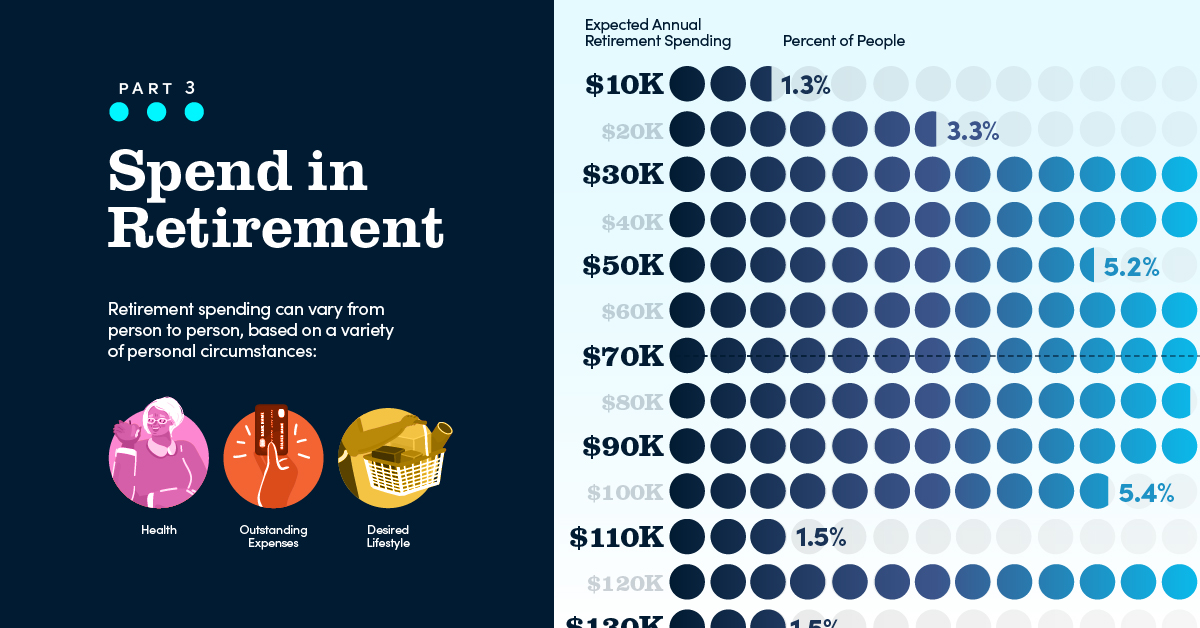

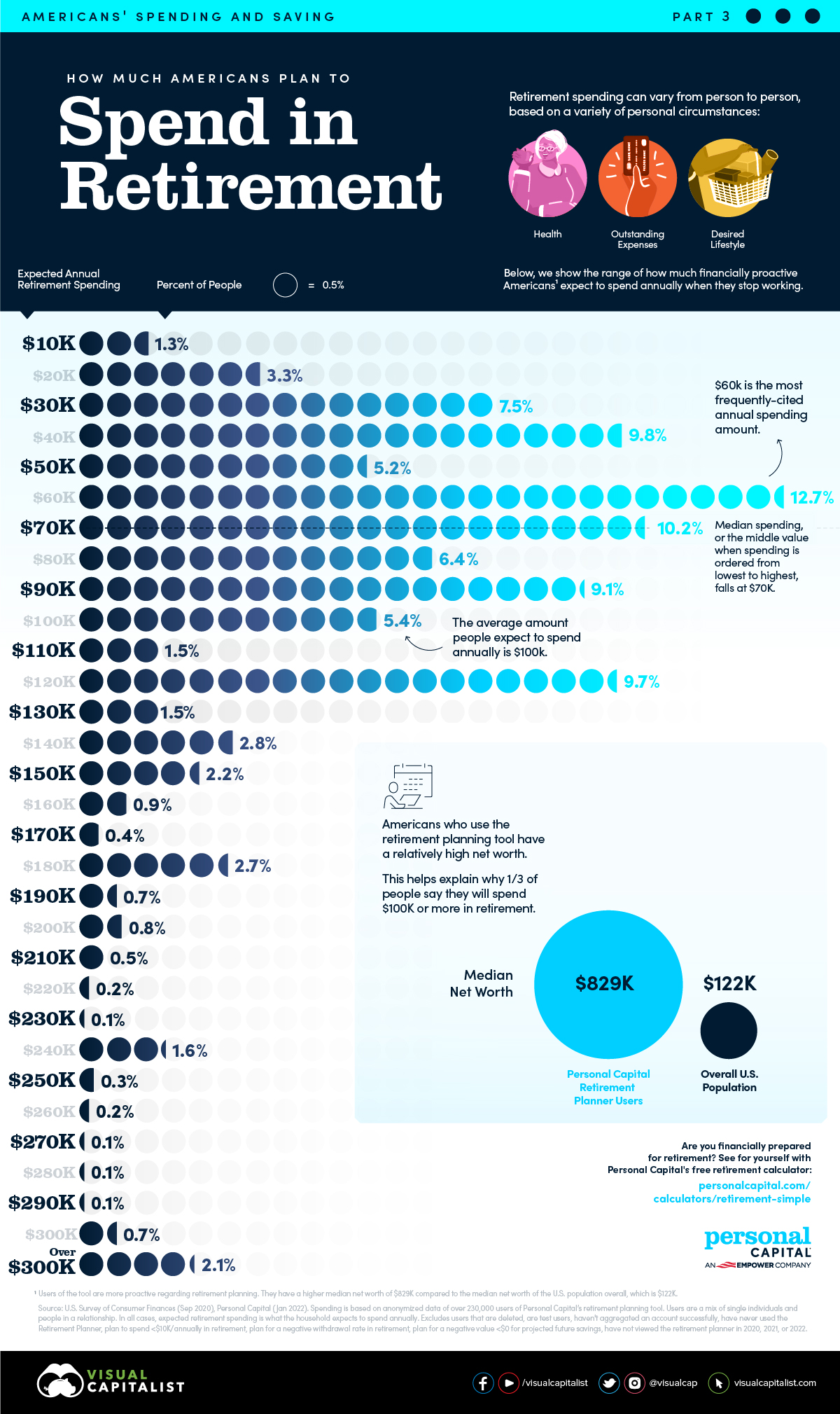

Retirement Spending: How Much Do Americans Plan to Spend Annually?

Americans’ Expected Annual Retirement Spending

Planning for retirement can be a daunting task. How much money will you need? What will your retirement spending look like?

It varies from person to person, based on factors like your health, outstanding expenses, and desired lifestyle. One helpful trick is to break it down into how much you estimate you’ll spend each year.

In this graphic from Personal Capital, we show the expected annual retirement spending of Americans. It’s the last in a three-part series that explores Americans’ spending and savings.

The Range of Retirement Spending

To determine how much people expect to spend, we used anonymized data from users of Personal Capital’s retirement planning tool. It’s worth noting that these users are proactive regarding financial planning. They also have a median net worth of $829,000 compared to the $122,000 median net worth of the U.S. population overall.

