Agriculture

Visualizing a Rapidly Changing Global Diet

Visualizing a Rapidly Changing Global Diet

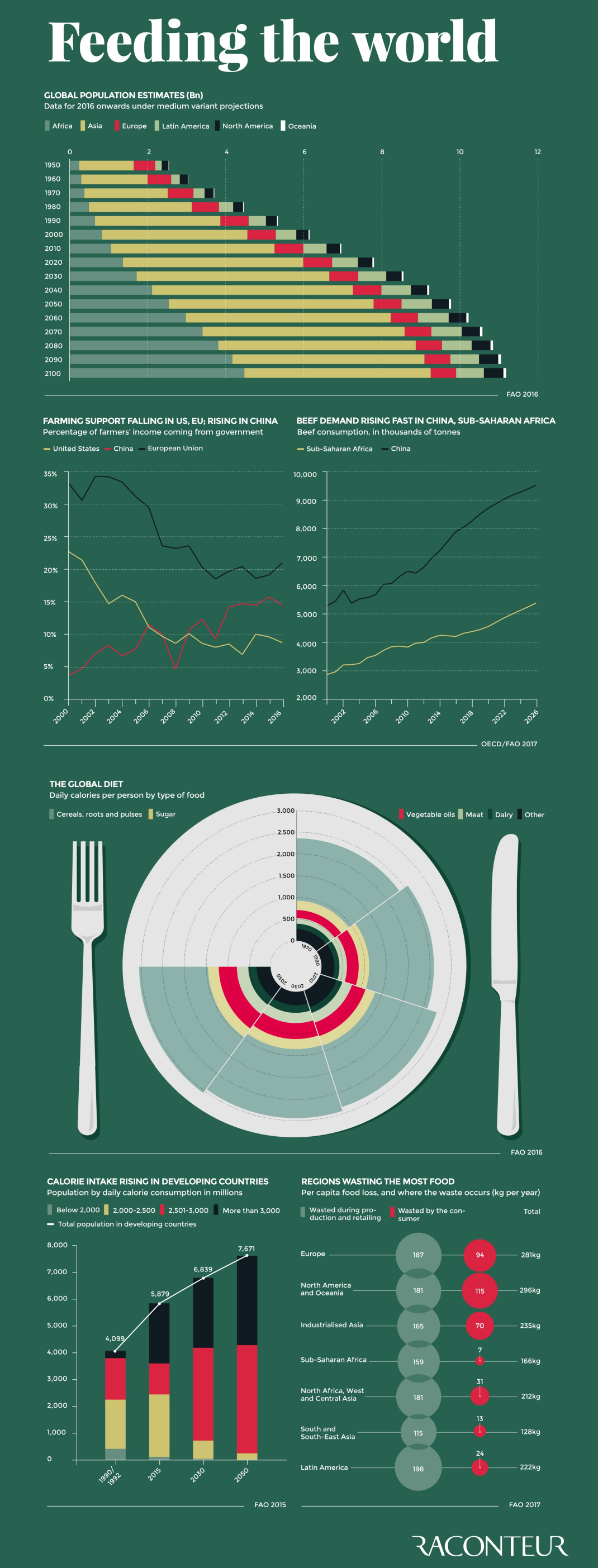

By 2050, there will be two billion more mouths to feed than today.

The increase in food supply required to feed this many people is difficult to fathom, but even that would just be scratching the surface of our future food needs.

Today’s infographic, which comes from Raconteur, makes it clear that the challenge of feeding the global population is actually magnitudes greater. The global diet is changing rapidly in both size and composition, especially in developing countries in Africa and Asia.

