Agriculture

Canada’s Medical Cannabis Report Card: Spring 2015

Canada’s Medical Cannabis Report Card: Spring 2015

Just over a year ago, we released an infographic that introduced the new MMPR (Marihuana for Medical Purposes Regulations) introduced in Canada as well as the case for medical cannabis.

With the first full year of MMPR now behind us, we wanted to take a look at how the medical cannabis industry has matured. For two weeks of April, we talked to every practicing LP (Licensed Producer) in Canada to get a sense of the current landscape of the medical cannabis market.

We wanted to see how the market has changed as well as the type of experience that prospective patients could expect. Then, our team put this information together with some industry context. In the infographic and report, we include a timeline highlighting the last year of events affecting the medical marijuana space in Canada, and also a section focusing on the cultural shift towards acceptance of cannabis.

Methodology

The purpose of this report is to serve as a snapshot of what a potential patient may experience while contacting and researching different LPs.

This report is meant to be representative of the time of the two weeks of research (mid-April) and not today. Things change fast and it is possible that producers have come out with new strains (or run out of strains) since that time period.

Further, we measured things like social media, phone, and email response times with only a small sample size. These are not statistically significant measures, but are again indicative of what our experience was in trying to reach producers with questions.

Lastly, it is also worth noting that at the end of April, we reached out to every LP with the opportunity to correct information that we had collected. Most producers wrote us back and provided some corrections or affirmation that the information was correct, but a few did not respond.

Conclusions

TRADEOFFS

The market is still in its early stages, and companies are executing different strategies to win over patients. Right now, there are brands ranging from low to high end in terms of pricing and quality. There are also a variety of preparation strategies, including but not limited to: selling only whole buds, pre-milling the product, machine-trimming, or irradiating the product. In the future, as the market matures, it will be clearer which of these strategies work best for patients and which are better suited for smaller niches.

Moving forward, it will also be interesting to watch if all LPs move towards creating a similar selection of products with comparable benefits, or if they all specialize in specific areas based on patient demand.

STRAIN AVAILABILITY

The single biggest trend we noticed was a lack of consistent strain availability. While the LPs have made big progress since last autumn, there is still a wide variability in what is available at any given time.

Supply hiccups are expected in a new industry, but we did get the impression that it does impact patients significantly. We hope that as medical cannabis in Canada matures, that patients will be able to rely on consistent supply for the medicine that works best for them.

TRANSPARENCY

Our last note is on transparency. We found several LPs very reluctant to give out information on their company or their medicine. This is a concern for patients that are interested in knowing more about what they are buying.

A possible cause of this could also be that some representatives for each company may not yet have enough industry experience to know answers to questions like whether their product is irradiated, or if their flowers are trimmed by machines or by hand.

The good news is that companies seem to be rapidly maturing in their approach to knowledge and customer service. We had done some preliminary calls and research in the autumn of 2014, and many less-established LPs were much more reluctant to give us information at that time. Further, some representatives were not knowledgeable about product traits and were unprofessional with their phone and email responses.

While we still received some of these types of responses in our most recent rounds, we saw a noticeable decrease as company representatives acted more professional, courteous, and with genuine knowledge of their product and the industry. Companies also responded much faster to us in April than they did in 2014, which means that they are improving from a customer service standpoint.

Edits: We updated this on June 4, 2015 at 12:58pm, updating the total amount of listed LPs by Health Canada to 19.

