Money

The World’s Most Famous Case of Hyperinflation (Pt. 2)

The World’s Most Famous Case of Hyperinflation (Part 2)

The Money Project is an ongoing collaboration between Visual Capitalist and Texas Precious Metals that seeks to use intuitive visualizations to explore the origins, nature, and use of money.

For the first infographic in this series, which summarizes the circumstances leading up to hyperinflation in Germany in 1921-1924, it can be found here: Hyperinflation (Part 1 of 2)

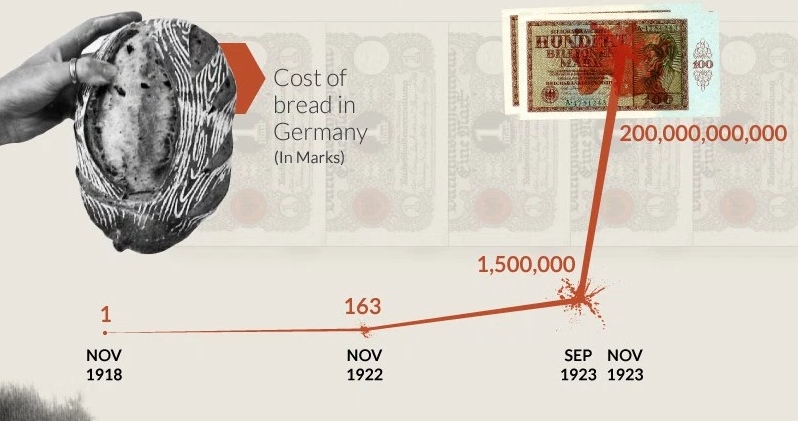

Slippery Slope

“Inflation took the basic law-and-order principles of loyalty and trust to the extreme.” Martin Geyer, Historian.

“As things stand, the only way to finance the cost of fighting the war is to shift the burden into the future through loans.” Karl Helfferich, an economist in 1915.

“There is a point at which printing money affects purchasing power by causing inflation.” Eduard Bernstein, socialist in 1918.

In the two years past World War I, the German government added to the monetary base of the Papiermark by printing money. Economic historian Carl-Ludwig Holtfrerich said that the “lubricant of inflation” helped breathe new life into the private sector.

The mark was trading for a low value against the dollar, sterling and the French franc and this helped to boost exports. Industrial output increased by 20% a year, unemployment fell to below 1 percent in 1922, and real wages rose significantly.

Then, suddenly this “lubricant” turned into a slippery slope: at its most severe, the monthly rate of inflation reached 3.25 billion percent, equivalent to prices doubling every 49 hours.

When did the “lubricant” of inflation turn into a toxic hyperinflationary spiral?

The ultimate trigger for German hyperinflation was the loss of trust in the government’s policy and debt. Foreign markets refused to buy German debt or Papiermarks, the exchange rate depreciated, and the rate of inflation accelerated.

The Effects

Hyperinflation in Germany left millions of hard-working savers with nothing left.

Over the course of months, what was enough money to start a stable retirement fund was no longer enough to buy even a loaf of bread.

Who was affected?

- The middle class – or Mittelstand – saw the value of their cash savings wiped out before their eyes.

- Wealth was transferred from general public to the government, which issued the money.

- Borrowers gained at the expense of lenders.

- Renters gained at the expense of property owners (In Germany’s case, rent ceilings did not keep pace with general price levels)

- The efficiency of the economy suffered, as people preferred to barter.

- People preferred to hold onto hard assets (commodities, gold, land) rather than paper money, which continually lost value.

Stories of Hyperinflation

During the peak of hyperinflation, workers were often paid twice a day. Workers would shop at midday to make sure their money didn’t lose more value. People burned paper bills in the stove, as they were cheaper than wood or other fuel.

Here some of the stories of ordinary Germans during the world’s most famous case of hyperinflation.

- “The price of tram rides and beef, theater tickets and school, newspapers and haircuts, sugar and bacon, is going up every week,” Eugeni Xammar, a journalist, wrote in February 1923. “As a result no one knows how long their money will last, and people are living in constant fear, thinking of nothing but eating and drinking, buying and selling.”

- A man who drank two cups of coffee at 5,000 marks each was presented with a bill for 14,000 marks. When he asked about the large bill, he was told he should have ordered the coffees at the same time because the price had gone up in between cups.

- A young couple took a few hundred million marks to the theater box office hoping to see a show, but discovered it wasn’t nearly enough. Tickets were now a billion marks each.

- Historian Golo Mann wrote: “The effect of the devaluation of the German currency was like that of a second revolution, the first being the war and its immediate aftermath,” he concluded. Mann said deep-seated faith was being destroyed and replaced by fear and cynicism. “What was there to trust, who could you rely on if such were even possible?” he asked.