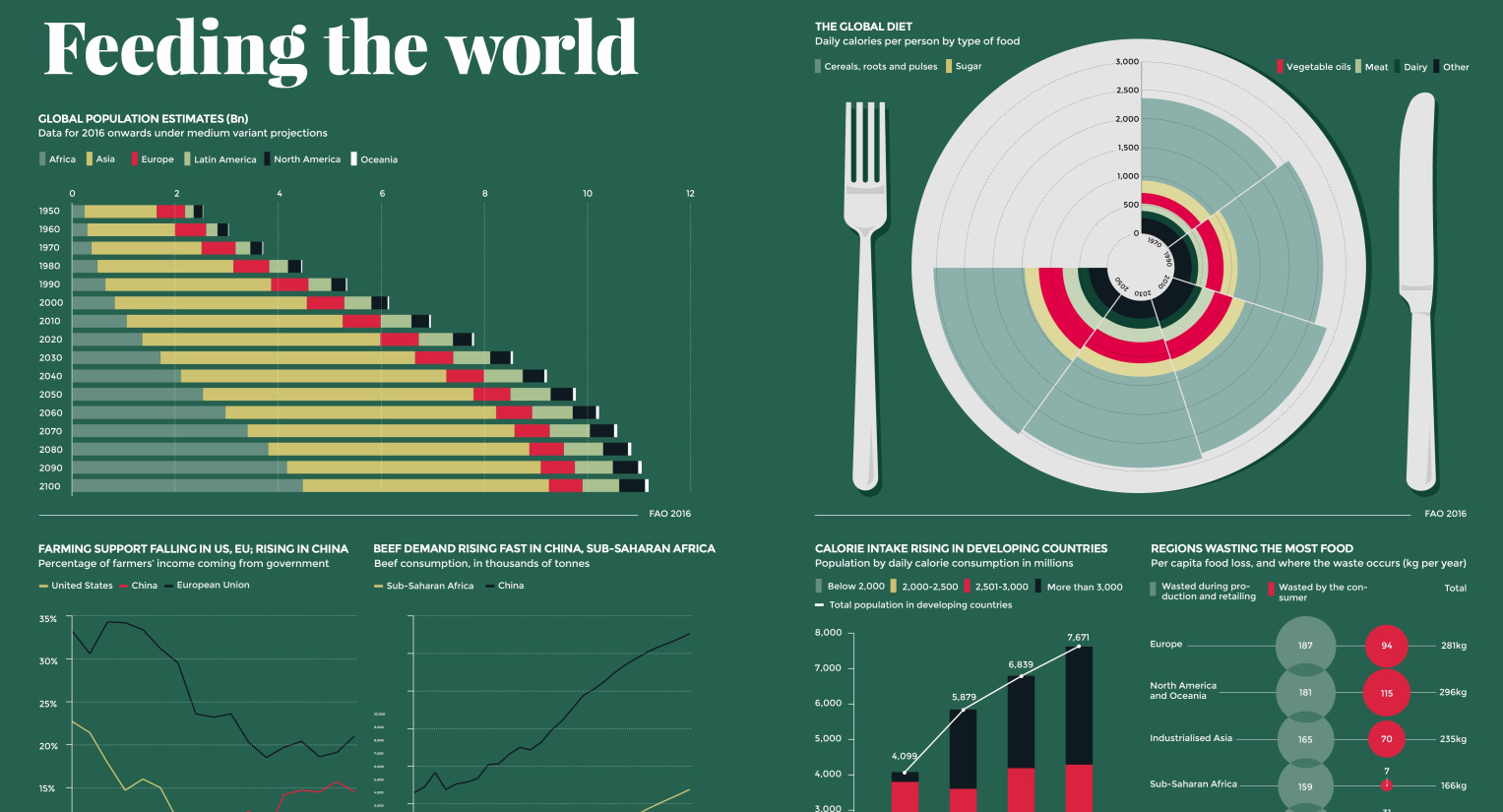

The Global Diet

Right now, the average person consumes close to 3,000 calories per day – with the lion’s share coming from grains such as wheat, corn, or rice.

| Food | Avg. Daily Calories per Person (Global, 2011) | % of Diet |

|---|---|---|

| Grain | 1,296 | 45.2% |

| Sugar & Fat | 570 | 19.9% |

| Produce | 327 | 11.4% |

| Meat | 272 | 9.5% |

| Dairy & Eggs | 235 | 8.2% |

| Other | 170 | 5.9% |

| Total Diet | 2,870 | 100% |

However, the amount of food consumed by each person is growing around the world.

