Decoding the Economics of a Soft Landing

Decoding the Economics of a Soft Landing

Is a soft landing on the horizon?

So far, the U.S. economy has illustrated unexpected strength, with S&P 500 returns up over 18% year-to-date. A resilient labor market and cooling inflation have improved the odds of the U.S. avoiding a recession, in spite of 11 interest rate hikes since March 2022.

This graphic, sponsored by New York Life Investments, shows three key factors that could impact whether the U.S. achieves a soft landing.

What is a Soft Landing?

Historically, after a steep rise in interest rates, the U.S. economy often falls into recession.

Still, there have been some exceptions where it avoided a sharp downturn. The most notable example was in 1994-1995, when the Fed raised interest rates seven times in one year without triggering a recession.

Consider the following general definitions:

- Soft landing: The Federal Reserve raises interest rates just enough to stabilize inflation. A recession is avoided, or only a minor one occurs.

- Hard landing: The Federal Reserve raises interest rates too far, excessively slowing the economy and causing a recession.

Below, we show the factors having an outsized influence on the health of the U.S. economy today.

1. The Labor Market

The U.S. labor market is an important indicator of economic health.

In July, there were 1.7 job openings for every unemployed person, highlighting strong demand for workers. In fact, almost 4 million jobs have been added since 2020, recovering the majority of jobs that were lost due to the pandemic.

At the same time, the U.S. unemployment rate remains near five-decade lows, sitting at just 3.5% as of July.

Why Does This Matter?

- Wages have been steadily rising, although not fast enough to significantly impact inflation.

- With no shortage of job options, this suggests economic strength, supporting a soft landing.

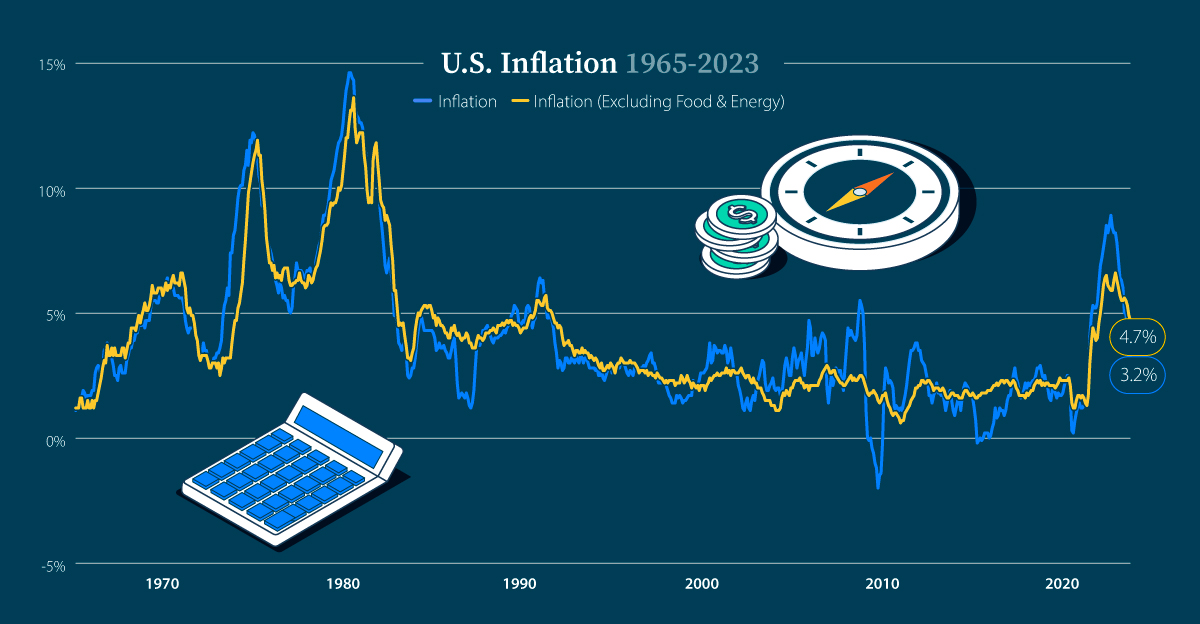

2. Inflation

Inflation has fallen to 3.2% in July, down from a peak of 8.9% seen in June 2022.

We can see in the table below that inflation has been stabilizing, but core inflation, which excludes food and energy, has been declining at a slower pace. The Fed watches core inflation more closely since it is less affected by short-term price fluctuations, and is therefore a better barometer of where prices are headed.