Even Worse Cases of Hyperinflation

While the German hyperinflation from 1921-1924 is the most known – it was not the worst episode in history.

In mid-1946, prices in Hungary doubled every fifteen hours, giving an inflation rate of 41.9 quintillion percent. By July 1946, the 1931 gold pengõ was worth 130 trillion paper pengõs.

Peak Inflation Rates:

Germany (1923): 3.5 billion percent

Zimbabwe (2008): 79.6 billion percent

Hungary (1946): 41.9 quintillion percent

Hyperinflation has been surprisingly common in the 20th century, happening many dozens of times throughout the world. It continues to happen even today in countries such as Venezuela.

What would become of Germany after its bout of hyperinflation?

A young man named Adolf Hitler began to grow angry that innocent Germans were starving…

“We are opposed to swarms of Americans and other foreigners raising prices throughout Germany while millions of Germans are starving because of the increased prices. We are equally opposed to German profiteers and we are demanding that all be imprisoned.” – Adolf Hitler, 1923, Chicago Tribune

About the Money Project

The Money Project aims to use intuitive visualizations to explore ideas around the very concept of money itself. Founded in 2015 by Visual Capitalist and Texas Precious Metals, the Money Project will look at the evolving nature of money, and will try to answer the difficult questions that prevent us from truly understanding the role that money plays in finance, investments, and accumulating wealth.

Money

Charted: Which City Has the Most Billionaires in 2024?

Just two countries account for half of the top 20 cities with the most billionaires. And the majority of the other half are found in Asia.

Charted: Which Country Has the Most Billionaires in 2024?

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Some cities seem to attract the rich. Take New York City for example, which has 340,000 high-net-worth residents with investable assets of more than $1 million.

But there’s a vast difference between being a millionaire and a billionaire. So where do the richest of them all live?

Using data from the Hurun Global Rich List 2024, we rank the top 20 cities with the highest number of billionaires in 2024.

A caveat to these rich lists: sources often vary on figures and exact rankings. For example, in last year’s reports, Forbes had New York as the city with the most billionaires, while the Hurun Global Rich List placed Beijing at the top spot.

Ranked: Top 20 Cities with the Most Billionaires in 2024

The Chinese economy’s doldrums over the course of the past year have affected its ultra-wealthy residents in key cities.

Beijing, the city with the most billionaires in 2023, has not only ceded its spot to New York, but has dropped to #4, overtaken by London and Mumbai.

| Rank | City | Billionaires | Rank Change YoY |

|---|---|---|---|

| 1 | 🇺🇸 New York | 119 | +1 |

| 2 | 🇬🇧 London | 97 | +3 |

| 3 | 🇮🇳 Mumbai | 92 | +4 |

| 4 | 🇨🇳 Beijing | 91 | -3 |

| 5 | 🇨🇳 Shanghai | 87 | -2 |

| 6 | 🇨🇳 Shenzhen | 84 | -2 |

| 7 | 🇭🇰 Hong Kong | 65 | -1 |

| 8 | 🇷🇺 Moscow | 59 | No Change |

| 9 | 🇮🇳 New Delhi | 57 | +6 |

| 10 | 🇺🇸 San Francisco | 52 | No Change |

| 11 | 🇹🇭 Bangkok | 49 | +2 |

| 12 | 🇹🇼 Taipei | 45 | +2 |

| 13 | 🇫🇷 Paris | 44 | -2 |

| 14 | 🇨🇳 Hangzhou | 43 | -5 |

| 15 | 🇸🇬 Singapore | 42 | New to Top 20 |

| 16 | 🇨🇳 Guangzhou | 39 | -4 |

| 17T | 🇮🇩 Jakarta | 37 | +1 |

| 17T | 🇧🇷 Sao Paulo | 37 | No Change |

| 19T | 🇺🇸 Los Angeles | 31 | No Change |

| 19T | 🇰🇷 Seoul | 31 | -3 |

In fact all Chinese cities on the top 20 list have lost billionaires between 2023–24. Consequently, they’ve all lost ranking spots as well, with Hangzhou seeing the biggest slide (-5) in the top 20.

Where China lost, all other Asian cities—except Seoul—in the top 20 have gained ranks. Indian cities lead the way, with New Delhi (+6) and Mumbai (+3) having climbed the most.

At a country level, China and the U.S combine to make up half of the cities in the top 20. They are also home to about half of the world’s 3,200 billionaire population.

In other news of note: Hurun officially counts Taylor Swift as a billionaire, estimating her net worth at $1.2 billion.

-

Mining1 week ago

Mining1 week agoGold vs. S&P 500: Which Has Grown More Over Five Years?

-

Markets2 weeks ago

Markets2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Countries2 weeks ago

Countries2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries