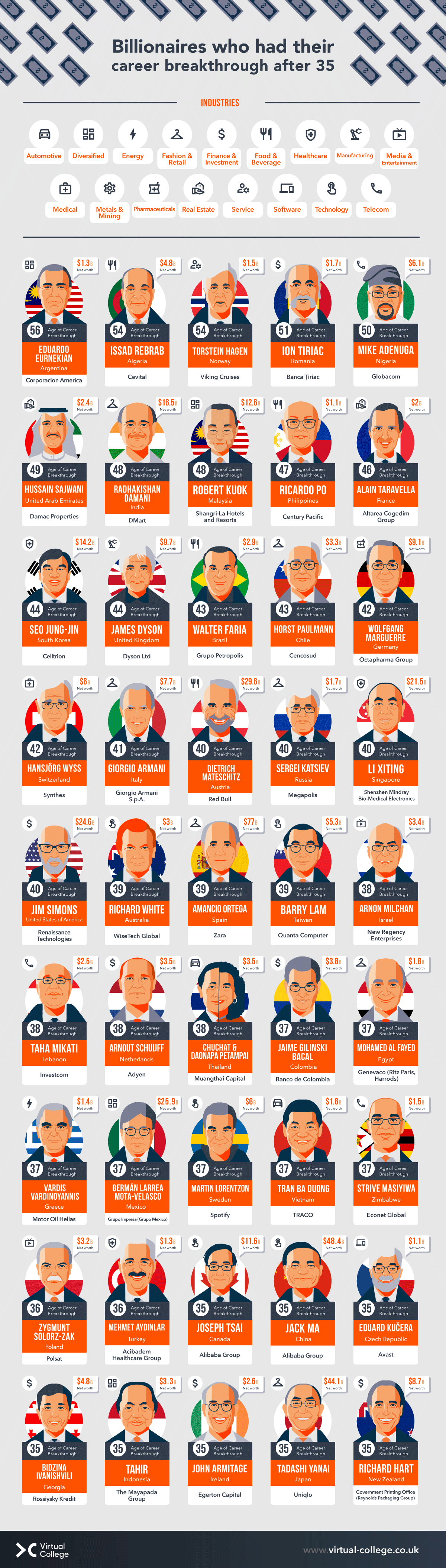

Billionaire Late Bloomers, by Age of Their Breakthrough

Billionaire Late Bloomers, by Age of Breakthrough

More often than not, individuals and media alike focus on the success stories of early bloomers.

These early-age accomplishments of some of the richest people in the world are highlighted as marvels. The early achievements of hoodie-wearing CEOs like Mark Zuckerberg or Evan Spiegel—who became billionaires at ages 23 and 25, respectively—come to mind.

But there’s also the case to be made for the late bloomer. According to the Census Bureau, a 35-year-old is three times more likely to found a successful start-up than someone aged 22.

The infographic above, from Virtual College, highlights 45 billionaires who had their breakthrough later in life, by the age of their respective breakthrough.

Billionaires With Career Breakthroughs at or After Age 35

Though these late successes span many different industries and countries, there are many consistent through lines.

The 45 billionaires highlighted had an average age of 41 and an average net worth of $10 billion.

| Billionaire | Company | Age of Breakthrough | Net Worth ($B) | Nationality |

|---|---|---|---|---|

| Eduardo Eurnekian | Corporacion America | 56 | $1.3 | 🇦🇷 Argentina |

| Issad Rebrab | Cevital | 54 | $4.8 | 🇩🇿 Algeria |

| Torstein Hagen | Viking Cruises | 54 | $1.5 | 🇳🇴 Norway |

| Ion Tiriac | Banca Tiriac | 51 | $1.7 | 🇷🇴 Romania |

| Mike Adenuga | Globacom | 50 | $6.1 | 🇳🇬 Nigeria |

| Hussain Sajwani | Damac Properties | 49 | $2.4 | 🇦🇪 UAE |

| Radhakishan Damani | Dmart | 48 | $16.5 | 🇮🇳 India |

| Robert Kuok | Shangra-La Hotels and Resorts | 48 | $12.6 | 🇲🇾 Malaysia |

| Ricardo Po | Century Pacific | 47 | $1.1 | 🇵🇭 Philippines |

| Alain Tarvella | Altarea Cogedim Group | 46 | $2.0 | 🇫🇷 France |

| Seo Jung-Jin | Celltrion | 44 | $14.2 | 🇰🇷 South Korea |

| James Dyson | Dyson Ltd | 44 | $9.7 | 🇬🇧 UK |

| Walter Faria | Grupo Petropolis | 43 | $2.9 | 🇧🇷 Brazil |

| Horst Paulmann | Cencosud | 43 | $3.3 | 🇨🇱 Chile |

| Wolfgang Marguerre | Octapharma Group | 42 | $9.1 | 🇩🇪 Germany |

| Hansjorg Wyss | Synthes | 42 | $6.0 | 🇨🇭Switzerland |

| Giorgio Armani | Giorgio Armani S.p.A. | 41 | $7.7 | 🇮🇹 Italy |

| Dietrich Mateschitz | Red Bull | 40 | $29.6 | 🇦🇹 Austria |

| Sergei Katsiev | Megapolis | 40 | $1.7 | 🇷🇺 Russia |

| Li Xiting | Shenzhen Mindray Bio-Medical Electronics | 40 | $21.5 | 🇸🇬 Singapore |

