Economy

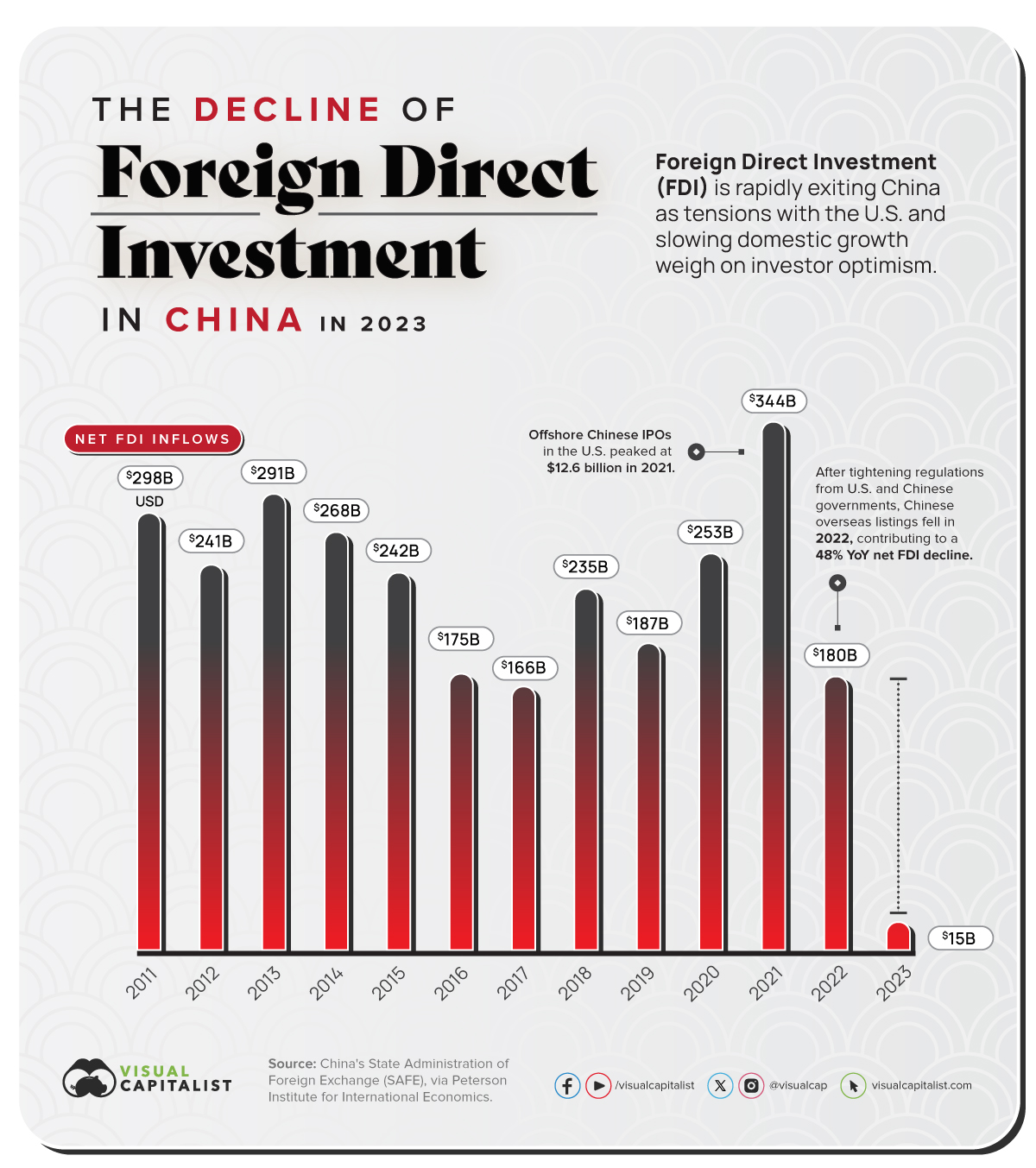

Charted: Chinese FDI Inflows Hit Multi-Year Lows

![]() See this visualization first on the Voronoi app.

See this visualization first on the Voronoi app.

Charted: Chinese FDI Inflows Hit Multi-Year Lows

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

The Chinese economy has thrown up several red flags in 2023 and now foreign investors are losing confidence in the world’s second-largest economy.

Data accessed via the Peterson Institute for International Economics and sourced from China’s State Administration of Foreign Exchange (SAFE) shows foreign direct investment (FDI) inflows have hit multi-year lows.

Foreign Investors Hit “Sell” on China in 2023

Aside from a broadly slowing economy, the Peterson Institute’s analysis highlights other key reasons why FDI inflows have scaled back so dramatically this year.

Firstly, geopolitical tensions (in the form of an escalating chip war) between the U.S. and China are worrying foreign investors—many of them American-headquartered companies with a presence in China, holding back on investments in local companies.

Secondly, the closure of due diligence firms (which allow foreign investors to make informed decisions on Chinese companies) along with a new national security law aimed at restricting cross-border data flows have disincentivized foreign investors from betting big if they wanted to.

| Year | FDI Inflows | YoY Change |

|---|---|---|

| 2011 | $280B | N/A |

| 2012 | $241B | -13.93% |

| 2013 | $291B | +20.75% |

| 2014 | $268B | -7.90% |

| 2015 | $242B | -9.70% |

| 2016 | $175B | -27.69% |

| 2017 | $166B | -5.14% |

| 2018 | $235B | +41.57% |

| 2019 | $187B | -20.43% |

| 2020 | $253B | +35.29% |

| 2021 | $344B | +35.97% |

| 2022 | $180B | -47.67% |

| 2023 Q1-Q3 | $15B | -91.67% |

Meanwhile, huge spikes in FDI inflows between 2018 and 2021 indicate the success of Chinese companies listing on American securities exchanges, which SAFE includes in its data. However, crackdowns from both Chinese and U.S. securities regulators in 2022 turned the tap off briefly. Despite the restrictions being since removed, new listings have not bounced back.

