Technology

Can Predictive Data Revolutionize Capital Markets?

Can Predictive Data Revolutionize Capital Markets?

For investors around the world, the information age presents a double-edged sword.

On one hand, all this data can be harnessed to make intelligent and timely investment decisions. However, with data growing at exponential rates, this also means that there is a lot of noise – and finding the right signal can be like looking for a needle in a haystack.

Today’s infographic from Mergalim shows how the power of predictive data analytics is growing, and using tools like AI and Bayesian inference to anticipate the outcome of events before they happen is more feasible and applicable than ever.

The Big Data Landscape

Before we get into predictive analytics, let’s look at what investors are up against in the first place.

Volume: The rate of data creation is accelerating so fast, that in 2017 there will be more data created than the previous 5,000 years combined. To put this in perspective: in the U.S. alone, approximately 2,657,000 GB of data is created every minute.

Variety: Data is not uniform, and there are many types of data. With data coming from many sources simultaneously, useful analysis can be very difficult.

Velocity: Especially in the markets, data needs to be monitored in real-time to be useful. Getting information too late could mean zero liquidity for a portfolio in some sort of crisis.

In other words, one missed data signal can cause irreparable harm to a portfolio in a situation where things go awry. Therefore, along with having a smart allocation of assets, it can be advantageous to also be one step ahead of the game to know what’s coming.

The Power of Predictive Data

Predictive analytics is defined as:

“The branch of advanced analytics used to make predictions about unknown future events. It uses techniques from data mining, statistics, modelling, machine learning, and artificial intelligence to make predictions about the future.”

This kind of predictive power is already widely used by companies like Amazon, which uses algorithms to sort through billions of data points, your buying history, and current trends to recommend to you the items that you are most likely to buy. In fact, experts estimate that 35% of Amazon’s revenue comes from this practice of anticipating exactly what you want.

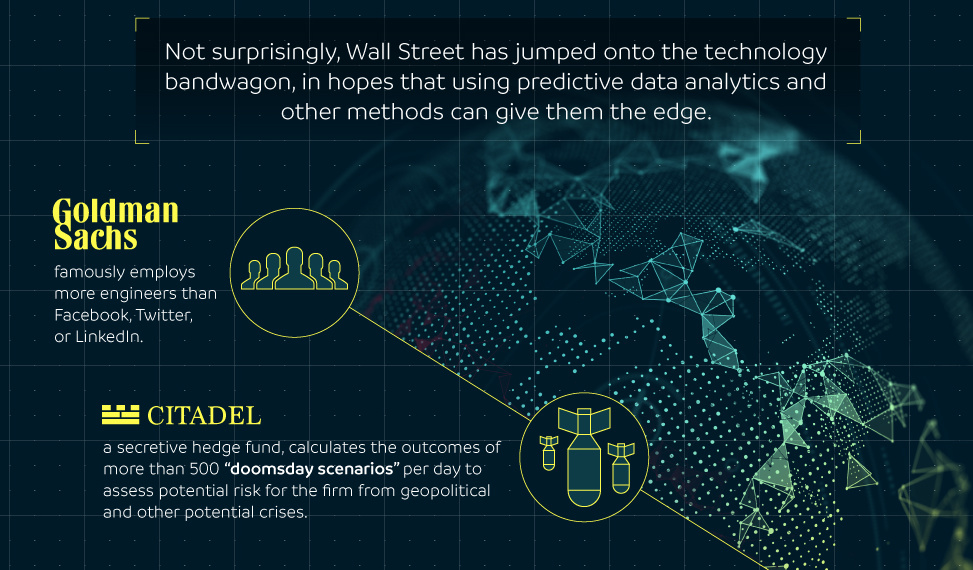

Not surprisingly, Wall Street has jumped on this bandwagon too.

- Goldman Sachs famously employs more engineers than Facebook, Twitter, or LinkedIn.

- Citadel, a secretive hedge fund, calculates the outcomes of more than 500 “doomsday scenarios” per day to assess potential risk for the firm from geopolitical and other potential crises

- Quantitative traders use streams of data and complex algorithms to create models of the market to find predictable patterns, and create machine-derived forecasts

But there is one possible limitation with these approaches. Markets are complex systems and need to be analyzed as such. After all, human decision makers can be irrational, events can be “triggered” by seemingly random factors, and traditional mathematical models can fall apart when markets get volatile.

A Multi-Disciplinary Approach?

One solution to this limitation may be to borrow ideas from the intelligence industry, which must anticipate irrational or “random” human actions before they happen.

As an example of this, intelligence agencies like the CIA have already been working to apply other disciplines to the techniques already widely used in predictive data:

Bayesian Inference: A formula in which the probability for the hypothesis is updated based on new data.

Behavioral Psychology: The science behind how responses to environmental stimuli shape people’s actions.

Complexity Theory: Born in the 1960s, the science around how complex systems work is now well established.

