7 ESG Essentials Investors Need to Know

The following content is sponsored by J.P. Morgan Asset Management.

7 ESG Essentials Investors Need to Know

From consumers to policy makers, many economic actors are backing sustainability—and creating a powerful portfolio opportunity for investors.

The use of environmental, social, and governance factors (altogether known as ESG) is increasingly informing investment decisions. But although ESG investing has grown in prominence in a few short years, there’s a disconnect:

- 69% of retail investors are interested in ESG, yet…

- Only 10% actually invest in products that incorporate ESG factors

To properly capitalize on this trend, it’s important to first fully understand it.

According to J.P. Morgan Asset Management, here are seven essentials that can help investors understand the growing importance of ESG investing.

1. ESG considerations are affecting consumer preferences and attitudes.

The public is paying attention to how companies position themselves, to ensure their purchases will be sustainable.

In a survey, respondents around the world were asked whether they agree with the question, “I buy from companies that are conscious of protecting the environment.”

Here are the trends that emerged:

| Country | Agree | Disagree |

|---|---|---|

| 🇨🇳 China | 71% | 3% |

| 🇮🇩 Indonesia | 61% | 3% |

| 🇸🇬 Singapore | 52% | 9% |

| 🇺🇸 U.S. | 51% | 15% |

| 🇰🇷 Korea | 48% | 17% |

| 🇩🇪 Germany | 47% | 11% |

| 🇦🇺 Australia | 47% | 15% |

| 🇯🇵 Japan | 33% | 22% |

| 🇭🇰 Hong Kong | 31% | 17% |

Source: J.P. Morgan Asset Management; PwC June 2021 Global consumer insights pulse survey. Data as of June 30, 2021.

Across markets, consumers in China seem to be the most environmentally inclined, but all countries surveyed exhibited a positive shift towards companies that support environmental protection.

Why it matters: Consumers are making decisions based on ESG considerations, and they’re voting with their wallets. This change has ripple effects, and is shifting from individuals to impacting higher levels, such as governments.

2. Policymakers are setting environmental and social goals.

Governments of the world’s top greenhouse gas (GHG) emitters are working towards a net zero future, in which GHG emissions are reduced or offset.

What is the current trajectory of GHG emissions (measured in tonnes per year of CO₂ equivalents, tCO₂e) and what is the gap we need to bridge in the race to net zero?

| Year | 🇪🇺 EU (tCO₂e) | 🇺🇸 U.S. (tCO₂e) | 🇨🇳 China (tCO₂e) |

|---|---|---|---|

| 1990 | 5.7B | 6.4B | 3.3B |

| 2000 | 5.2B | 7.3B | 5.1B |

| 2010 | 4.8B | 7.0B | 10.9B |

| 2020 | 3.7B | 5.9B | 13.0B |

| 2030P | 3.3B | 5.9B | 13.8B |

| 2040P | 1.6B | 3.0B | 9.2B |

| 2050P | 0B | 0B | 4.6B |

| 2060P | 0B | 0B | 0B |

Source: J.P. Morgan Asset Management; Climate Action Tracker. Data as of June 30, 2021.

Why it matters: Altogether, around 60 countries—representing over half of global GHG emissions—have set ambitious net zero emissions targets for the coming decades.

3. For some, the shift to sustainability may be a headwind.

Traditional energy needs to account for a much smaller proportion of the global energy mix, if we are to achieve the goal of net zero emissions by 2050.

Here’s what each energy source needs to contribute in terms of their share (%) of the primary energy mix, compared to past trends:

| Year | Oil | Coal | Gas | Renewables | Nuclear and Hydro |

|---|---|---|---|---|---|

| 1970 | 46.9% | 30.0% | 16.9% | 0.2% | 6.1% |

| 1980 | 45.8% | 26.9% | 18.3% | 0.2% | 8.7% |

| 1990 | 39.7% | 27.2% | 20.5% | 0.5% | 12.2% |

| 2000 | 39.2% | 25.0% | 21.9% | 0.7% | 13.3% |

| 2010 | 34.2% | 29.9% | 22.5% | 1.9% | 11.5% |

| 2030P | 26.9% | 17.0% | 22.2% | 20.9% | 12.9% |

| 2040P | 15.4% | 5.5% | 15.9% | 47.5% | 15.7% |

| 2050P | 6.8% | 1.9% | 13.0% | 59.2% | 19.0% |

Source: J.P. Morgan Asset Management; BP Energy Outlook 2020. Forecast is based on BP’s scenario for global net zero emissions by 2050. Data as of June 30, 2021.

Why it matters: The shift to renewable energy may pose a challenge for industries reliant on fossil fuels. Fortunately, it’s not too late for companies to transition.

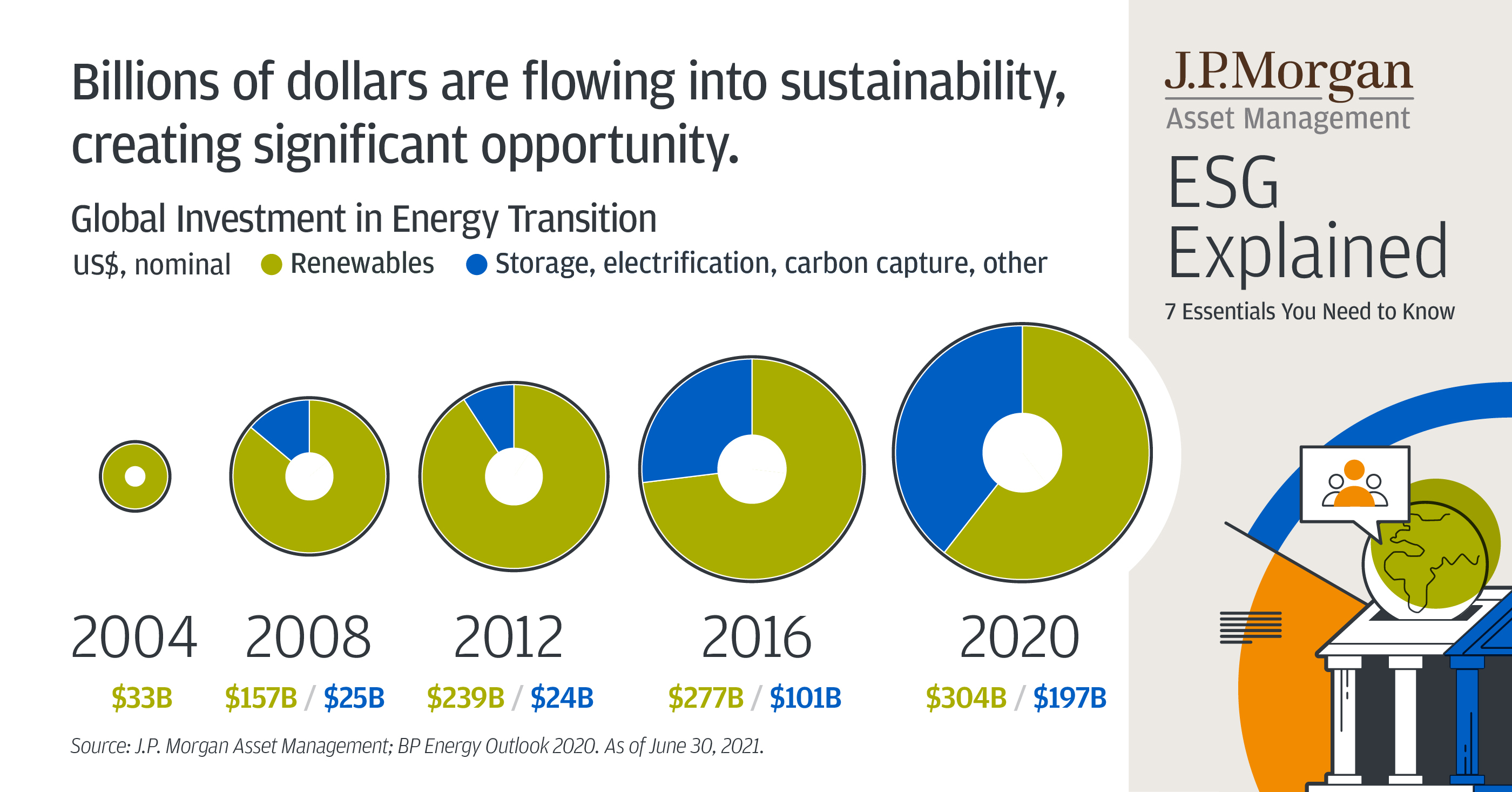

4. ESG creates opportunities for those at the forefront of change.

Looking at the movement of global investment, billions of dollars are flowing into the energy transition.

| Year | Renewable energy | Storage, electrification, carbon capture, other | Total Amount |

|---|---|---|---|

| 2004 | $33B | $0B | $33B |

| 2008 | $157B | $25B | $182B |

| 2012 | $239B | $24B | $263B |

| 2016 | $277B | $101B | $378B |

| 2020 | $304B | $197B | $501B |

Source: J.P. Morgan Asset Management; Bloomberg NEF, BP Statistical, Eurostat, Lazard, METI. Storage, electrification, other includes hydrogen, carbon capture and storage, energy storage, electrified transport and electrified heat. Data as of June 30, 2021.

Why it matters: With interest expanding quickly, this provides a unique opportunity to tap into the nascent ESG market.

5. ESG covers more than climate—Social and Governance is growing too.

