Markets

Understanding the Disconnect Between Consumers and the Stock Market

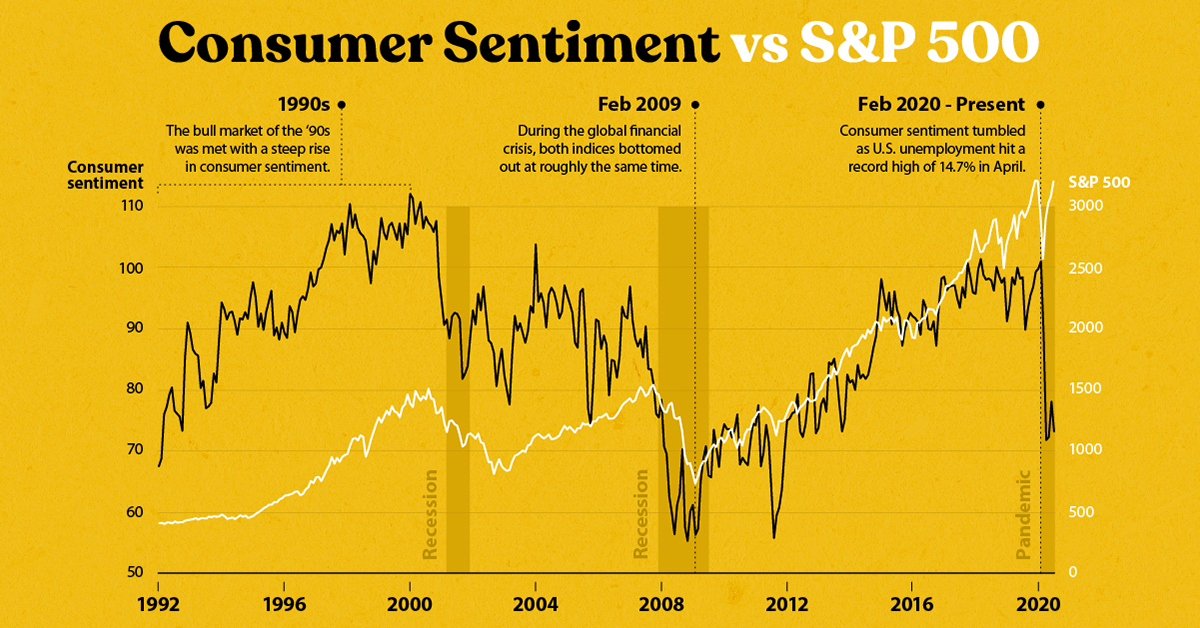

The Disconnect Between Consumers and Stock Markets

Consumer sentiment indices are relatively accurate indicators for the outlook of an economy. They rise during periods of growth as consumers become more financially confident, and fall during recessions as consumers cut back on discretionary spending.

Since the direction of the overall economy also affects stock markets, measures of consumer sentiment have historically moved in tandem with major indices like the S&P 500. Since the COVID-19 pandemic began, however, consumers and stock markets have become noticeably disjointed from one another.

To help us understand why this may be the case, this infographic charts the University of Michigan’s Index of Consumer Sentiment against the S&P 500, before diving into potential underlying factors for their divergence.

A Tale of Two Indices

Before we compare these two indices, it’s helpful to first understand how they’re comprised.

The Index of Consumer Sentiment

The University of Michigan’s Index of Consumer Sentiment (ICS) is derived from a monthly survey of consumers that aims to get a snapshot of personal finances, business conditions, and buying conditions in the market.

The survey consists of five questions (paraphrased):

- Are you better or worse off financially compared to a year ago?

- Will you be better or worse off financially a year in the future?

- Will business conditions during the next year be good, bad, or other?

- Will business conditions over the next five years be good, bad, or other?

- Is it a good time to make large purchases such as major household appliances?

A score for each of these questions is calculated based on the percent of favorable and nonfavorable replies. The scores are then aggregated to arrive at the final index value, relative to 6.8—the 1966 base period value.

The S&P 500

The S&P 500 is a market capitalization-weighted index of the 500 largest publicly traded U.S. companies. A company’s market capitalization is calculated as its current stock price multiplied by its total number of outstanding shares.

Market caps change over time, with movements determined by daily stock price fluctuations, the issuance of new stock, or the repurchase of existing shares (also known as share buybacks).

The COVID-19 Divergence

Throughout past market cycles, these two indices have displayed some degree of correlation.

During the bull market of the ‘90s, the S&P 500 generated an astonishing 417% return, and was accompanied by a 75% increase in consumer sentiment. Critically, both indices also peaked at roughly the same time. The ICS began to decline after reaching its record high of 112.0 in January 2000, while the S&P 500 began to falter in August that same year.