Another Red Flag for the Chinese Economy

The Peterson Institute’s comparison of gross and net FDI flows found a nearly $100 billion shortfall—which means foreign firms are selling their Chinese investments, adding yet another red flag for the economy.

This slowdown is now having a ripple effect across the region—for Japan, South Korea, and Thailand’s economies—whose export sectors rely on substantial Chinese demand. Nations in sub-saharan Africa will also feel the pinch as Chinese sovereign lending continues to fall, already past the lowest it’s been in two decades.

Meanwhile, on a broader scale, Chinese growth contributes to one-third of world economic growth, which means the global economy will miss growth projections made last year—when economists had a more optimistic view of the world’s second-largest economy.

Economy

Economic Growth Forecasts for G7 and BRICS Countries in 2024

The IMF has released its economic growth forecasts for 2024. How do the G7 and BRICS countries compare?

G7 & BRICS Real GDP Growth Forecasts for 2024

The International Monetary Fund’s (IMF) has released its real gross domestic product (GDP) growth forecasts for 2024, and while global growth is projected to stay steady at 3.2%, various major nations are seeing declining forecasts.

This chart visualizes the 2024 real GDP growth forecasts using data from the IMF’s 2024 World Economic Outlook for G7 and BRICS member nations along with Saudi Arabia, which is still considering an invitation to join the bloc.

Get the Key Insights of the IMF’s World Economic Outlook

Want a visual breakdown of the insights from the IMF’s 2024 World Economic Outlook report?

This visual is part of a special dispatch of the key takeaways exclusively for VC+ members.

Get the full dispatch of charts by signing up to VC+.

Mixed Economic Growth Prospects for Major Nations in 2024

Economic growth projections by the IMF for major nations are mixed, with the majority of G7 and BRICS countries forecasted to have slower growth in 2024 compared to 2023.

Only three BRICS-invited or member countries, Saudi Arabia, the UAE, and South Africa, have higher projected real GDP growth rates in 2024 than last year.

| Group | Country | Real GDP Growth (2023) | Real GDP Growth (2024P) |

|---|---|---|---|

| G7 | 🇺🇸 U.S. | 2.5% | 2.7% |

| G7 | 🇨🇦 Canada | 1.1% | 1.2% |

| G7 | 🇯🇵 Japan | 1.9% | 0.9% |

| G7 | 🇫🇷 France | 0.9% | 0.7% |

| G7 | 🇮🇹 Italy | 0.9% | 0.7% |

| G7 | 🇬🇧 UK | 0.1% | 0.5% |

| G7 | 🇩🇪 Germany | -0.3% | 0.2% |

| BRICS | 🇮🇳 India | 7.8% | 6.8% |

| BRICS | 🇨🇳 China | 5.2% | 4.6% |

| BRICS | 🇦🇪 UAE | 3.4% | 3.5% |

| BRICS | 🇮🇷 Iran | 4.7% | 3.3% |

| BRICS | 🇷🇺 Russia | 3.6% | 3.2% |

| BRICS | 🇪🇬 Egypt | 3.8% | 3.0% |

| BRICS-invited | 🇸🇦 Saudi Arabia | -0.8% | 2.6% |

| BRICS | 🇧🇷 Brazil | 2.9% | 2.2% |

| BRICS | 🇿🇦 South Africa | 0.6% | 0.9% |

| BRICS | 🇪🇹 Ethiopia | 7.2% | 6.2% |

| 🌍 World | 3.2% | 3.2% |

China and India are forecasted to maintain relatively high growth rates in 2024 at 4.6% and 6.8% respectively, but compared to the previous year, China is growing 0.6 percentage points slower while India is an entire percentage point slower.

On the other hand, four G7 nations are set to grow faster than last year, which includes Germany making its comeback from its negative real GDP growth of -0.3% in 2023.

Faster Growth for BRICS than G7 Nations

Despite mostly lower growth forecasts in 2024 compared to 2023, BRICS nations still have a significantly higher average growth forecast at 3.6% compared to the G7 average of 1%.

While the G7 countries’ combined GDP is around $15 trillion greater than the BRICS nations, with continued higher growth rates and the potential to add more members, BRICS looks likely to overtake the G7 in economic size within two decades.

BRICS Expansion Stutters Before October 2024 Summit

BRICS’ recent expansion has stuttered slightly, as Argentina’s newly-elected president Javier Milei declined its invitation and Saudi Arabia clarified that the country is still considering its invitation and has not joined BRICS yet.

Even with these initial growing pains, South Africa’s Foreign Minister Naledi Pandor told reporters in February that 34 different countries have submitted applications to join the growing BRICS bloc.

Any changes to the group are likely to be announced leading up to or at the 2024 BRICS summit which takes place October 22-24 in Kazan, Russia.

Get the Full Analysis of the IMF’s Outlook on VC+

This visual is part of an exclusive special dispatch for VC+ members which breaks down the key takeaways from the IMF’s 2024 World Economic Outlook.

For the full set of charts and analysis, sign up for VC+.

-

Debt1 week ago

Debt1 week agoHow Debt-to-GDP Ratios Have Changed Since 2000

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Countries2 weeks ago

Countries2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries

-

United States2 weeks ago

United States2 weeks agoWhere U.S. Inflation Hit the Hardest in March 2024

-

Green2 weeks ago

Green2 weeks agoTop Countries By Forest Growth Since 2001

-

United States2 weeks ago

United States2 weeks agoRanked: The Largest U.S. Corporations by Number of Employees