Fuzzy Cognitive Maps: A way of representing social scientific knowledge and modelling decision making in systems.

Historical Perspective: Applying knowledge of past events and subject matter experts to these other disciplinary fields.

Artificial Intelligence: Today’s deep learning now allows AI to instantly recognize and process all types of previously impenetrable data.

If predictive data analytics becomes the norm and its potential is fully realized, having data only in real-time may not be enough for many active market participants. In turn, this could set up a very different landscape than exists today.

Technology

Visualizing AI Patents by Country

See which countries have been granted the most AI patents each year, from 2012 to 2022.

Visualizing AI Patents by Country

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

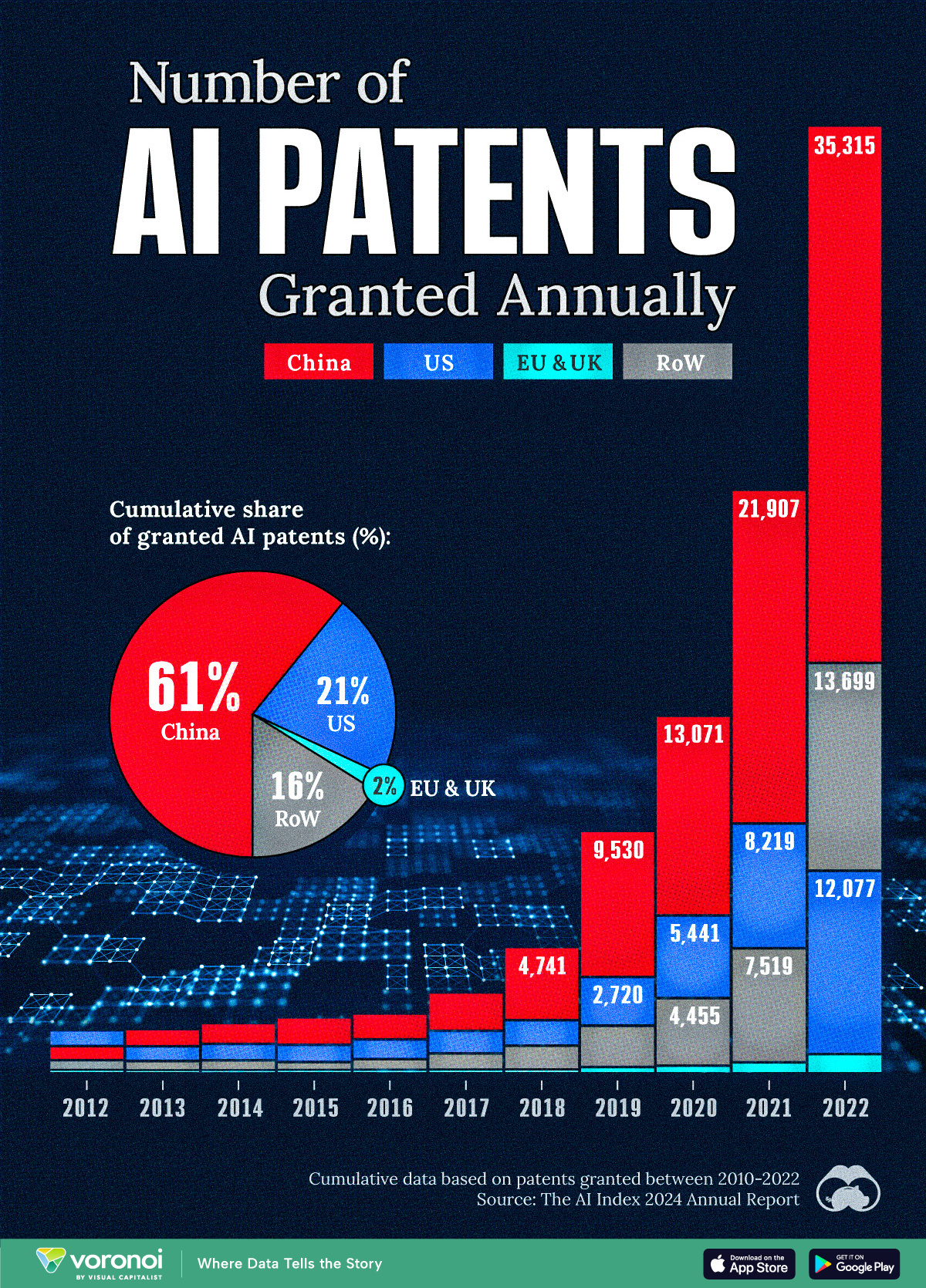

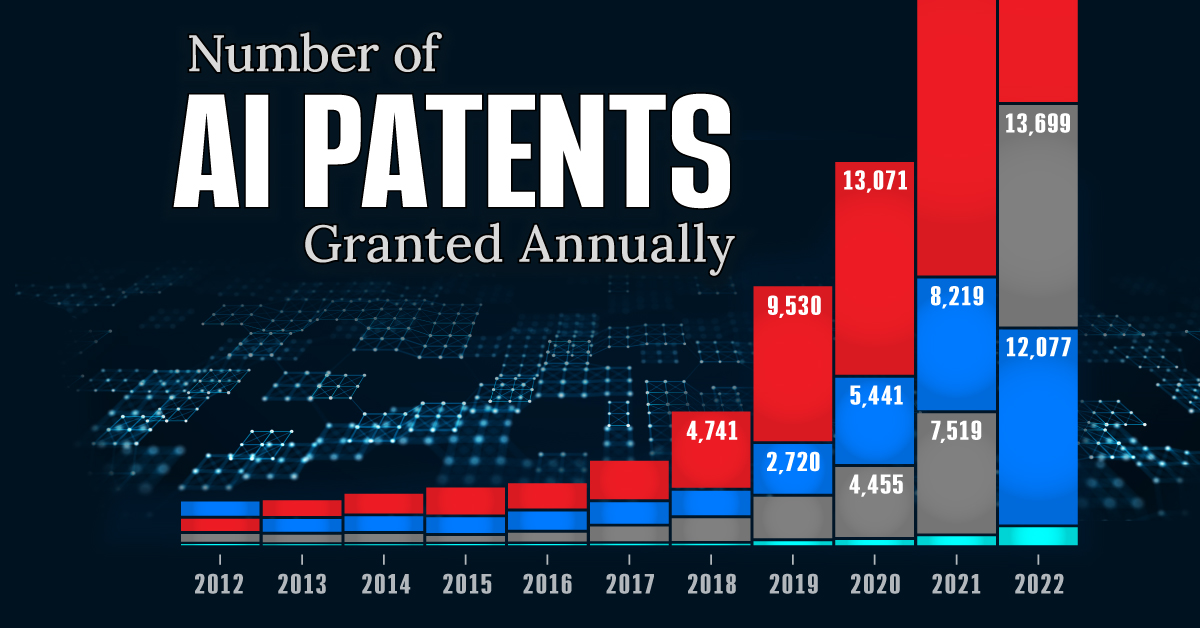

This infographic shows the number of AI-related patents granted each year from 2010 to 2022 (latest data available). These figures come from the Center for Security and Emerging Technology (CSET), accessed via Stanford University’s 2024 AI Index Report.

From this data, we can see that China first overtook the U.S. in 2013. Since then, the country has seen enormous growth in the number of AI patents granted each year.

| Year | China | EU and UK | U.S. | RoW | Global Total |

|---|---|---|---|---|---|

| 2010 | 307 | 137 | 984 | 571 | 1,999 |

| 2011 | 516 | 129 | 980 | 581 | 2,206 |

| 2012 | 926 | 112 | 950 | 660 | 2,648 |

| 2013 | 1,035 | 91 | 970 | 627 | 2,723 |

| 2014 | 1,278 | 97 | 1,078 | 667 | 3,120 |

| 2015 | 1,721 | 110 | 1,135 | 539 | 3,505 |

| 2016 | 1,621 | 128 | 1,298 | 714 | 3,761 |

