Visual Capitalist

Here’s What’s New on VC+ in January 2020

If you’re a regular visitor to Visual Capitalist, you know that we’re your home base for data-driven, beautiful visuals that help explain a complex world.

But did you know there’s a way to get an even more out of Visual Capitalist, all while helping support the work we do?

New to VC+ in January 2020

VC+ is our newly launched members program that gives you exclusive access to extra visual content and insightful special features. It also gets you access to The Trendline, our new members-only graphic newsletter.

So, what is getting sent to VC+ members in the coming days?

“Commodities: Explained Through Powerful Visuals”

SPECIAL DISPATCH: 9 Techniques We Use to Make Commodity Markets Easier to Understand

No two commodities are alike, and each has different market dynamics.

Luckily, visuals such as charts, infographics, and data visualizations can help us approach commodities in a way that helps to improve your understanding of how things fit together.

Whether it’s explaining the special “safe haven” status ascribed to gold or a flow diagram of how energy sources are used, this VC+ feature will dive into the innovative techniques we’ve successfully used to approach topics on energy, metals, and agriculture.

Publishing date: Jan 17 (Get VC+ to access)

“Investing 101: Breaking Down the Basics for Beginners”

SPECIAL DISPATCH: Summing up our best infographic recommendations for new investors

Investing can be a daunting subject for newbies. Luckily, visuals have a powerful way of cutting through the complexity.

From defining industry terms to visualizing volatility in the market, this VC+ special feature will round up our favorite data-driven graphics to help new investors get started.

Publishing date: Jan 23 (Get VC+ to access)

The Trendline

PREMIUM NEWSLETTER: Our weekly members-only newsletter for VC+ members

Every week, VC+ members also get our premium graphic newsletter, The Trendline.

With The Trendline, we’ll send you the best visual content, datasets, and insightful reports relating to business that our editors find each week.

Publishing Date: Every Sunday

More Visuals. More Insight. More Understanding.

Get access to these upcoming features by becoming a VC+ member.

For a limited time, get 25% off, which makes your VC+ membership the same price as a coffee each month:

PS – We look forward to sending you even more great visuals and data!

Best of

Best Visualizations of March on the Voronoi App

We round up the most popular, most discussed, and most liked visualizations of the month on Voronoi, our new data storytelling platform.

At the end of 2023, we publicly launched Voronoi, our free new data discovery app!

The initial response from both users and creators has been incredible. We now have millions of in-app views, and there are already more than 700 interesting visualizations to discover, many of which will never be published on Visual Capitalist.

For that reason, we’ve chosen to highlight some of the most popular visualizations and creators from March in this roundup. To see them and many others, make sure to download the app!

Let’s take a look at a popular creator worth highlighting, as well as the most viewed, most discussed, and most liked posts of the month.

POPULAR CREATOR

Ehsan Soltani

Visual Capitalist isn’t the only creator on the Voronoi app.

Instead, it features incredible data-driven charts and stories from many of the world’s best creators, like Ehsan Soltani.