As the name suggests, ESG is all-encompassing, with a scope that goes far beyond the environment.

MSCI analyzed the corporate mentions of diversity and inclusion in earnings calls (four-quarter moving average for MSCI ACWI companies)—and found that they have almost doubled in the past two years.

Why it matters: This signals rising interest in the varied criteria that make up ESG investing.

6. ESG is affecting the investment landscape.

The demand for sustainable fixed income strategies is also growing rapidly, with global sustainable bond issuance growing over 25x between 2016-2020:

| Type of Bond Issuance | 2012 | 2016 | 2020 |

|---|---|---|---|

| Green | $4B | $84B | $291B |

| Sustainable | $1B | $7B | $176B |

| Social | $1B | $3B | $237B |

Source: J.P. Morgan Asset Management; Climate Bonds Initiative. Data as of 30 June 2021.

Why it matters: Growth and demand is high, and sustainable investing is not limited to equities—environmental and social projects have increasing access to financing.

7. ESG is changing the nature of investment flows.

Looking at the big picture, here’s what proportion of each country’s assets into sustainable strategies has evolved around the world:

| Region/ Country | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|

| 🇪🇺 EU | 5% | 8% | 18% | 27% | 48% |

| 🇺🇸 U.S. | 1% | 0% | 1% | 4% | 22% |

| 🌏 APAC | -1% | -1% | 0% | 2% | 6% |

J.P. Morgan Asset Management, Morningstar. Data as of 30 June 2021.

Why it matters: Although certain regions are leading the way, overall demand for sustainable funds is expected to continue on this upward trend.

As these seven ESG essentials make clear, sustainable investing is becoming a compelling vehicle for change worldwide. But incorporating ESG criteria into investing is as much about doing well financially, as it is about doing good.

Find out more at J.P. Morgan Asset Management’s dedicated sustainable investing hub.

