Politics

Charted: Trust in Government Institutions by G7 Countries

![]() See this visualization first on the Voronoi app.

See this visualization first on the Voronoi app.

Trust in Government Institutions by G7 Countries

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

How much do you trust the government, and its various institutions?

It’s likely that your level of confidence probably depends on a wide range of factors, such as perceived competency, historical context, economic performance, accountability, social cohesion, and transparency.

And for these same reasons, trust levels in government institutions also change all the time, even in the world’s most developed countries: the G7.

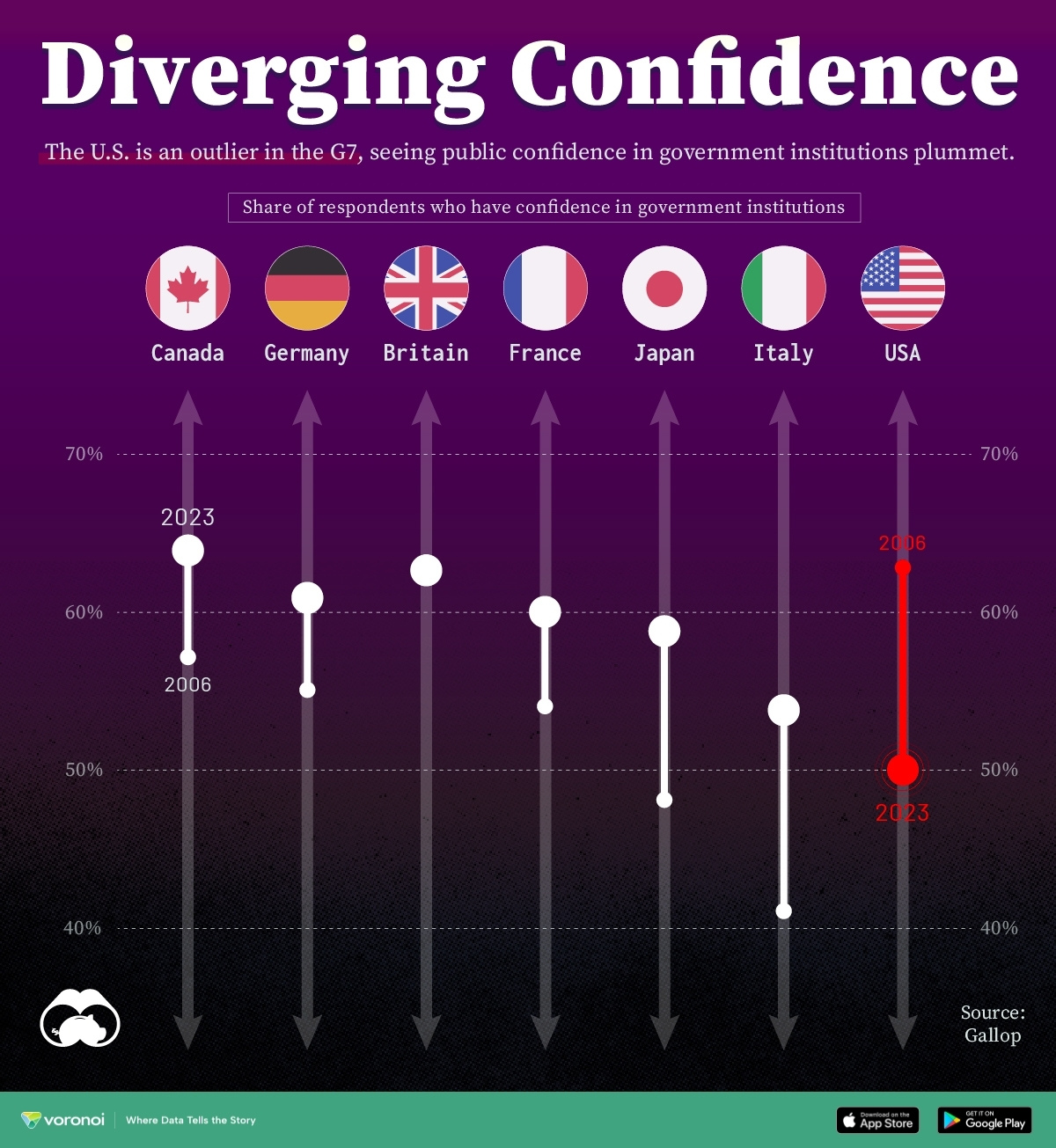

Confidence in Government by G7 Countries (2006-2023)

This chart looks at the changes in trust in government institutions between the years 2006 and 2023, based on data from a multi-country Gallup poll.