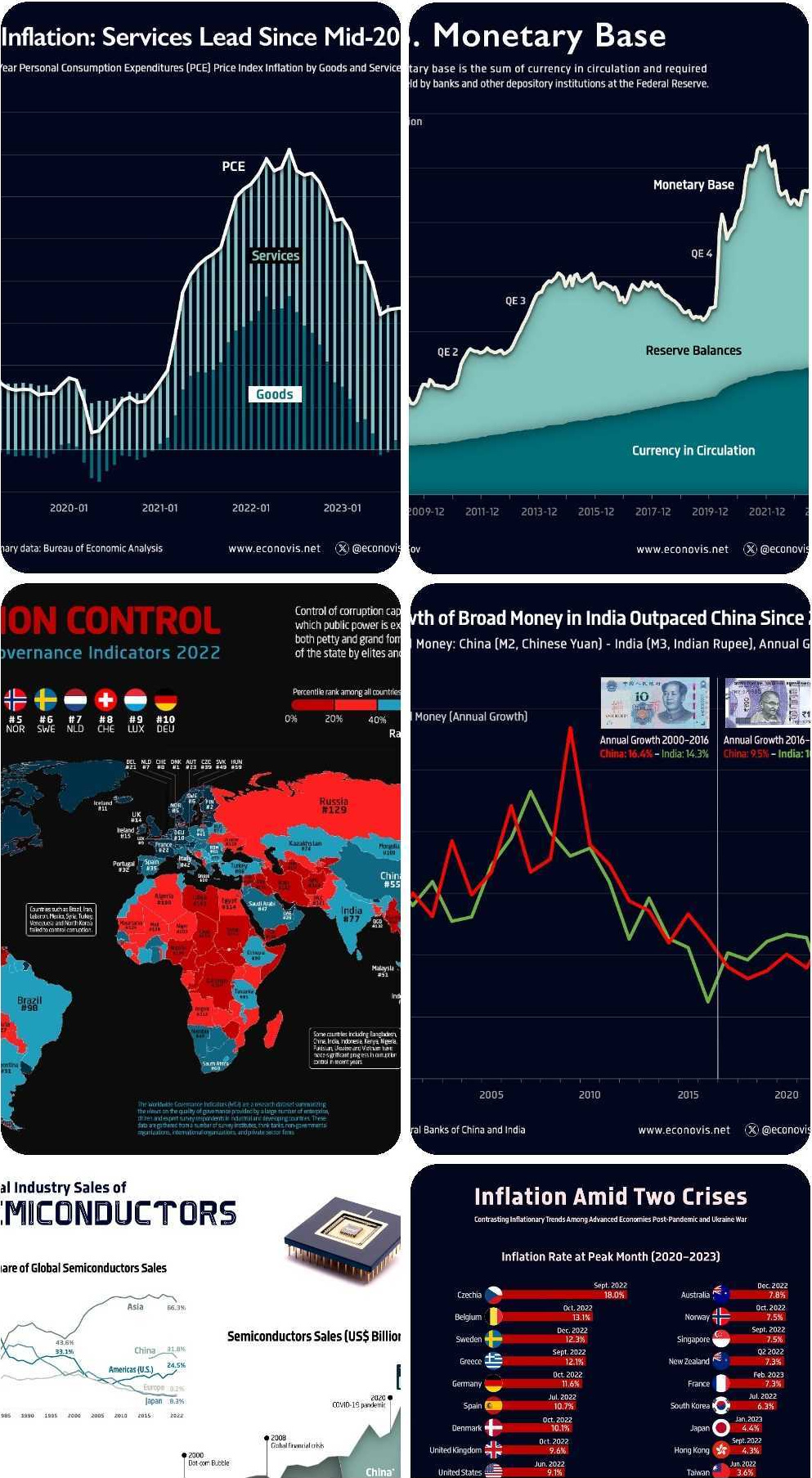

Ehsan is an economist, and one of the most prolific creators on Voronoi so far. He’s published 41 visualizations on wide-ranging subjects such as:

- The world’s biggest “money printer” economies

- Global commodity returns

- Corruption by country

- Inflation rates in advanced economies

For those interested in what’s happening with the global economy, Ehsan Soltani is definitely worth a follow!

![]() View all of Ehsan’s visuals on Voronoi today.

View all of Ehsan’s visuals on Voronoi today.

MOST VIEWED

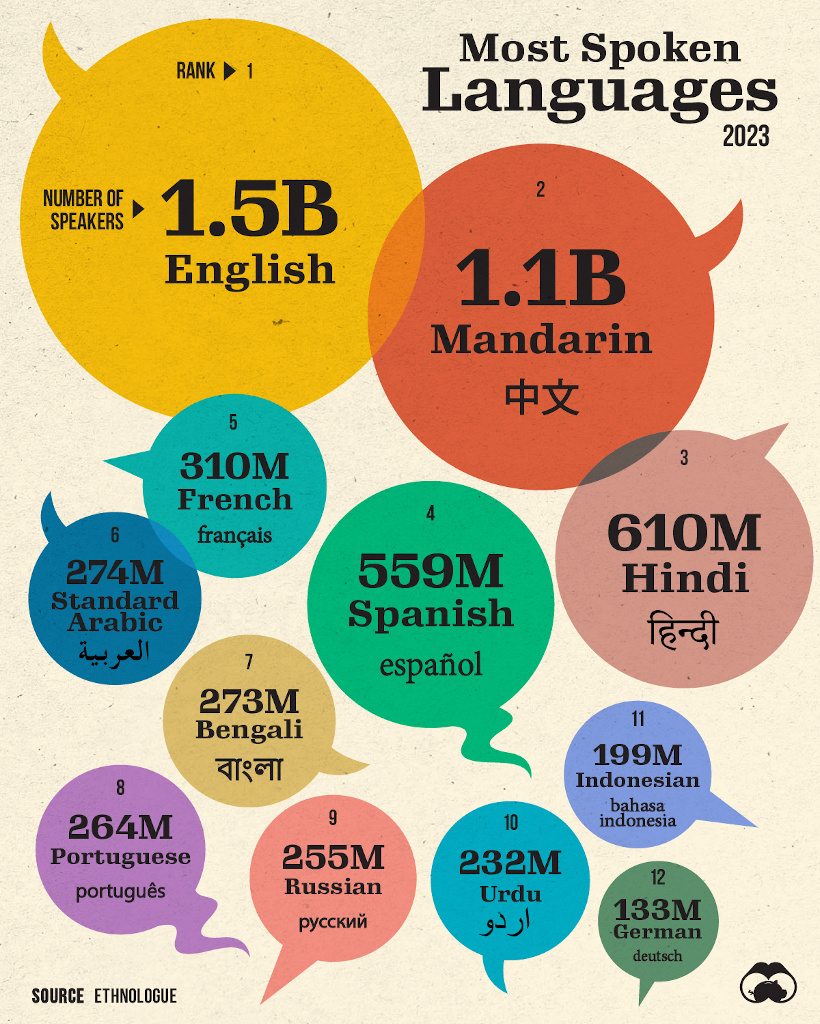

The 12 Most Spoken Languages in 2023

Which languages are most commonly spoken around the world by native speakers?