Fast forwarding to 2020, we can see that these indices have responded quite differently during the pandemic so far:

| Index | Jan 2020 | Feb 2020 | Mar 2020 | Apr 2020 | May 2020 | June 2020 | July 17, 2020 |

|---|---|---|---|---|---|---|---|

| ICS Value | 99.8 | 101 | 89.1 | 71.8 | 72.3 | 78.1 | 73.2 |

| ICS YTD | 0.5% | 1.7% | -10.3% | -27.7% | -27.2% | -21.4% | -26.3% |

| S&P 500 Value | 3225.5 | 2954.2 | 2584.6 | 2912.4 | 3044.3 | 3100.3 | 3224.7 |

| S&P 500 YTD | -0.2% | -8.6% | -20.0% | -9.9% | -5.8% | -4.0% | -0.2% |

All figures as of month end unless otherwise specified. Source: Yahoo Finance

The ICS has not yet recovered from its initial decline beginning in March, whereas the S&P 500 has seemingly bounced back during the same time frame.

Examining the Disconnect

Why are stock markets failing to recognize the hardships that consumers are feeling? Let’s examine two central factors behind this disconnect.

Reason 1: Tech’s Dominance of the S&P 500

Recall that a company’s weight in the S&P 500 is determined by its market cap. This means that certain sectors can form a larger part of the index than others. Here’s how each sector sizes up:

| S&P 500 Sector | Index weight as of June 30, 2020 (%) |

|---|---|

| Information technology | 27.5% |

| Health care | 14.6% |

| Consumer discretionary | 10.8% |

| Communication services | 10.8% |

| Financials | 10.1% |

| Industrials | 8.0% |

| Consumer staples | 7.0% |

| Utilities | 3.1% |

| Real estate | 2.8% |

| Energy | 2.8% |

| Materials | 2.5% |

Source: S&P Global

Based on this breakdown, we can see that the information technology (IT) sector accounts for over a quarter of the S&P 500. With a weighting of 27.5%, the sector alone is bigger than the bottom six combined (Industrials to Materials).

This inequality means the performance of the IT sector has a stronger relative impact on the index’s overall returns. Within IT, we can highlight the FAANGM subset of stocks, which include some of America’s biggest names in tech:

| Stock | Market Cap as of June 30, 2020 ($) |

|---|---|

| Apple | $1.6 trillion |

| Microsoft | $1.5 trillion |

| Amazon | $1.4 trillion |

| $930 billion | |

| $668 billion | |

| Netflix | $200 billion |

| S&P 500 average | $53 billion |

Source: Yahoo Finance

These companies have grown rapidly over the past decade, and continue to perform strongly during the pandemic. If this trend continues, the S&P 500 could skew even further towards the IT sector, and become less representative of America’s overall economy.

Reason 2: The U.S. Federal Reserve

Stock prices typically reflect a company’s future earnings prospects, meaning they are influenced, to a degree, by the outlook for the broader economy.

With an ongoing pandemic and steep decline in consumer sentiment, it’s reasonable to believe that many company prospects would look bleak. This is especially true for consumer cyclicals—companies like automobile manufacturers that rely on discretionary spending.

In a somewhat controversial move, the U.S. Federal Reserve has stepped in to counter these effects by creating the Secondary Market Corporate Credit Facility (SMCCF). This facility operates two programs which ensure businesses have access to funding during the pandemic.

Corporate Bond Purchase Program

The SMCCF is currently buying corporate bonds from an index of nearly 800 companies. Of the ten largest recipients of this program, five are categorized as consumer cyclical:

| Issuer | Category | Index Weight (%) |

|---|---|---|

| Toyota Motor Credit Corp | Consumer cyclical | 1.74% |

| Volkswagen Group America | Consumer cyclical | 1.74% |

| Daimler Finance NA LLC | Consumer cyclical | 1.72% |

| AT&T Inc | Communications | 1.60% |

| Apple Inc | Technology | 1.60% |

| Verizon Communications | Communications | 1.60% |

| General Electric | Capital goods | 1.48% |

| Ford Motor Credit Co LLC | Consumer cyclical | 1.34% |

| Comcast Corp | Communications | 1.32% |

| BMW US Capital LLC | Consumer cyclical | 1.25% |

Source: Investopedia

This program is intended to support the flow of credit, but its announcement in June also gave stock markets a boost in confidence. With the Fed directly supporting corporations, shareholders are being shielded from risks related to declining sales and bankruptcy.

By the end of June, the SMCCF had purchased $429 million in corporate bonds.

