The 26-Year History of ETFs, in One Infographic

The following content is sponsored by iShares by BlackRock.

The 26-Year History of ETFs, in One Infographic

In recent decades, there have been many breakthrough technologies that have re-shaped the nature of entire industries.

In finance, perhaps the most notable disruption has come from the rise of the exchange-traded fund (ETF) — an investment vehicle that has quadrupled in size over the last decade alone. But how did the ETF originate, and how has its use evolved through to today?

Today’s infographic comes to us from iShares by BlackRock, and it shows how the ETF has gone from an obscure index tracking tool to becoming a mainstream investing vehicle that encompasses trillions of dollars of assets around the world.

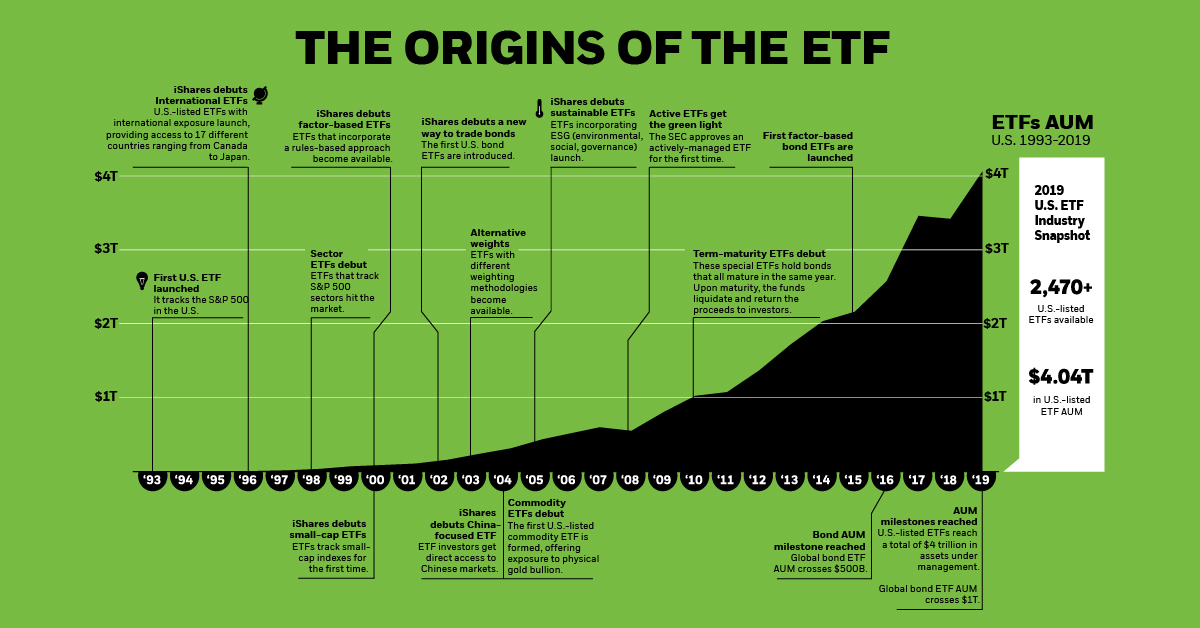

The Origin and History of ETFs

ETFs emerged out of the index investing phenomenon in the late 1980s and early 1990s, and there are two early examples that can be referenced as a starting point:

- Index Participation Shares – 1989

This initial attempt to create an ETF was set to track the S&P 500, and garnered significant investor interest. However, it was ruled to work like a futures contract according to a federal court in Chicago, so it never made it to the exchange. - Toronto 35 Index Participation Units – 1990

These were a warehouse, receipt-based instrument that tracked Canada’s major index, the TSE-35. They allowed investors to participate in the performance in the index, without owning individual shares of stocks in the index.

Since these pioneering ETF endeavors, the investment vehicle has caught on in popularity — and it is now clear that ETFs provide a range of important benefits to investors, such as: low costs, liquidity, diversification, tax efficiency, flexibility, accessibility, and transparency.

Key Milestones in U.S. ETF History:

- 1993 – The First ETF launches in the U.S., tracking the S&P 500

- 1998 – Sector ETFs debut, tracking individual S&P 500 sectors

- 2004 – The first U.S.-listed commodity ETF is formed, offering exposure to gold bullion

- 2008 – Actively-managed ETFs get the green light from the SEC

- 2010 – Term-maturity ETFs debut, holding bonds that all mature in same year

- 2015 – First factor-based bond ETFs are launched

- 2019 – U.S.-listed ETFs hit $4 trillion in AUM, and global bond ETF AUM crosses $1 trillion

How ETFs are Used Today

Today, the U.S. ETF industry has $4.04 trillion of assets under management (AUM), covering a wide spectrum of assets including equities, bonds, alternatives, and money markets.

ETFs are now the go-to index vehicle for 78% of institutional investors, according to a study by Greenwich Associates. Here are the 10 most popular applications for ETFs based on the same data:

| ETF Application | Usage | Description |

|---|---|---|

| Tactical adjustments | 72% | Over- or underweight certain styles, regions, or countries on the basis of short term views. |

| Core allocation | 68% | Build a long-term strategic holding in a portfolio. |

| Rebalancing | 60% | Manage portfolio risk in between rebalancing cycles. |

| Portfolio completion | 57% | Fill in gaps in a strategic asset allocation. |

| International diversification | 56% | Gain efficient access to foreign markets. |

| Liquidity management | 54% | Maintain exposure in a liquid investment vehicle to meet cash flow needs. |

| Transition management | 44% | Facilitate manager transitions with ETFs. |

| Risk management | 42% | Mitigate undesired portfolio risk and hedge asset allocation decisions. |

| Interim beta | 37% | Maintain market exposure while refining a long-term view. |

| Cash equitization | 37% | Put long-term cash positions to work with ETFs to minimize cash drag. |

In the 26 years since the introduction of ETFs, they have grown and evolved to cover almost every aspect of the market. The next stage of growth for the ETF will be driven by investors finding even more uses for these versatile tools.

-

Sponsored3 years ago

Sponsored3 years agoMore Than Precious: Silver’s Role in the New Energy Era (Part 3 of 3)

Long known as a precious metal, silver in solar and EV technologies will redefine its role and importance to a greener economy.

-

Sponsored7 years ago

Sponsored7 years agoThe History and Evolution of the Video Games Market

Everything from Pong to the rise of mobile gaming and AR/VR. Learn about the $100 billion video games market in this giant infographic.

-

Sponsored8 years ago

Sponsored8 years agoThe Extraordinary Raw Materials in an iPhone 6s

Over 700 million iPhones have now been sold, but the iPhone would not exist if it were not for the raw materials that make the technology...

-

Sponsored8 years ago

Sponsored8 years agoThe Industrial Internet, and How It’s Revolutionizing Mining

The convergence of the global industrial sector with big data and the internet of things, or the Industrial Internet, will revolutionize how mining works.