Specifically, this dataset aggregates confidence in multiple national institutions, including the military, the judicial system, the national government, and the integrity of the electoral system.

| Country | Confidence (2006) | Confidence (2023) | Change (p.p.) |

|---|---|---|---|

| Canada | 57% | 64% | +7 |

| Britain | 63% | 63% | +0 |

| Germany | 55% | 61% | +6 |

| France | 54% | 60% | +6 |

| Japan | 48% | 59% | +11 |

| Italy | 41% | 54% | +13 |

| United States | 63% | 50% | -13 |

What’s interesting here is that in the G7, a group of the world’s most developed economies, there is only one country bucking the general trend: the United States.

Across most G7 countries, confidence in institutions has either improved or stayed the same between 2006 and 2023. The largest percentage point (p.p.) increases occur in Italy and Japan, which saw +13 p.p. and +11 p.p. increases in trust over the time period.

In the U.S., however, confidence in government institutions has fallen by 13 p.p. over the years. What happened?

Key Figures on U.S. Trust in Institutions

In 2006, the U.S. was tied with the UK as having the highest confidence in government institutions, at 63%.

But here’s where the scores stand in 2023, across various institutions:

| 🇺🇸 Institutions | Confidence (2023) |

|---|---|

| Military | 81% |

| Judiciary | 42% |

| National Government | 30% |

| Elections | 44% |

| Overall | 49% |

Based on this data, it’s clear that the U.S. lags behind in three key indicators: confidence in the national government, confidence in the justice system, and confidence in fair elections. It ranked in last place for each indicator in the G7.

One other data point that stands out: despite leading the world in military spending, the U.S. is only the third most confident in its military in the G7. It lags behind France (86%) and the United Kingdom (83%).

China

Which Countries Have the Most Economic Influence in Southeast Asia?

One country dominates this survey of who has the most economic influence in the region.