| Date | Inflation (%) | Inflation Excluding Food & Energy (%) |

|---|---|---|

| Jul 2023 | 3.2% | 4.7% |

| Jun 2023 | 3.1% | 4.9% |

| May 2023 | 4.1% | 5.3% |

| Apr 2023 | 5.0% | 5.5% |

| Mar 2023 | 5.0% | 5.6% |

| Feb 2023 | 6.0% | 5.5% |

| Jan 2023 | 6.3% | 5.5% |

| Dec 2022 | 6.4% | 5.7% |

| Nov 2022 | 7.1% | 6.0% |

| Oct 2022 | 7.8% | 6.3% |

| Sep 2022 | 8.2% | 6.6% |

| Aug 2022 | 8.2% | 6.3% |

| Jul 2022 | 8.4% | 5.9% |

| Jun 2022 | 8.9% | 5.9% |

| May 2022 | 8.5% | 6.0% |

| Apr 2022 | 8.2% | 6.1% |

| Mar 2022 | 8.5% | 6.5% |

| Feb 2022 | 8.0% | 6.4% |

| Jan 2022 | 7.6% | 6.1% |

| Dec 2021 | 7.2% | 5.5% |

| Nov 2021 | 6.9% | 5.0% |

| Oct 2021 | 6.2% | 4.6% |

| Sep 2021 | 5.4% | 4.0% |

| Aug 2021 | 5.2% | 3.9% |

| Jul 2021 | 5.2% | 4.2% |

| Jun 2021 | 5.3% | 4.4% |

| May 2021 | 4.9% | 3.8% |

| Apr 2021 | 4.1% | 3.0% |

| Mar 2021 | 2.6% | 1.7% |

| Feb 2021 | 1.7% | 1.3% |

| Jan 2021 | 1.4% | 1.4% |

| Dec 2020 | 1.3% | 1.6% |

| Nov 2020 | 1.2% | 1.7% |

| Oct 2020 | 1.2% | 1.6% |

| Sep 2020 | 1.4% | 1.7% |

| Aug 2020 | 1.3% | 1.7% |

| Jul 2020 | 1.0% | 1.5% |

| Jun 2020 | 0.7% | 1.2% |

| May 2020 | 0.2% | 1.2% |

| Apr 2020 | 0.3% | 1.4% |

| Mar 2020 | 1.5% | 2.1% |

| Feb 2020 | 2.3% | 2.4% |

| Jan 2020 | 2.5% | 2.3% |

Housing costs accounted for 90% of inflation’s increase in July, while food and energy costs increased slightly. And even though inflation remains above the 2% target set by the Federal Reserve, we can see that price pressures continue to be easing.

Why Does This Matter?

- If inflation continues to subside, the Federal Reserve may be able to cut interest rates.

- This could help pave the way toward a soft landing as lower borrowing costs support stock market performance.

3. Consumer Savings

Household spending makes up roughly two-thirds of U.S. GDP.

During the pandemic, excess savings—those that go beyond expected savings—hit historic levels. Analysis from the Federal Reserve shows that excess savings hit a peak of $2.1 trillion in August 2021, but have since fallen to $190 billion as of June this year.

Americans also had access to more liquid funds than before the pandemic. The table below shows household liquid assets by income level compared to pre-pandemic levels.

| Household Liquid Assets | Pre-Pandemic Average 2016-2019 | Q4 2022 |

|---|---|---|

| Lowest Income Level Households | 24% | 33% |

| 2nd | 25% | 27% |

| 3rd | 19% | 21% |

| 4th | 14% | 16% |

| Highest Income Level Households | 13% | 15% |

Household income distribution from lowest 20% to highest 20%.

These liquid assets have likely provided a buffer for consumers in the face of rising costs and interest expenses. More liquid assets mean that consumers have the ability to spend more, supporting economic growth.

Why Does This Matter?

- Excess savings are projected to bolster consumer spending through the third quarter of 2023.

- This will support business investment and help prevent a rise in unemployment.

Soft Landing Playbook

Despite these positive signals, the full effects of rising interest rates may take time to filter through the economy. With this in mind, the following investments could help investors navigate interest rate uncertainty and mixed recession forecasts:

- Value equities: Historically have more stable earnings than growth equities.

- Pairing longer-dated and short-dated bonds: This type of bond strategy allows for investors to pivot if interest rates change, and to lock-in higher rates over longer horizons.

Together, these investments may allow investors to weather an unpredictable market environment.

Explore more investment insights with New York Life Investments.

-

Business2 hours ago

Business2 hours agoThe Top Private Equity Firms by Country

This map visualizes the leading private equity firms of major countries, ranked by capital raised over the past five years.

-

Economy5 days ago

Economy5 days agoEconomic Growth Forecasts for G7 and BRICS Countries in 2024

The IMF has released its economic growth forecasts for 2024. How do the G7 and BRICS countries compare?

-

Markets2 weeks ago

Markets2 weeks agoU.S. Debt Interest Payments Reach $1 Trillion

U.S. debt interest payments have surged past the $1 trillion dollar mark, amid high interest rates and an ever-expanding debt burden.

-

Business2 weeks ago

Business2 weeks agoRanked: The Largest U.S. Corporations by Number of Employees

We visualized the top U.S. companies by employees, revealing the massive scale of retailers like Walmart, Target, and Home Depot.

-

Markets3 weeks ago

Markets3 weeks agoThe Top 10 States by Real GDP Growth in 2023

This graphic shows the states with the highest real GDP growth rate in 2023, largely propelled by the oil and gas boom.

-

Markets3 weeks ago

Markets3 weeks agoRanked: The World’s Top Flight Routes, by Revenue

In this graphic, we show the highest earning flight routes globally as air travel continued to rebound in 2023.