| Jim Simmons | Renaissance Technologies | 40 | $24.6 | 🇺🇸 U.S. |

| Richard White | WiseTech Global | 39 | $3.5 | 🇦🇺 Australia |

| Amancio Ortega | Zara | 39 | $77 | 🇪🇸 Spain |

| Barry Lam | Quanta Computer | 39 | $5.3 | 🇹🇼 Taiwan |

| Arnon Milchan | New Regency Enterprises | 38 | $3.4 | 🇮🇱 Israel |

| Taha Mikati | Investcom | 38 | $2.5 | 🇱🇧 Lebanon |

| Arnout Schuijff | Adyen | 38 | $3.5 | 🇳🇱 Netherlands |

| Chuchat & Daonapa Petampai | Muangthai Capital | 38 | $3.5 | 🇹🇭 Thailand |

| Jaime Gilinski Bacal | Banco De Colombia | 37 | $3.8 | 🇨🇴 Colombia |

| Mohamed Al Fayed | Genevaco (Ritz Paris, Harrods) | 37 | $1.8 | 🇪🇬 Egypt |

| Vardis Vardinyannis | Motor Oil Hellas | 37 | $1.4 | 🇬🇷 Greece |

| German Larrea Mota-Velasco | Grupo Mexico | 37 | $25.9 | 🇲🇽 Mexico |

| Martin Lorentzon | Spotify | 37 | $6.0 | 🇸🇪 Sweden |

| Tran Ba Duong | Traco | 37 | $1.6 | 🇻🇳 Vietnam |

| Strive Masiyiwa | Econet Global | 37 | $1.5 | 🇿🇼 Zimbabwe |

| Zygmunt Solorz-Zak | Polsat | 36 | $3.2 | 🇵🇱 Poland |

| Mehmet Aydinlar | Acibadem Healthcare Group | 36 | $1.3 | 🇹🇷 Turkey |

| Joseph Tsai | Alibaba Group | 35 | $11.6 | 🇨🇦 Canada |

| Jack Ma | Alibaba Group | 35 | $48.4 | 🇨🇳 China |

| Eduard Kucera | Avast | 35 | $1.1 | 🇨🇿 Czech Republic |

| Bidzina Ivanishvili | Rossiysky Kredit | 35 | $4.8 | 🇬🇪 Georgia |

| Tahir | The Mayapada Group | 35 | $3.3 | 🇮🇩 Indonesia |

| John Armitage | Egerton Capital | 35 | $2.6 | 🇮🇪 Ireland |

| Tadashi Yanai | Uniqlo | 35 | $44.1 | 🇯🇵 Japan |

| Richard Hart | Raynolds Packaging Group | 35 | $8.7 | 🇳🇿 New Zealand |

Here are just a few highlights of late career breakthroughs:

Jack Ma

Ma is best known for co-founding Alibaba and becoming one of China’s wealthiest people, but his start came rather unexpectedly. After failing to secure jobs as a fresh graduate and starting his own translation company, Ma went on a business trip to the U.S. and discovered the internet (and a lack of Chinese websites). Over time, he connected Chinese companies with American coders to create websites, and soon saw room in the market for a business-to-business marketplace, which became Alibaba. The company secured millions in investment and would go on to become one of China’s leading forces in tech, all without Ma writing a single line of code.

Amancio Ortega

As the former CEO of fashion chain Zara and its parent company Inditex, Ortega is Europe’s third wealthiest person. That success came after opening the first Zara store in 1975 with his then-wife Rosalía Mera, with their store focusing on cheaper versions of high-end fashion. Ortega fine-tuned the design and manufacturing process to produce new trends more quickly, helping to pioneer the concept of “fast fashion,” and soon becoming a fashion powerhouse.

Jim Simons

Simons was once lauded as the world’s greatest investor, largely due to his outlandish returns of over 60% before fees. But he actually started in the academic field, acquiring a PhD in mathematics—he worked in many faculties, and even as a codebreaker for the NSA. Eventually, Simons utilized his mathematical knowledge on Wall Street, where he had his breakthrough in 1982 by starting his model-based hedge fund—Renaissance Technologies, and built a net worth of $24.6 billion.

