Why Telcos Must Get in the Game for the Rise of Esports

The following content is sponsored by Swarmio Media.

Why Telcos Must Get in the Game for the Rise of Esports

Over the last century, the world’s telecommunications companies have built out the complex infrastructure that makes the information age possible.

Hundreds of billions of dollars has been invested into phone lines, submarine cables, wireless towers, and fiber optics to connect the world. And with 5G innovations in the pipeline, the world has never been able to communicate faster and more effectively.

Despite this impressive accomplishment, telcos find themselves in an awkward situation: their revenue growth is stagnating and margins continue to shrink, all while companies like Netflix are monetizing internet bandwidth around the world.

Today’s infographic is from Swarmio Media, and it highlights challenges faced by telcos — and how they can potentially capitalize on the emergence of esports and a massive gaming market.

A Missed Opportunity

Habits around content consumption can change abruptly, and fast-moving technology companies have been able to capitalize on these changes.

That’s why, in recent years, there’s been a boom in over-the-top (OTT) media services (Netflix, Amazon Prime, Skype, etc.) that have found effective ways to operate on top of the telco infrastructure, streaming content or providing VoIP services to end consumers.

| Television | Voice & Messaging | Audio | |

|---|---|---|---|

| Example OTT services | - Netflix - Disney+ - Amazon Prime - YouTube - HBO | - Skype - Messenger - Viber | - Spotify - Apple Music - Podcasts - Internet Radio - YouTube |

| Global market size (2018) | $68.7 billion | $26.7 billion | $8.9 billion |

| Growth rate (2017-2018): | 28% | 15% | 33% |

Although telcos arguably missed the boat on video streaming, voice, and messaging, there is now an emerging segment that could help fill the gap.

The rising popularity of esports could be the multi-billion dollar industry that provides telcos a much-needed growth area to better monetize their infrastructure.

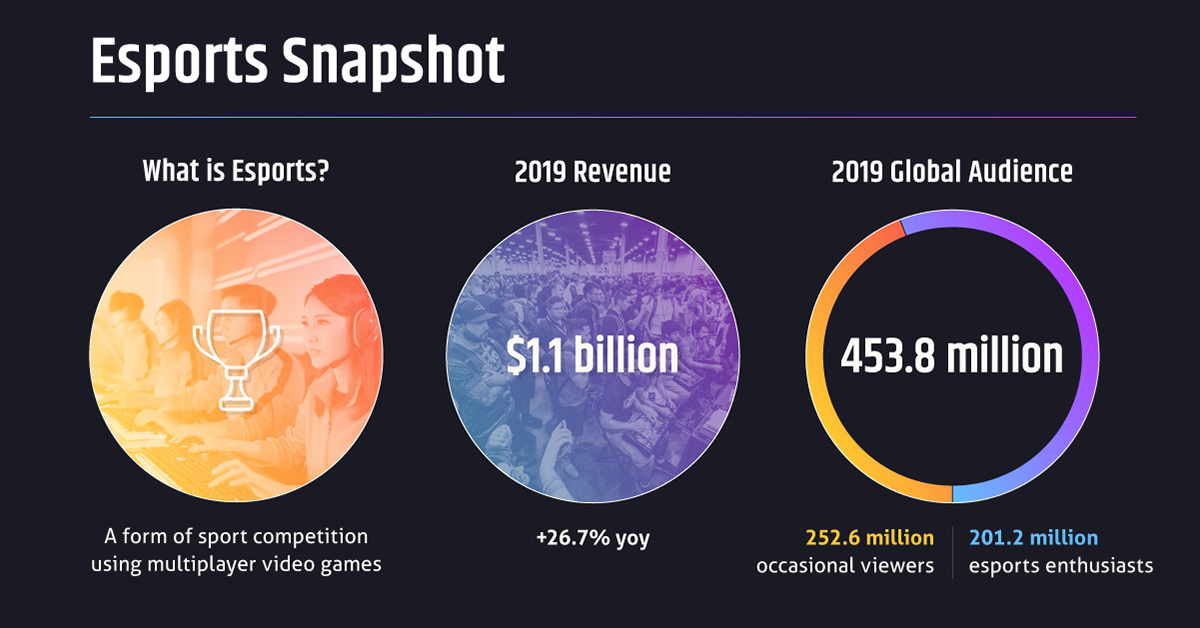

The Esports Boom

In recent years, the growth in professional gaming has been explosive.

Already worth over $1 billion, the market is projected by experts to triple by 2025. Esports is regularly packing stadiums with avid fans, spawning new professional teams, and selling massive sponsorship deals.

This boom in esports – and in online multiplayer gaming in general — has created a commercial audience of digital natives that is both young and affluent. It’s a growing segment that sees gaming as a lifestyle, and they see professional esports gamers and personalities as their heroes.

The Need For Speed

Any multiplayer gamer will tell you that there is one surefire way to ruin the gaming experience: high latencies (or as they call it, “lag”). This is an area telecoms are uniquely positioned to help with, especially with the advent of edge computing technology and 5G.

When it comes to online gaming, a sophisticated edge computing system will be able to detect where each player is located, while creating a server in an optimal location that provides all the players with the same high bandwidth, low latency, and experience.

By leveraging technology that enables edge computing at scale, forward-looking telcos can take gamers to where they want to go – and with plenty of value-adds.

Living on the Edge

To compete against growing outside threats like Netflix and Google, telcos must make bold investments in enabling technologies that bring edge computing to their customers at scale.

Beyond acting as the gatekeeper to lightning fast connections, telcos can take advantage of esports and gaming by building internal online communities, delivering tailored esports content, and enabling and promoting esports tournaments.

If done right, this can help telcos engage with digital natives, create meaningful experiences, win lifelong customers and advocates, and maximize average revenue per user (ARPU).

For many of the 2.5 billion gamers globally, there is little reason to be loyal to a telco – until now.

-

Sponsored3 years ago

Sponsored3 years agoMore Than Precious: Silver’s Role in the New Energy Era (Part 3 of 3)

Long known as a precious metal, silver in solar and EV technologies will redefine its role and importance to a greener economy.

-

Sponsored7 years ago

Sponsored7 years agoThe History and Evolution of the Video Games Market

Everything from Pong to the rise of mobile gaming and AR/VR. Learn about the $100 billion video games market in this giant infographic.

-

Sponsored8 years ago

Sponsored8 years agoThe Extraordinary Raw Materials in an iPhone 6s

Over 700 million iPhones have now been sold, but the iPhone would not exist if it were not for the raw materials that make the technology...

-

Sponsored8 years ago

Sponsored8 years agoThe Industrial Internet, and How It’s Revolutionizing Mining

The convergence of the global industrial sector with big data and the internet of things, or the Industrial Internet, will revolutionize how mining works.