Between 2015 and 2030, it’s estimated that on a global basis, each person will be consuming an extra 110 calories per day.

Meat as a Staple

Increasing wealth and rising populations are key drivers for meat consumption in developing countries.

In China, which is already the world’s largest pork market, consumption of beef is expected to nearly double in the period between 2000 and 2026. In Sub-Saharan Africa, numbers are similar.

While beef is already extremely popular in many high-income economies, it is not the most sustainable food to produce. Beef needs more water and land per pound than almost any other protein source – but that’s not stopping people around the world in developing economies from eating it in greater amounts.

Meanwhile, in India, about one-third of the population is vegetarian – yet the country is turning into a major driver of new meat demand.

Since 2009, India’s annual disposable income has improved by 95 percent and meat consumption has increased by nearly 50 percent during the same time period.

– Anastasia Alieva, Head of Fresh Food Research at Euromonitor International

Outside the Box

To meet new demand for food, scientists are starting to think outside the box.

For an in-depth look at new technology envisioned for food production – including automated vertical farms, aquaponics, in vitro meats, and artificial animal products – make sure to visit the following infographic on the future of food.

Markets

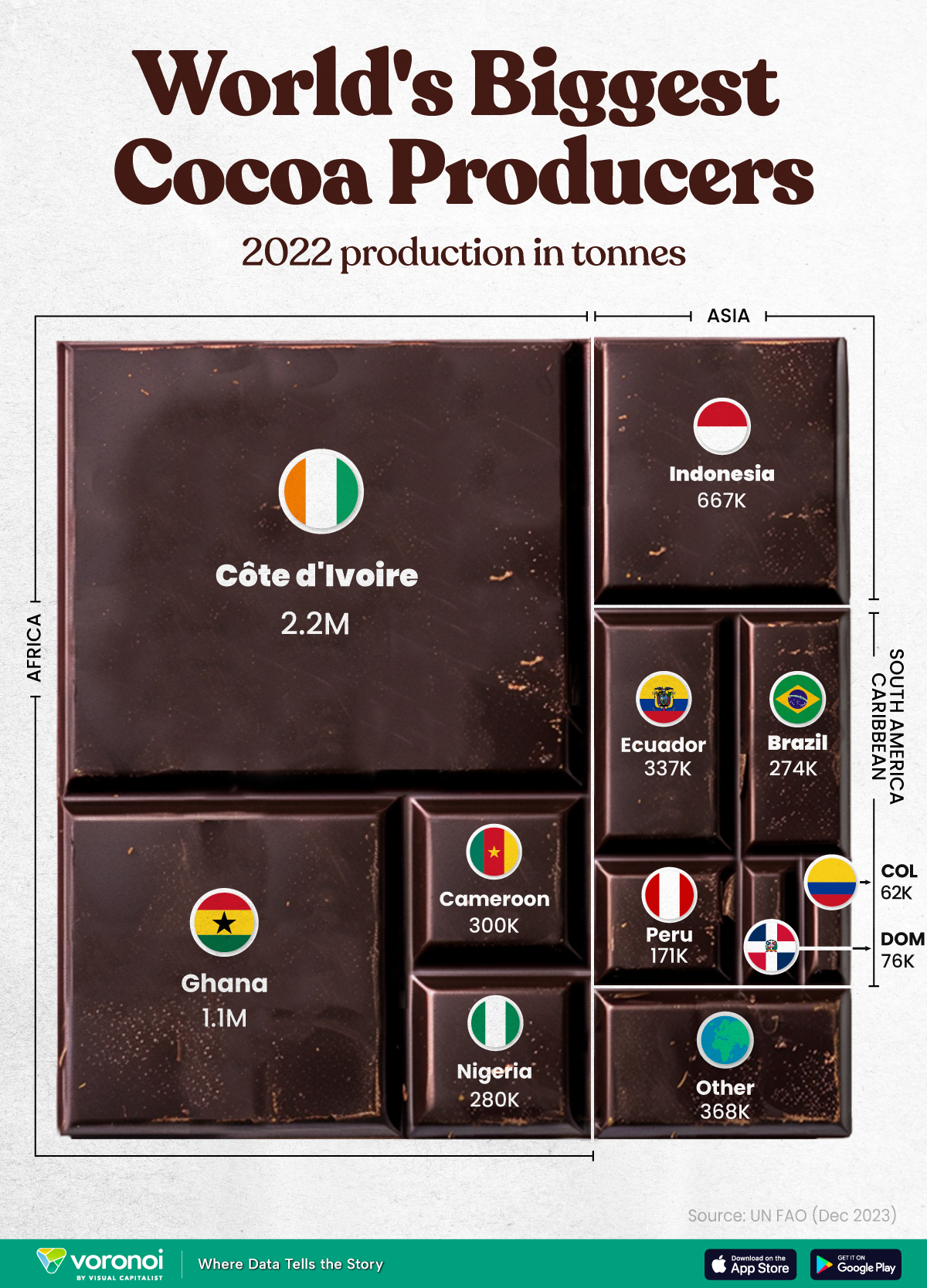

The World’s Top Cocoa Producing Countries

Here are the largest cocoa producing countries globally—from Côte d’Ivoire to Brazil—as cocoa prices hit record highs.

The World’s Top Cocoa Producing Countries

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

West Africa is home to the largest cocoa producing countries worldwide, with 3.9 million tonnes of production in 2022.

In fact, there are about one million farmers in Côte d’Ivoire supplying cocoa to key customers such as Nestlé, Mars, and Hershey. But the massive influence of this industry has led to significant forest loss to plant cocoa trees.