| 2017 | 2,428 | 144 | 1,489 | 1,075 | 5,136 |

| 2018 | 4,741 | 155 | 1,674 | 1,574 | 8,144 |

| 2019 | 9,530 | 322 | 3,211 | 2,720 | 15,783 |

| 2020 | 13,071 | 406 | 5,441 | 4,455 | 23,373 |

| 2021 | 21,907 | 623 | 8,219 | 7,519 | 38,268 |

| 2022 | 35,315 | 1,173 | 12,077 | 13,699 | 62,264 |

In 2022, China was granted more patents than every other country combined.

While this suggests that the country is very active in researching the field of artificial intelligence, it doesn’t necessarily mean that China is the farthest in terms of capability.

Key Facts About AI Patents

According to CSET, AI patents relate to mathematical relationships and algorithms, which are considered abstract ideas under patent law. They can also have different meaning, depending on where they are filed.

In the U.S., AI patenting is concentrated amongst large companies including IBM, Microsoft, and Google. On the other hand, AI patenting in China is more distributed across government organizations, universities, and tech firms (e.g. Tencent).

In terms of focus area, China’s patents are typically related to computer vision, a field of AI that enables computers and systems to interpret visual data and inputs. Meanwhile America’s efforts are more evenly distributed across research fields.

Learn More About AI From Visual Capitalist

If you want to see more data visualizations on artificial intelligence, check out this graphic that shows which job departments will be impacted by AI the most.

-

Mining1 week ago

Mining1 week agoGold vs. S&P 500: Which Has Grown More Over Five Years?

-

Markets2 weeks ago

Markets2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Countries2 weeks ago

Countries2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries