5 Tax Tips for Investors

5 Tax Tips for Investors

Are your investments tax efficient? If you’re not sure, you’re not alone.

- 82% of Americans are bothered by the complexity of the tax system

- 66% of Americans are frustrated by the amount they pay in taxes

In this graphic from New York Life Investments, we look at five practical tax tips you can consider for your own investments.

Tip #1: Use a Tax-Advantaged Account

Using a tax-advantaged account can maximize the growth of your investments. This is because you aren’t paying out a portion of your earnings in taxes each year, so your earnings are fully reinvested.

Consider how this affects the value of a hypothetical portfolio over time, assuming $10,000 annual contributions, an 8.4% annual return, and a 20.9% tax rate applied to the taxable account.

| Year | 401(k) | Taxable Account |

|---|---|---|

| 1 | $10,840 | $10,660 |

| 5 | $64,103 | $60,815 |

| 10 | $160,049 | $144,530 |

| 15 | $303,655 | $259,765 |

| 20 | $518,595 | $418,391 |

| 25 | $840,306 | $636,743 |

| 30 | $1,312,822 | $937,312 |

While the difference is minimal in the beginning, the balance of the tax-advantaged 401(k) is 41% larger after 30 years.

Tip #2: Use the Right Tax-Advantaged Account

Among tax-advantaged accounts, there are traditional and Roth options.

| Traditional | Roth | |

|---|---|---|

| Contribution | Pre-Tax Dollars | After-Tax Dollars |

| Withdrawals After Age 59 ½ | Taxable | Tax-Free |

If you’re strategic about which account type you choose, you can lower the amount of tax you pay. Consider a young person early in their career who expects that their marginal tax rate will increase by the time they retire:

- Current Marginal Tax Rate: 17.9%

- Expected Marginal Tax Rate in Retirement: 27.9%

With a traditional account, they will pay the higher expected tax rate of 27.9% on withdrawals in retirement. With a Roth account, they will pay their lower marginal tax rate of 17.9% on contributions they make now.

While there are other factors to consider, the timing of tax benefits can be a key difference when you are choosing between tax-advantaged accounts.

Tip #3: Harvest Tax Losses

Taxable accounts, which can be helpful for investors looking for flexibility, offer the benefit of tax loss harvesting. If you sell an investment at a loss, you can use it to offset gains that you would otherwise owe taxes on.

Consider an investor with the following:

- $25,000 short-term capital gain

- $10,000 short-term capital loss

- 27.9% marginal tax rate

How will their tax bill differ based on whether or not they harvest the loss?

| Option 1: Not Harvesting Losses | Option 2: Harvesting Losses | |

|---|---|---|

| Short-Term Capital Gain | $25,000 | $25,000 |

| Short-Term Capital Loss Offset | - | ($10,000) |

| Net Short-Term Capital Gain | $25,000 | $15,000 |

| Taxes Owed | $6,975 | $4,185 |

By harvesting the loss, the investor has reduced their taxes by nearly $3,000.

Tip #4: Donate Appreciated Assets Rather Than Cash

If charitable donations are part of your money goals, you could be leaving tax savings on the table if you’re donating cash.

Consider an investor who has stock worth $5,000 that they originally purchased for $3,000. They have held the stock for over a year and have a 20.9% marginal tax rate on long-term capital gains.

| Option 1: Sell Shares and Donate the Cash | Option 2: Transfer Shares Directly to Charity | |

|---|---|---|

| Sale of Shares | $5,000 | - |

| Capital Gain | $2,000 | - |

| Taxes Owed | $418 | - |

| Net Donation | $4,582 | $5,000 |

By donating the shares directly, the investor does not have to pay capital gains taxes and can donate a higher amount. Another benefit? Investors are generally able to deduct the full fair market value of the donation on their taxes.