This visualization from Visual Capitalist was one of the most viewed by users, and it highlights the top languages spoken around the world.

Data here comes from the Ethnologue database, the most rigorous and comprehensive language database globally. It’s worth noting that it highlights languages spoken by native speakers only, so second languages are not counted here.

![]() Get the data behind this visual on Voronoi today.

Get the data behind this visual on Voronoi today.

MOST DISCUSSED

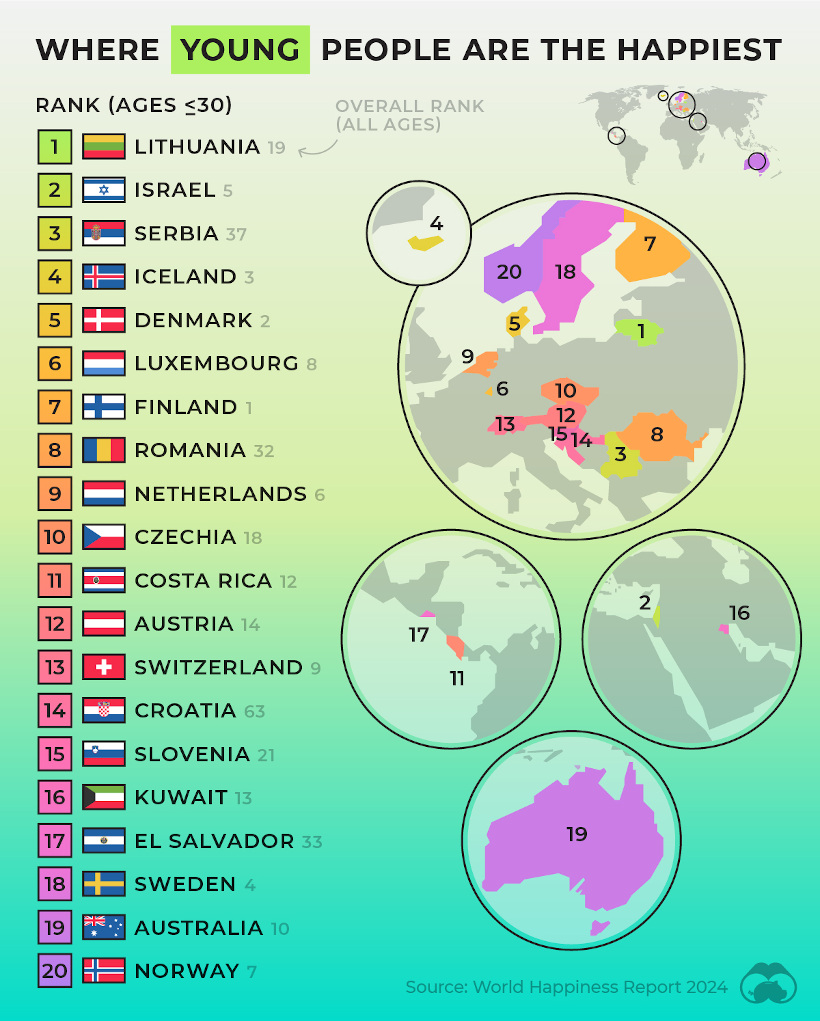

Where Young People are Happiest

The most commented on visualization from Visual Capitalist showed the countries with the happiest young people (under 30 years old).

This comes from the World Happiness Report, which Visual Capitalist covers extensively every year.

In this year’s edition, one particularly interesting feature focused on happiness discrepancies between age groups. For example, in some countries, younger people were much happier than the average population—in others, older populations were far happier.

![]() To join the conversation, download Voronoi today.

To join the conversation, download Voronoi today.

MOST LIKED

The Fastest Growing Brands in the U.S.

The most liked visual on Voronoi in March came from Visual Capitalist, showing the brands that are growing the fastest in the United States.

The data here comes from Morning Consult, and shows the share of customers that were considering purchasing a brand in October 1-24, 2023, and subtracted the share of those who said the same between Jan 1-31, 2023.

![]() Get the data behind this visual on Voronoi today.

Get the data behind this visual on Voronoi today.

-

Real Estate2 weeks ago

Real Estate2 weeks agoVisualizing America’s Shortage of Affordable Homes

-

Technology1 week ago

Technology1 week agoRanked: Semiconductor Companies by Industry Revenue Share

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

Real Estate2 weeks ago

Real Estate2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Business2 weeks ago

Business2 weeks agoCharted: Big Four Market Share by S&P 500 Audits

-

AI2 weeks ago

AI2 weeks agoThe Stock Performance of U.S. Chipmakers So Far in 2024

-

Misc2 weeks ago

Misc2 weeks agoAlmost Every EV Stock is Down After Q1 2024

-

Money2 weeks ago

Money2 weeks agoWhere Does One U.S. Tax Dollar Go?