This graphic shows the leading producers of cocoa, based on data from the UN FAO.

Global Hotspots for Cocoa Production

Below, we break down the top cocoa producing countries as of 2022:

| Country | 2022 Production, Tonnes |

|---|---|

| 🇨🇮 Côte d'Ivoire | 2.2M |

| 🇬🇭 Ghana | 1.1M |

| 🇮🇩 Indonesia | 667K |

| 🇪🇨 Ecuador | 337K |

| 🇨🇲 Cameroon | 300K |

| 🇳🇬 Nigeria | 280K |

| 🇧🇷 Brazil | 274K |

| 🇵🇪 Peru | 171K |

| 🇩🇴 Dominican Republic | 76K |

| 🌍 Other | 386K |

With 2.2 million tonnes of cocoa in 2022, Côte d’Ivoire is the world’s largest producer, accounting for a third of the global total.

For many reasons, the cocoa trade in Côte d’Ivoire and Western Africa has been controversial. Often, farmers make about 5% of the retail price of a chocolate bar, and earn $1.20 each day. Adding to this, roughly a third of cocoa farms operate on forests that are meant to be protected.

As the third largest producer, Indonesia produced 667,000 tonnes of cocoa with the U.S., Malaysia, and Singapore as major importers. Overall, small-scale farmers produce 95% of cocoa in the country, but face several challenges such as low pay and unwanted impacts from climate change. Alongside aging trees in the country, these setbacks have led productivity to decline.

In South America, major producers include Ecuador and Brazil. In the early 1900s, Ecuador was the world’s largest cocoa producing country, however shifts in the global marketplace and crop disease led its position to fall. Today, the country is most known for its high-grade single-origin chocolate, with farms seen across the Amazon rainforest.

Altogether, global cocoa production reached 6.5 million tonnes, supported by strong demand. On average, the market has grown 3% annually over the last several decades.

-

Markets1 week ago

Markets1 week agoU.S. Debt Interest Payments Reach $1 Trillion

-

Business2 weeks ago

Business2 weeks agoCharted: Big Four Market Share by S&P 500 Audits

-

Markets2 weeks ago

Markets2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Demographics2 weeks ago

Demographics2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023