Erupting Gold Exploration Potential: The Pacific Ring of Fire

The following content is sponsored by Kalo Gold.

The Pacific Ring of Fire

From bubbling pits of lava to deep ocean sinkholes and everything in between, the Earth is full of geological wonders. The Pacific Ring of Fire is a prime example of one such marvel. Like a necklace of pearls, this long belt of active and inactive volcanoes spans 40,000 km along the tectonic plate boundaries of the Pacific Ocean.

While many people see volcanoes as something to fear, for the mining industry, they can present huge potential. In fact, ancient inactive volcanoes could eventually become profitable mines. With 75% of the earth’s volcanoes and 90% of all earthquakes, the Pacific Ring of Fire is home to many rich mineral deposits, such as gold, copper, molybdenum, and other metals.

Today’s infographic comes to us from Kalo Gold and highlights how the Pacific Ring of Fire’s geology enables the potential for mineral discovery.

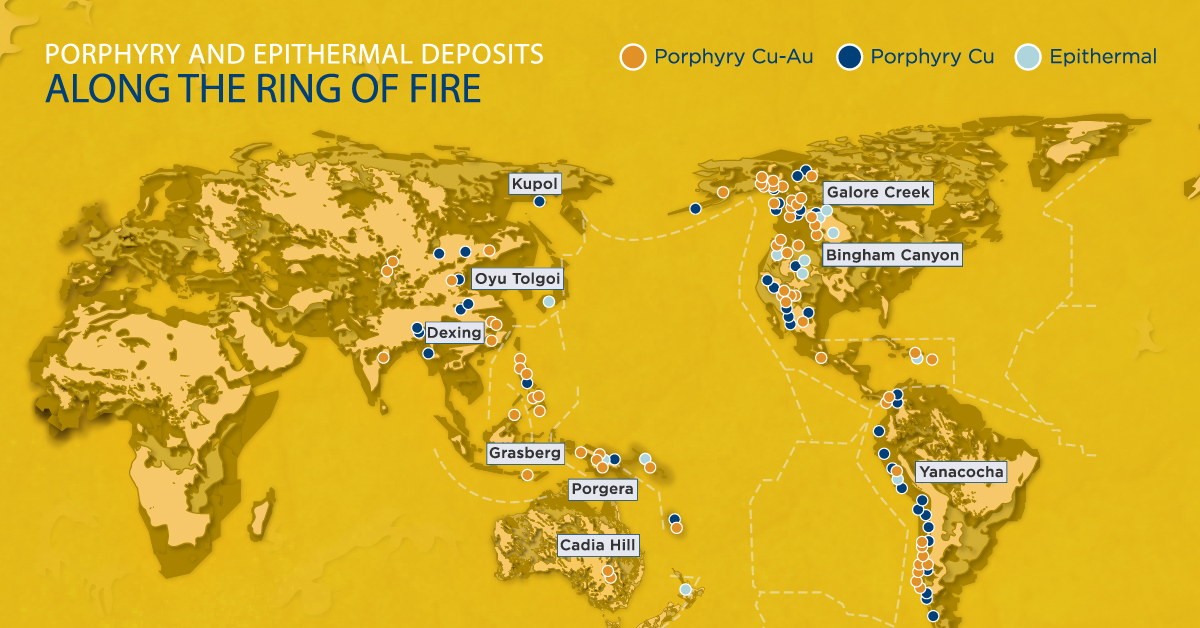

Magmas to Metals: Mineral Deposits on the Pacific Ring of Fire

Volcanic activity at tectonic plate boundaries reveals the natural processes of creation and destruction that shape the Earth along its Pacific Rim. The Pacific Ring of Fire is built on two types of tectonic plate boundaries:

- Convergent:

Two tectonic plates moving towards each other, where the oceanic crust often subducts under the continental crust. - Divergent:

Two tectonic plates moving away from each other, often resulting in rifts and earthquakes.

It is at these subduction zones where volcanic and seismic activity aids the formation of mineral deposits. The subduction of one plate under the other creates immense pressure, forcing the hot magma that lies beneath the crust to rise towards the surface. This magma transports minerals that solidify when hydrothermal fluids (or magmatic water) rise and cool off, sometimes creating mineable deposits of valuable minerals.

Subduction zones in the Pacific Ring of Fire host the vast majority of the earth’s porphyry deposits and several epithermal deposits. Porphyry deposits contain copper, gold, and molybdenum, whereas epithermal deposits typically bear gold and silver.

However, turning a deposit into a mine requires much more than just the presence of minerals. Although mineral deposits are found all around the Ring, some regions have produced many more discoveries than others.

The Edge of Discovery: The South Pacific

The South Pacific has proven itself as one of the most productive regions for gold and copper mining along the Ring.

The region hosts the famous Grasberg mine, one of the world’s largest gold and copper mines, along with other prolific discoveries like the Lihir mine in Papua New Guinea, and the Cadia mine in Australia. But as these existing mines deplete, the opportunity lies in making new discoveries.

Fiji: The Next Edge of Discovery on the Pacific Ring of Fire

Fiji has a lot to offer to the mining industry with its prime location along the Pacific Ring of Fire.

The Fijian islands are endowed with rich deposits of gold, copper, and zinc. Fiji’s history of gold mining goes back to the 1930s with the Vatukoula mine, which is still in operation today. Furthermore, Fiji topped the Fraser Institute’s 2018 rankings of mining jurisdictions in Oceania in both investment and policy attractiveness.

Fiji’s government supports ethical exploration because the mining industry brings economic benefits to the country. In fact, gold has consistently been one of Fiji’s largest exports:

| Year | Amount of Gold Exported | Gold (as % Share of Total Exports |

|---|---|---|

| 2010 | 2,015 kg | 9.25% |

| 2011 | 1,621 kg | 7.46% |

| 2012 | 1,584 kg | 6.31% |

| 2013 | 1,098 kg | 4.07% |

| 2014 | 1,245 kg | 3.54% |

| 2015 | 1,252 kg | 4.97% |

| 2016 | 3,777 kg | 6.26% |

| 2017 | 2,461 kg | 6.05% |

| 2018 | 1,378 kg | 5.23% |

| 2019 | 1,840 kg | 4.87% |

Following a period of steady decline between 2010-2015, Fiji’s gold exports peaked in 2016 at 3,777 kg—making up 6.26% of its total exports. In 2019, gold was Fiji’s sixth-largest export, generating more than $50 million in value.

Fiji: Ready for the Next Big Gold Discovery

Fiji remains a hub of exploration activity with several mining companies on the hunt for its next big discovery.

The presence of Vatukoula, Fiji’s largest gold mine containing 10 million ounces of gold, suggests that other large gold deposits are waiting to be found. Although recent discoveries in Fiji do not come close to the Vatukoula’s grand size, it’s only a matter of time before Fiji reveals its treasure.

-

Sponsored3 years ago

Sponsored3 years agoMore Than Precious: Silver’s Role in the New Energy Era (Part 3 of 3)

Long known as a precious metal, silver in solar and EV technologies will redefine its role and importance to a greener economy.

-

Sponsored7 years ago

Sponsored7 years agoThe History and Evolution of the Video Games Market

Everything from Pong to the rise of mobile gaming and AR/VR. Learn about the $100 billion video games market in this giant infographic.

-

Sponsored8 years ago

Sponsored8 years agoThe Extraordinary Raw Materials in an iPhone 6s

Over 700 million iPhones have now been sold, but the iPhone would not exist if it were not for the raw materials that make the technology...

-

Sponsored8 years ago

Sponsored8 years agoThe Industrial Internet, and How It’s Revolutionizing Mining

The convergence of the global industrial sector with big data and the internet of things, or the Industrial Internet, will revolutionize how mining works.