Visualized: The EV Mineral Shortage

How Mineral Supply Will Change EV Forecasts

Did you know that EVs need up to six times more minerals than conventional cars?

EVs are mineral-intensive and are pushing up demand for critical battery metals. According to the International Energy Agency (IEA), lithium, nickel, and cobalt demand is expected to grow from 10%-20% to over 80% by 2030.

As countries around the world pledge to go all-electric by 2035 and 2040, do we have enough mineral supply for EV demand?

Factors such as geopolitical concentration of resources, quality of materials, mining industry lead times, and environmental factors will together determine whether we have the minerals we need.

Let’s take a look at how critical minerals are affected.

| Mineral | Constraints |

|---|---|

| Copper | Copper mines currently in operation are nearing their peak, suffering from reserve exhaustion, while ore quality in older mines is declining. South American and Australian mines are located in areas where water availability can be scarce. This could cause setbacks given the high water requirements needed for the mining process. |

| Nickel | There are a number of growing concerns related to higher CO2 emissions and waste disposal. Nickel quality needs to be high (Class 1) for EV batteries. Most nickel in the global supply chain is unusable for EVs. |

| Cobalt | The Democratic Republic of Congo and China account for around 70% of production. 90% of cobalt produced is a by-product of nickel and copper, making new supply subject to the development of these mines. |

| Rare Earth Elements | Concerns surrounding negative environmental credentials in processing operations. The value chain from mining to processing and magnet production is geographically concentrated in China. |

| Lithium | The world could face severe lithium shortages as early as 2025. Lithium mines that started operations between 2010-2019 took an average of 16.5 years to develop. China accounts for 60% of global production and more than 80% of lithium hydroxide. Over 50% of lithium mines are located in areas that suffer water shortages. This could cause setbacks, given the high water requirements for mining processes. |

Recycling is a partial solution to alleviate critical mineral supply but will fall short of meeting the high levels of demand until around the 2030s.

The EV Supply Chain

Currently, the resources for EV batteries are concentrated in very few countries. This concentration is an increasing concern for supply chain distribution.

China is home to more than half of the world’s lithium, cobalt, and graphite processing and refining capacity, as well as three-quarters of all lithium-ion battery production capacity.

Europe accounts for more than one-quarter of worldwide EV assembly, but home to very little of the supply chain, with the region’s cobalt processing share accounting for 20% of the mix.

Meanwhile, both Korea and Japan control a sizable portion of the downstream supply chain after raw material processing. Korea accounts for 15% of worldwide cathode material production capacity. Japan produces 14% of cathode and 11% of anode material.

The United States accounts for just 10% of EV production and 7% of battery production capacity.

Suggested Solutions

To reduce setbacks surrounding resource demand, KGP Auto’s new report recommends that material supply is accessed and matched to a broader fuel energy mix.

In this scenario, platinum group metals (PGMs) continue to play a leading role in the auto industry by assisting in building cleaner emission vehicles.

These vehicles support more sustainable fuels such as hydrogen, filling the gaps to net-zero targets by allowing EVs to catch up with material supply

>> Read KGP Auto’s Powertrain Outlook Report to learn more.

-

Mining2 days ago

Mining2 days agoGold vs. S&P 500: Which Has Grown More Over Five Years?

The price of gold has set record highs in 2024, but how has this precious metal performed relative to the S&P 500?

-

Mining2 weeks ago

Mining2 weeks agoCharted: The Value Gap Between the Gold Price and Gold Miners

While the price of gold has reached new record highs in 2024, gold mining stocks are still far from their 2011 peaks.

-

Uranium2 months ago

Uranium2 months agoCharted: Global Uranium Reserves, by Country

We visualize the distribution of the world’s uranium reserves by country, with 3 countries accounting for more than half of total reserves.

-

Markets3 months ago

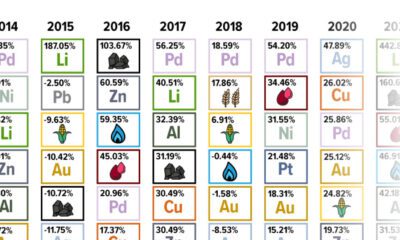

Markets3 months agoThe Periodic Table of Commodity Returns (2014-2023)

Commodity returns in 2023 took a hit. This graphic shows the performance of commodities like gold, oil, nickel, and corn over the last decade.

-

Strategic Metals3 months ago

Strategic Metals3 months agoChina Dominates the Supply of U.S. Critical Minerals List

The U.S. Geological Survey estimates that in 2022, China was the world’s leading producer of 30 out of 50 entries on the U.S. critical minerals list.

-

Mining5 months ago

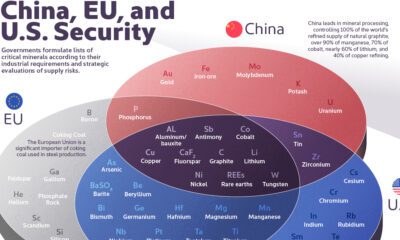

Mining5 months agoThe Critical Minerals to China, EU, and U.S. National Security

Ten materials, including cobalt, lithium, graphite, and rare earths, are deemed critical by all three.