Here is the range of expected annual retirement spending.

| Expected Annual Retirement Spending | Percent of People |

|---|---|

| $10K | 1.3% |

| $20K | 3.3% |

| $30K | 7.5% |

| $40K | 9.8% |

| $50K | 5.2% |

| $60K | 12.7% |

| $70K | 10.2% |

| $80K | 6.4% |

| $90K | 9.1% |

| $100K | 5.4% |

| $110K | 1.5% |

| $120K | 9.7% |

| $130K | 1.5% |

| $140K | 2.8% |

| $150K | 2.2% |

| $160K | 0.9% |

| $170K | 0.4% |

| $180K | 2.7% |

| $190K | 0.7% |

| $200K | 0.8% |

| $210K | 0.5% |

| $220K | 0.2% |

| $230K | 0.1% |

| $240K | 1.6% |

| $250K | 0.3% |

| $260K | 0.2% |

| $270K | 0.1% |

| $280K | 0.1% |

| $290K | 0.1% |

| $300K | 0.7% |

| Over $300K | 2.1% |

Users are a mix of single individuals and people in a relationship. In all cases, expected retirement spending is what the household expects to spend annually.

The most commonly-cited expected spending amount is $60,000. Interestingly, this is roughly in line with what Americans spend annually on their credit cards. This suggests that people may be using their current bills to help gauge their future retirement spending.