Markets

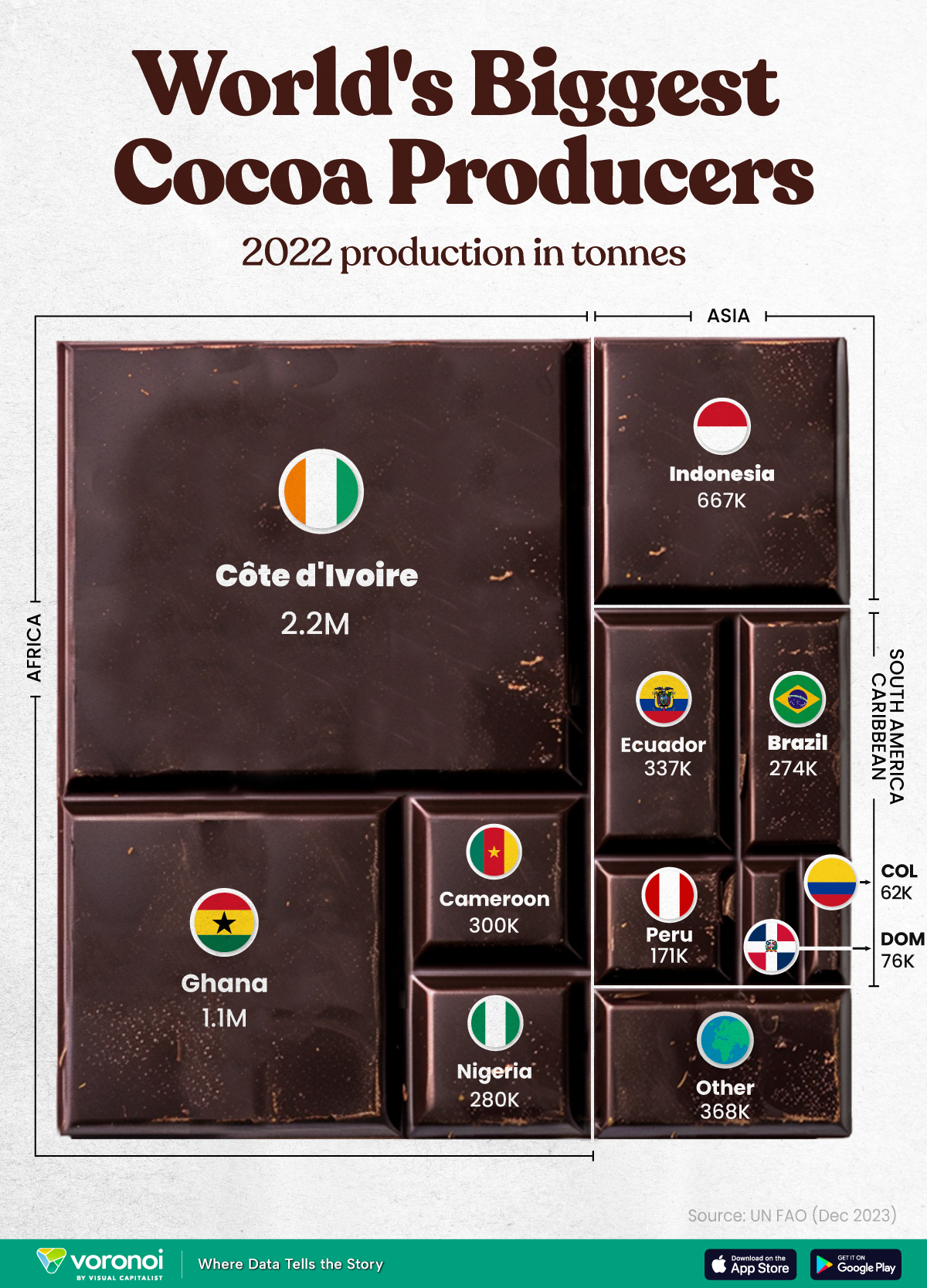

The World’s Top Cocoa Producing Countries

Here are the largest cocoa producing countries globally—from Côte d’Ivoire to Brazil—as cocoa prices hit record highs.

The World’s Top Cocoa Producing Countries

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

West Africa is home to the largest cocoa producing countries worldwide, with 3.9 million tonnes of production in 2022.

In fact, there are about one million farmers in Côte d’Ivoire supplying cocoa to key customers such as Nestlé, Mars, and Hershey. But the massive influence of this industry has led to significant forest loss to plant cocoa trees.

This graphic shows the leading producers of cocoa, based on data from the UN FAO.

Global Hotspots for Cocoa Production

Below, we break down the top cocoa producing countries as of 2022:

| Country | 2022 Production, Tonnes |

|---|---|

| 🇨🇮 Côte d'Ivoire | 2.2M |

| 🇬🇭 Ghana | 1.1M |

| 🇮🇩 Indonesia | 667K |

| 🇪🇨 Ecuador | 337K |

| 🇨🇲 Cameroon | 300K |

| 🇳🇬 Nigeria | 280K |

| 🇧🇷 Brazil | 274K |

| 🇵🇪 Peru | 171K |

| 🇩🇴 Dominican Republic | 76K |

| 🌍 Other | 386K |

With 2.2 million tonnes of cocoa in 2022, Côte d’Ivoire is the world’s largest producer, accounting for a third of the global total.

For many reasons, the cocoa trade in Côte d’Ivoire and Western Africa has been controversial. Often, farmers make about 5% of the retail price of a chocolate bar, and earn $1.20 each day. Adding to this, roughly a third of cocoa farms operate on forests that are meant to be protected.

As the third largest producer, Indonesia produced 667,000 tonnes of cocoa with the U.S., Malaysia, and Singapore as major importers. Overall, small-scale farmers produce 95% of cocoa in the country, but face several challenges such as low pay and unwanted impacts from climate change. Alongside aging trees in the country, these setbacks have led productivity to decline.

In South America, major producers include Ecuador and Brazil. In the early 1900s, Ecuador was the world’s largest cocoa producing country, however shifts in the global marketplace and crop disease led its position to fall. Today, the country is most known for its high-grade single-origin chocolate, with farms seen across the Amazon rainforest.

Altogether, global cocoa production reached 6.5 million tonnes, supported by strong demand. On average, the market has grown 3% annually over the last several decades.

-

Green2 weeks ago

Green2 weeks agoRanked: Top Countries by Total Forest Loss Since 2001

-

Travel1 week ago

Travel1 week agoRanked: The World’s Top Flight Routes, by Revenue

-

Technology2 weeks ago

Technology2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

Real Estate2 weeks ago

Real Estate2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Markets2 weeks ago

Markets2 weeks agoCharted: Big Four Market Share by S&P 500 Audits

-

AI2 weeks ago

AI2 weeks agoThe Stock Performance of U.S. Chipmakers So Far in 2024

-

Automotive2 weeks ago

Automotive2 weeks agoAlmost Every EV Stock is Down After Q1 2024