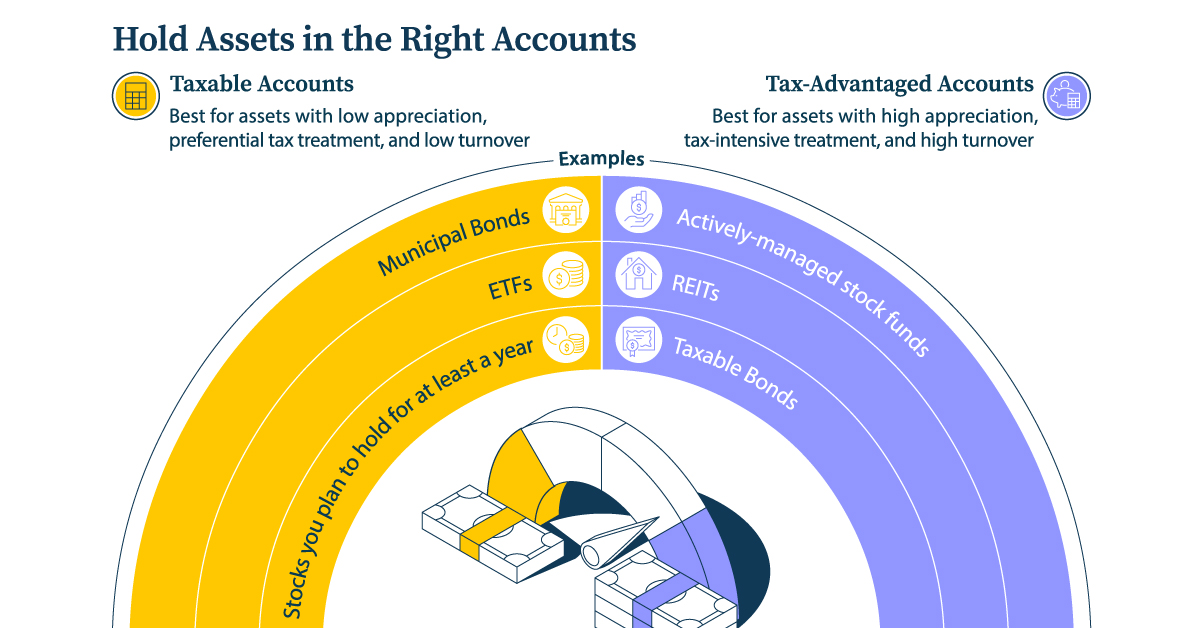

Tip #5: Hold Assets in the Right Accounts

Some investors may use whichever account is the most convenient and hold the same assets across their accounts. However, it’s more tax efficient to put certain assets in certain accounts based on their tax treatment.

- Taxable Accounts: Best for assets with low appreciation, preferential tax treatment, and low turnover. Assets that may be a good fit are municipal bonds, ETFs, and stocks you plan to hold for at least a year.

- Tax-Advantaged Accounts: Best for assets with high appreciation, tax-intensive treatment, and high turnover. Assets that may be a good fit are actively-managed stock funds, real estate investment trusts, and taxable bonds.

Taking a holistic view of your assets can help you make more strategic and informed decisions about where to put them.

Investing With Tax Tips in Mind

Through some advanced planning, you can consider these five tax tips and make your investments more tax efficient.

Learn more about tax efficient investing strategies with New York Life Investments.

-

Investor Education5 months ago

Investor Education5 months agoThe 20 Most Common Investing Mistakes, in One Chart

Here are the most common investing mistakes to avoid, from emotionally-driven investing to paying too much in fees.

-

Stocks10 months ago

Stocks10 months agoVisualizing BlackRock’s Top Equity Holdings

BlackRock is the world’s largest asset manager, with over $9 trillion in holdings. Here are the company’s top equity holdings.

-

Investor Education10 months ago

Investor Education10 months ago10-Year Annualized Forecasts for Major Asset Classes

This infographic visualizes 10-year annualized forecasts for both equities and fixed income using data from Vanguard.

-

Investor Education1 year ago

Investor Education1 year agoVisualizing 90 Years of Stock and Bond Portfolio Performance

How have investment returns for different portfolio allocations of stocks and bonds compared over the last 90 years?

-

Debt2 years ago

Debt2 years agoCountries with the Highest Default Risk in 2022

In this infographic, we examine new data that ranks the top 25 countries by their default risk.

-

Markets2 years ago

Markets2 years agoThe Best Months for Stock Market Gains

This infographic analyzes over 30 years of stock market performance to identify the best and worst months for gains.