Countries With the Most Economic Influence in Southeast Asia

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

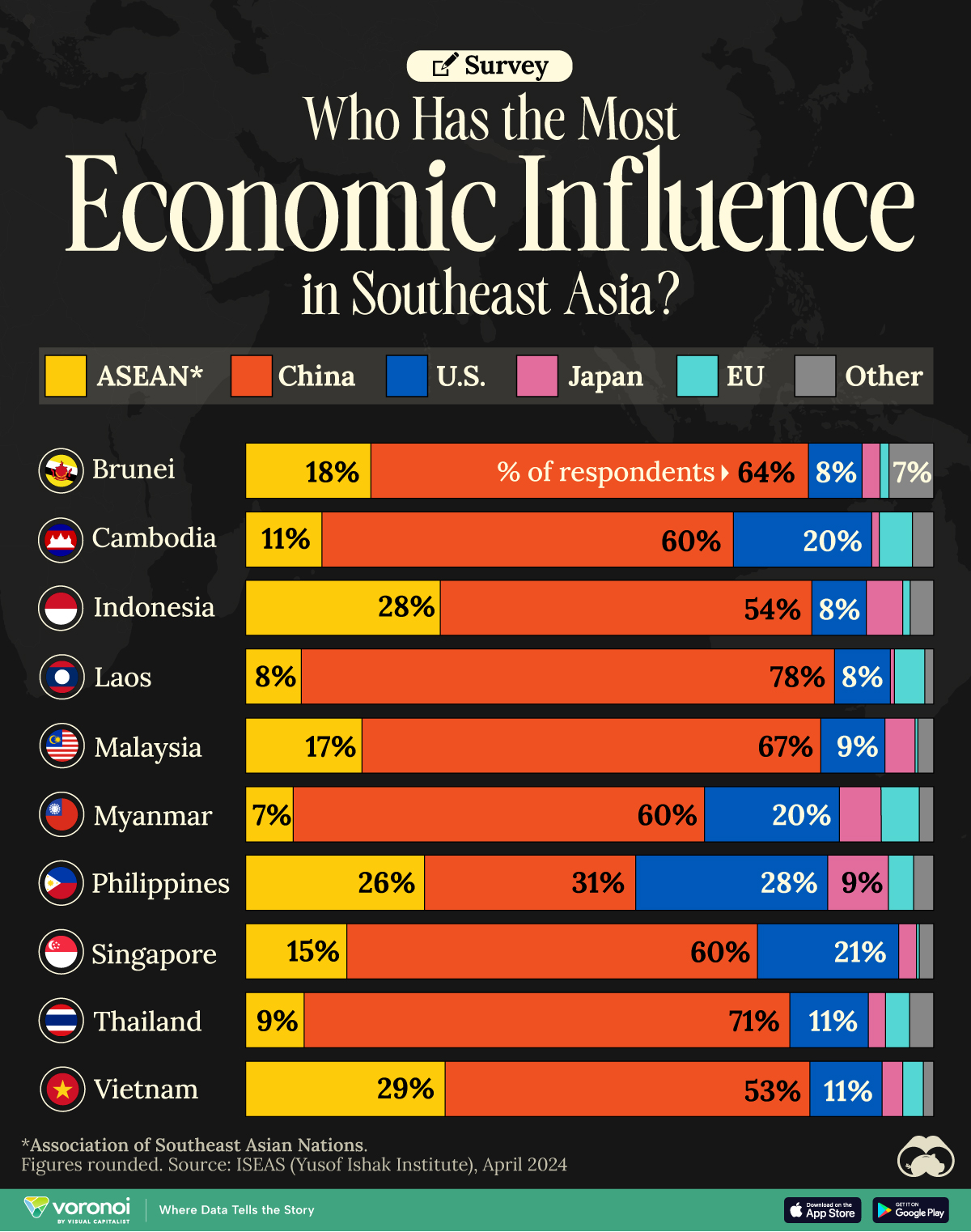

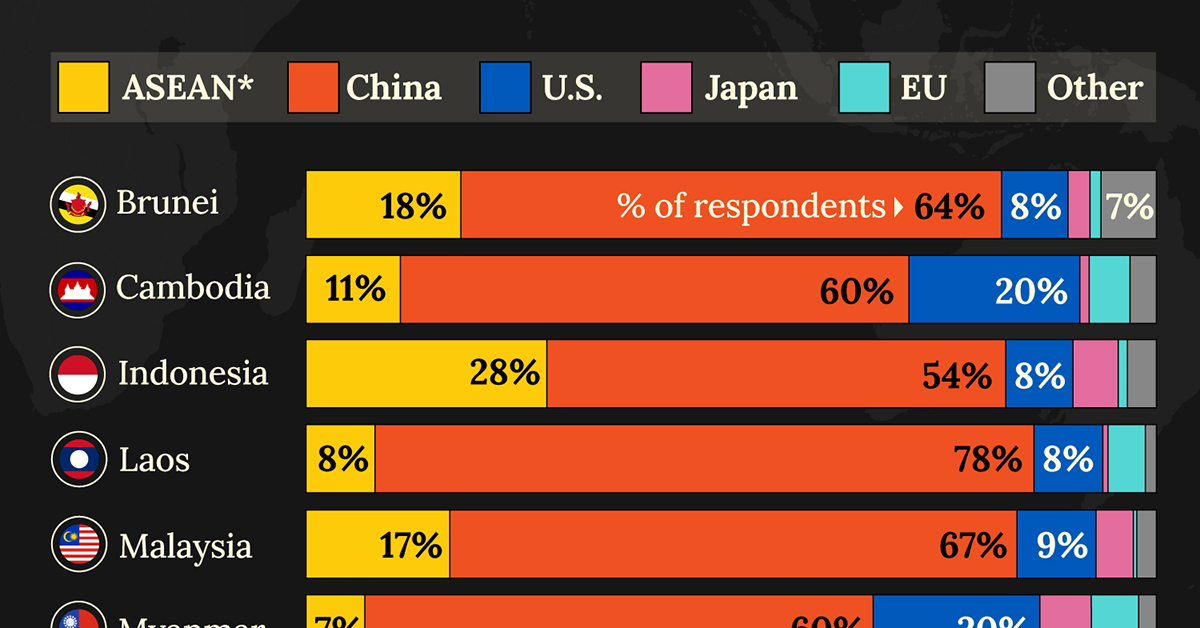

This chart visualizes the results of a 2024 survey conducted by the ASEAN Studies Centre at the ISEAS-Yusof Ishak Institute.

Nearly 2,000 respondents from 10 countries were asked to select which country/region they believe has the most influential economic power in Southeast Asia.

The countries surveyed are all member states of the Association of Southeast Asian Nations (ASEAN), a political and economic union of 10 countries in Southeast Asia.

Southeast Asia Perceptions: Who’s Got Economic Influence?

Across all ASEAN nations, China is regarded as the region’s most influential economic power.

Laos and Thailand had the highest share of respondents picking China, at 78% and 71% respectively. As the report points out, China is Laos’ largest foreign investor as well as its top export market.

| Country | 🇨🇳 China | 🌏 ASEAN | 🇺🇸 U.S. |

|---|---|---|---|

| 🇧🇳 Brunei | 64% | 18% | 8% |

| 🇰🇭 Cambodia | 60% | 11% | 20% |

| 🇮🇩 Indonesia | 54% | 28% | 8% |

| 🇱🇦 Laos | 78% | 8% | 8% |

| 🇲🇾 Malaysia | 67% | 17% | 9% |

| 🇲🇲 Myanmar | 60% | 7% | 20% |

| 🇵🇭 Philippines | 31% | 26% | 28% |

| 🇸🇬 Singapore | 60% | 15% | 21% |

| 🇹🇭 Thailand | 71% | 9% | 11% |

| 🇻🇳 Vietnam | 53% | 29% | 11% |

Note: Percentages are rounded.

Other ASEAN countries usually score highly as well, along with the United States.

It’s only in the Philippines, where China (31%), the U.S. (28%) and ASEAN (26%) were perceived as having a similar amount of influence.

ASEAN, Japan, and the EU

Filipinos also rated Japan’s economic influence the highest (9%) compared to those surveyed in other ASEAN countries. In 2023, the Southeast Asian bloc celebrated 50 years of friendship with Japan, marking it as one of their most important “dialogue partners.”

| Country | 🇯🇵 Japan | 🇪🇺 EU | 🌐 Other |

|---|---|---|---|

| 🇧🇳 Brunei | 3% | 1% | 7% |

| 🇰🇭 Cambodia | 1% | 5% | 3% |

| 🇮🇩 Indonesia | 5% | 1% | 3% |

| 🇱🇦 Laos | 1% | 4% | 1% |

| 🇲🇾 Malaysia | 4% | 0% | 2% |

| 🇲🇲 Myanmar | 6% | 6% | 2% |

| 🇵🇭 Philippines | 9% | 4% | 3% |

| 🇸🇬 Singapore | 3% | 0% | 2% |

| 🇹🇭 Thailand | 3% | 4% | 4% |

| 🇻🇳 Vietnam | 3% | 3% | 2% |

Note: Percentages are rounded. Other countries include: Australia, South Korea, India, and the UK.

The EU also received single-percentage responses, its highest share coming from Myanmar (6%), Cambodia (5%), and Laos (4%).

Finally, the report contrasted China’s robust economic influence with concerns about its growing impact in the region. Respondents from Vietnam (88%), Myanmar (88%), and Thailand (80%) had the highest levels of concern, despite their countries’ strong trade ties with China.

-

Healthcare2 weeks ago

Healthcare2 weeks agoWhich Countries Have the Highest Infant Mortality Rates?

-

Misc1 week ago

Misc1 week agoVisualizing Global Losses from Financial Scams

-

population1 week ago

population1 week agoMapped: U.S. States By Number of Cities Over 250,000 Residents

-

Business1 week ago

Business1 week agoCharted: How the Logos of Select Fashion Brands Have Evolved

-

United States1 week ago

United States1 week agoMapped: Countries Where Recreational Cannabis is Legal

-

Misc1 week ago

Misc1 week agoVisualized: Aircraft Carriers by Country

-

Culture1 week ago

Culture1 week agoHow Popular Snack Brand Logos Have Changed

-

Mining2 weeks ago

Mining2 weeks agoVisualizing Copper Production by Country in 2023