IMPORTANT DISCLAIMER

For the purposes of MiFID II, the JPM Market Insights and Portfolio Insights programs are marketing communications and are not in scope for any MiFID II / MiFIR requirements specifically related to investment research. Furthermore, the J.P. Morgan Asset Management Market Insights and Portfolio Insights programs, as non-independent research, have not been prepared in accordance with legal requirements designed to promote the independence of investment research, nor are they subject to any prohibition on dealing ahead of the dissemination of investment research. This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from J.P. Morgan Asset Management or any of its subsidiaries to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields are not reliable indicators of current and future results. J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our privacy policies at https://am.jpmorgan.com/global/privacy. This communication is issued by the following entities: In the United States, by J.P. Morgan Investment Management Inc. or J.P. Morgan Alternative Asset Management, Inc., both regulated by the Securities and Exchange Commission; in Latin America, for intended recipients’ use only, by local J.P. Morgan entities, as the case may be.; in Canada, for institutional clients’ use only, by JPMorgan Asset Management (Canada) Inc., which is a registered Portfolio Manager and Exempt Market Dealer in all Canadian provinces and territories except the Yukon and is also registered as an Investment Fund Manager in British Columbia, Ontario, Quebec and Newfoundland and Labrador. In the United Kingdom, by JPMorgan Asset Management (UK) Limited, which is authorized and regulated by the Financial Conduct Authority; in other European jurisdictions, by JPMorgan Asset Management (Europe) S.à r.l. In Asia Pacific (“APAC”), by the following issuing entities and in the respective jurisdictions in which they are primarily regulated: JPMorgan Asset Management (Asia Pacific) Limited, or JPMorgan Funds (Asia) Limited, or JPMorgan Asset Management Real Assets (Asia) Limited, each of which is regulated by the Securities and Futures Commission of Hong Kong; JPMorgan Asset Management (Singapore) Limited (Co. Reg. No. 197601586K), which this advertisement or publication has not been reviewed by the Monetary Authority of Singapore; JPMorgan Asset Management (Taiwan) Limited; JPMorgan Asset Management (Japan) Limited, which is a member of the Investment Trusts Association, Japan, the Japan Investment Advisers Association, Type II Financial Instruments Firms Association and the Japan Securities Dealers Association and is regulated by the Financial Services Agency (registration number “Kanto Local Finance Bureau (Financial Instruments Firm) No. 330”); in Australia, to wholesale clients only as defined in section 761A and 761G of the Corporations Act 2001 (Commonwealth), by JPMorgan Asset Management (Australia) Limited (ABN 55143832080) (AFSL 376919). For all other markets in APAC, to intended recipients only.

Our manager seeks to integrate environmental, social and governance (“ESG”) factors in the investment processes. ESG integration is the systematic integration of material ESG factors in company/issuer selection through research and risk management. It involves proprietary research on financial materiality of the ESG factors in relation to the relevant company/issuer and discretion to invest regardless of whether the company/issuer may be positively or negatively impacted by the ESG factors. Integration of ESG factors in investment processes does not imply the funds or strategies incorporate ESG factors as a key investment focus.

For U.S. only: If you are a person with a disability and need additional support in viewing the material, please call us at 1-800-343-1113 for assistance. Copyright 2021 JPMorgan Chase & Co. All rights reserved.

-

Sponsored3 years ago

Sponsored3 years agoMore Than Precious: Silver’s Role in the New Energy Era (Part 3 of 3)

Long known as a precious metal, silver in solar and EV technologies will redefine its role and importance to a greener economy.

-

Sponsored7 years ago

Sponsored7 years agoThe History and Evolution of the Video Games Market

Everything from Pong to the rise of mobile gaming and AR/VR. Learn about the $100 billion video games market in this giant infographic.

-

Sponsored8 years ago

Sponsored8 years agoThe Extraordinary Raw Materials in an iPhone 6s

Over 700 million iPhones have now been sold, but the iPhone would not exist if it were not for the raw materials that make the technology...

-

Sponsored8 years ago

Sponsored8 years agoThe Industrial Internet, and How It’s Revolutionizing Mining

The convergence of the global industrial sector with big data and the internet of things, or the Industrial Internet, will revolutionize how mining works.