Median spending, or the middle value when spending is ordered from lowest to highest, falls at $70,000. However, average spending is a fair amount higher at $100,000. This is because the average is calculated by adding up all the expected retirement spending amounts and dividing by the total number of users. Higher expected spending amounts, some in excess of $300,000 per year, skew the average calculation upwards.

Of course, given their higher net worth, it’s perhaps not surprising that many Personal Capital users expect to spend larger amounts in retirement. How does this compare to the general population? According to the Bureau of Labor Statistics, Americans age 65 and older spend about $48,000 per year on average.

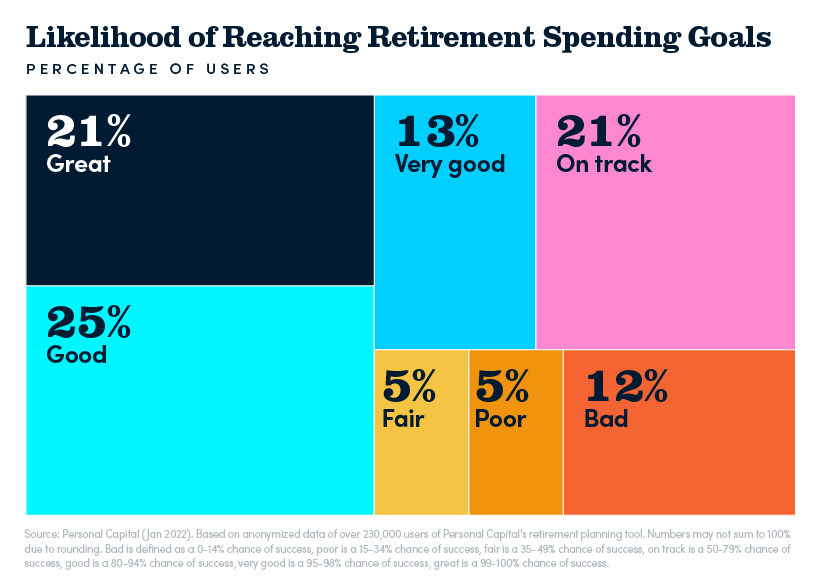

Chances of Retirement Success

Once you’ve determined how much you’ll spend in retirement, your next step may be to wonder if your savings are on track. Based on an assessment of Personal Capital retirement planner users, here is the breakdown of people’s chance of success.

The good news: more than half of people have an 80% or better chance of meeting their retirement spending goals. This means they have sufficient financial assets and are contributing enough, regularly enough, to meet their expected spending amount. The not so good news: one in five people has a less than 50% chance of meeting their goals.

This problem is even more troublesome in the overall U.S. population. Only 50% of people have a retirement account, and the Center for Retirement Research at Boston College estimates half of today’s workers are unprepared for retirement.

Setting Your Own Retirement Spending Goals

While seeing the goals of others is a starting point, your annual retirement spending will be very specific to you. Not sure where to start?

Financial planners typically recommend that you should plan on needing 70-80% of your pre-retirement income in retirement. This is because people generally no longer have certain expenses, such as commuting or childcare costs, when they retire. However, keep in mind your expenses could be higher if you still have a mortgage, encounter unforeseen medical expenses, or want to splurge on things like travel when you retire.

It requires some upfront planning, but being realistic about your retirement spending can give you confidence in your financial future.

-

Sponsored3 years ago

Sponsored3 years agoMore Than Precious: Silver’s Role in the New Energy Era (Part 3 of 3)

Long known as a precious metal, silver in solar and EV technologies will redefine its role and importance to a greener economy.

-

Sponsored7 years ago

Sponsored7 years agoThe History and Evolution of the Video Games Market

Everything from Pong to the rise of mobile gaming and AR/VR. Learn about the $100 billion video games market in this giant infographic.

-

Sponsored8 years ago

Sponsored8 years agoThe Extraordinary Raw Materials in an iPhone 6s

Over 700 million iPhones have now been sold, but the iPhone would not exist if it were not for the raw materials that make the technology…

-

Sponsored8 years ago

Sponsored8 years agoThe Industrial Internet, and How It’s Revolutionizing Mining

The convergence of the global industrial sector with big data and the internet of things, or the Industrial Internet, will revolutionize how mining works.