Dietrich Mateschitz

One of the 60 richest people in the world, Austrian businessman Mateschitz got his start in marketing for Unilever and then cosmetics company Blendax. His breakthrough came on a business trip to Thailand, where the 40-year-old discovered that the local energy drink Krating Daeng helped his jet lag. Mateschitz and the drink’s creator, Chaleo Yoovidhya, each put up $500,000 to turn the drink into an exported energy brand, and Red Bull was born.

James Dyson

Before Dyson was a household name of vacuums, fans, and dryers, The UK’s James Dyson was an industrial engineer with many ideas for inventions. After getting frustrated with the bags of Hoover vacuum cleaners, Dyson had the idea for a bagless cyclone vacuum, and developed one after more than 5,000 prototypes over five years (and supported by his wife’s salary). At first he couldn’t find a manufacturer or success in the UK, so Dyson instead sold his vacuums in Japan and ended up winning the 1991 International Design Fair Prize there. Thirty years later, Dyson’s success led to a royal knighting and becoming the fourth richest person in the UK.

Late Bloomers: The Rule Not The Exception

It’s helpful to remember that these stories might be incredible and successful on a grand scale, but they are not entirely unique.

According to the U.S. Census Bureau, the majority of successful businesses have been founded by middle-aged people and the average age of a company’s founder at the time of founding is 41.9 years. Experience definitely pays dividends, and the saying that “life is a marathon, not a sprint” seems especially true for this list of late breakthrough billionaires.

Money

Charted: Which City Has the Most Billionaires in 2024?

Just two countries account for half of the top 20 cities with the most billionaires. And the majority of the other half are found in Asia.

Charted: Which Country Has the Most Billionaires in 2024?

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Some cities seem to attract the rich. Take New York City for example, which has 340,000 high-net-worth residents with investable assets of more than $1 million.

But there’s a vast difference between being a millionaire and a billionaire. So where do the richest of them all live?

Using data from the Hurun Global Rich List 2024, we rank the top 20 cities with the highest number of billionaires in 2024.

A caveat to these rich lists: sources often vary on figures and exact rankings. For example, in last year’s reports, Forbes had New York as the city with the most billionaires, while the Hurun Global Rich List placed Beijing at the top spot.

Ranked: Top 20 Cities with the Most Billionaires in 2024

The Chinese economy’s doldrums over the course of the past year have affected its ultra-wealthy residents in key cities.

Beijing, the city with the most billionaires in 2023, has not only ceded its spot to New York, but has dropped to #4, overtaken by London and Mumbai.

| Rank | City | Billionaires | Rank Change YoY |

|---|---|---|---|

| 1 | 🇺🇸 New York | 119 | +1 |

| 2 | 🇬🇧 London | 97 | +3 |

| 3 | 🇮🇳 Mumbai | 92 | +4 |

| 4 | 🇨🇳 Beijing | 91 | -3 |

| 5 | 🇨🇳 Shanghai | 87 | -2 |

| 6 | 🇨🇳 Shenzhen | 84 | -2 |

| 7 | 🇭🇰 Hong Kong | 65 | -1 |

| 8 | 🇷🇺 Moscow | 59 | No Change |

| 9 | 🇮🇳 New Delhi | 57 | +6 |

| 10 | 🇺🇸 San Francisco | 52 | No Change |

| 11 | 🇹🇭 Bangkok | 49 | +2 |

| 12 | 🇹🇼 Taipei | 45 | +2 |

| 13 | 🇫🇷 Paris | 44 | -2 |

| 14 | 🇨🇳 Hangzhou | 43 | -5 |

| 15 | 🇸🇬 Singapore | 42 | New to Top 20 |

| 16 | 🇨🇳 Guangzhou | 39 | -4 |

| 17T | 🇮🇩 Jakarta | 37 | +1 |

| 17T | 🇧🇷 Sao Paulo | 37 | No Change |

| 19T | 🇺🇸 Los Angeles | 31 | No Change |

| 19T | 🇰🇷 Seoul | 31 | -3 |

In fact all Chinese cities on the top 20 list have lost billionaires between 2023–24. Consequently, they’ve all lost ranking spots as well, with Hangzhou seeing the biggest slide (-5) in the top 20.

Where China lost, all other Asian cities—except Seoul—in the top 20 have gained ranks. Indian cities lead the way, with New Delhi (+6) and Mumbai (+3) having climbed the most.

At a country level, China and the U.S combine to make up half of the cities in the top 20. They are also home to about half of the world’s 3,200 billionaire population.

In other news of note: Hurun officially counts Taylor Swift as a billionaire, estimating her net worth at $1.2 billion.

-

Education1 week ago

Education1 week agoHow Hard Is It to Get Into an Ivy League School?

-

Technology2 weeks ago

Technology2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Demographics2 weeks ago

Demographics2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries

-

Economy2 weeks ago

Economy2 weeks agoWhere U.S. Inflation Hit the Hardest in March 2024

-

Environment2 weeks ago

Environment2 weeks agoTop Countries By Forest Growth Since 2001