ETF Purchase Program

The SMCCF is also authorized to purchase corporate bond ETFs, a historic first for the Fed. The facility’s five largest ETF purchases as of June 18, 2020, are detailed below:

| ETF Name | Purchase size ($) | ETF Description |

|---|---|---|

| iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD) | $1.7 billion | Tracks an index composed of USD-denominated, investment grade corporate bonds. |

| Vanguard Short-Term Corporate Bond ETF (VCSH) | $1.3 billion | Invests primarily in investment grade corporate bonds, maintaining an average maturity of 1 to 5 years. |

| Vanguard Intermediate-Term Corporate Bond ETF (VCIT) | $1.0 billion | Invests primarily in investment grade corporate bonds, maintaining an average maturity of 5 to 10 years. |

| iShares Short-Term Corporate Bond ETF (IGSB) | $608 million | Tracks an index composed of USD-denominated investment-grade corporate bonds with maturities between 1 and 5 years. |

| SPDR Barclays High Yield Bond ETF (JNK) | $412 million | Seeks to provide a diversified exposure to USD-denominated high yield corporate bonds. |

Source: Investopedia

Although the SMCCF’s purchase of ETFs outsize those of corporate bonds, the Fed has signaled its intention to make direct bond purchases its primary focus going forward.

Will Markets and Consumers Reconnect Anytime Soon?

It’s hard to see the S&P 500 moving towards a more balanced sector composition in the near future. America’s big tech stocks have been resilient during the pandemic, with some even reaching new highs.

The Fed also remains committed to providing corporations with credit, thereby enabling them to “borrow” their way out of the pandemic. These commitments have propped up stock markets by reducing bankruptcy risk and potentially speeding up the economic recovery.

Consumer sentiment, on the other hand, has yet to show signs of recovery. Surveys released in early July may shed some light on why—63% of Americans believe it will take a year or more for the economy to fully recover, while 82% are hoping for an extension of COVID-19 relief programs.

With both sides moving in opposite directions, it’s possible the disconnect could grow even larger before it starts to shrink.

Markets

Ranked: The Largest U.S. Corporations by Number of Employees

We visualized the top U.S. companies by employees, revealing the massive scale of retailers like Walmart, Target, and Home Depot.

The Largest U.S. Corporations by Number of Employees

This was originally posted on our Voronoi app. Download the app for free on Apple or Android and discover incredible data-driven charts from a variety of trusted sources.

Revenue and profit are common measures for measuring the size of a business, but what about employee headcount?

To see how big companies have become from a human perspective, we’ve visualized the top U.S. companies by employees. These figures come from companiesmarketcap.com, and were accessed in March 2024. Note that this ranking includes publicly-traded companies only.

Data and Highlights

The data we used to create this list of largest U.S. corporations by number of employees can be found in the table below.

| Company | Sector | Number of Employees |

|---|---|---|

| Walmart | Consumer Staples | 2,100,000 |

| Amazon | Consumer Discretionary | 1,500,000 |

| UPS | Industrials | 500,000 |

| Home Depot | Consumer Discretionary | 470,000 |

| Concentrix | Information Technology | 440,000 |

| Target | Consumer Staples | 440,000 |

| Kroger | Consumer Staples | 430,000 |

| UnitedHealth | Health Care | 400,000 |

| Berkshire Hathaway | Financials | 383,000 |

| Starbucks | Consumer Discretionary | 381,000 |

| Marriott International | Consumer Discretionary | 377,000 |

| Cognizant | Information Technology | 346,600 |

Retail and Logistics Top the List

Companies like Walmart, Target, and Kroger have a massive headcount due to having many locations spread across the country, which require everything from cashiers to IT professionals.

Moving goods around the world is also highly labor intensive, explaining why UPS has half a million employees globally.

Below the Radar?

Two companies that rank among the largest U.S. corporations by employees which may be less familiar to the public include Concentrix and Cognizant. Both of these companies are B2B brands, meaning they primarily work with other companies rather than consumers. This contrasts with brands like Amazon or Home Depot, which are much more visible among average consumers.

A Note on Berkshire Hathaway

Warren Buffett’s company doesn’t directly employ 383,000 people. This headcount actually includes the employees of the firm’s many subsidiaries, such as GEICO (insurance), Dairy Queen (retail), and Duracell (batteries).

If you’re curious to see how Buffett’s empire has grown over the years, check out this animated graphic that visualizes the growth of Berkshire Hathaway’s portfolio from 1994 to 2022.

-

Business2 weeks ago

Business2 weeks agoAmerica’s Top Companies by Revenue (1994 vs. 2023)

-

Environment1 week ago

Environment1 week agoRanked: Top Countries by Total Forest Loss Since 2001

-

Markets1 week ago

Markets1 week agoVisualizing America’s Shortage of Affordable Homes

-

Maps2 weeks ago

Maps2 weeks agoMapped: Average Wages Across Europe

-

Mining2 weeks ago

Mining2 weeks agoCharted: The Value Gap Between the Gold Price and Gold Miners

-

Demographics2 weeks ago

Demographics2 weeks agoVisualizing the Size of the Global Senior Population

-

Misc2 weeks ago

Misc2 weeks agoTesla Is Once Again the World’s Best-Selling EV Company

-

Technology2 weeks ago

Technology2 weeks agoRanked: The Most Popular Smartphone Brands in the U.S.