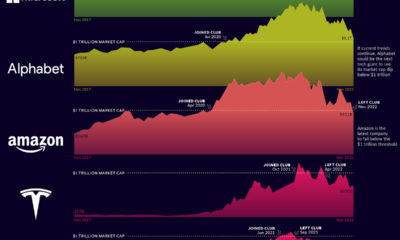

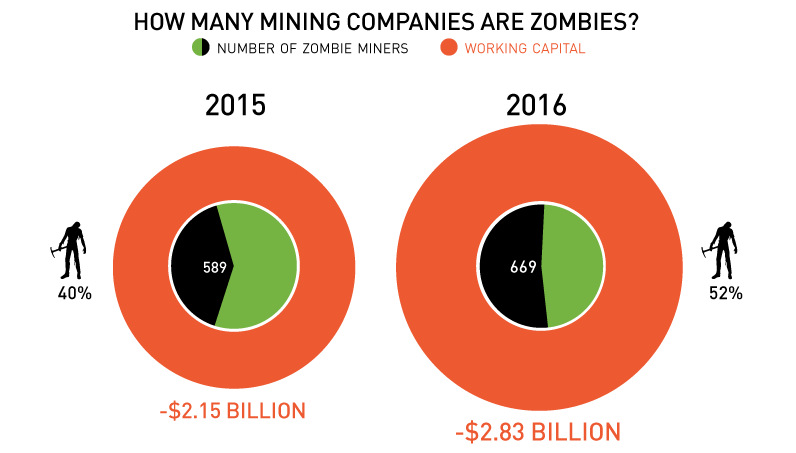

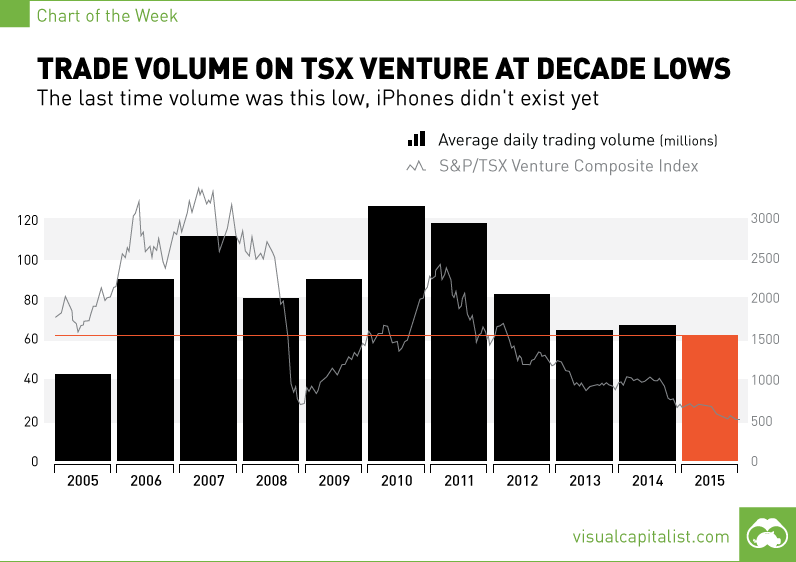

Mining

The Look and Feel of Canadian Venture Market Bottoms (From 1981 to 2014)

The Look and Feel of Canadian Venture Market Bottoms From 1981 to 2014

Special thanks to Dajin Resources for sponsoring. Also, information on market bottoms compiled by Ron Loewen.

In December 2014, the deteriorating market for metals and a suddenly floundering oil price pulled the resource-heavy TSX Venture Index to an all-time low.

Big board indices such as the S&P 500 are still reaching new highs each week, yet this is the second longest bear market since 1932 for gold stocks according to Barron’s Gold Mining Index (BGMI).

While it is difficult to discern if today’s market is truly the absolute bottom, the similarities in media headlines, the tone of discussion, and overall sentiment are reminiscent of bear markets past. That is why, in this infographic, we look at some of the major headlines at market bottoms over the past 35 years including those from the most recent downturn.

When it comes to companies such as those that make up the TSX Venture, it can be incredibly hard to judge fundamentals as there are no earnings or steady revenue growth for most companies. As a result, these markets are driven by greed and fear even more so than other sectors.

It’s important to be a contrarian and to go against the herd mentality. This doesn’t mean going against the grain no matter what, but it means thinking and acting with conviction based on fundamental market truths – regardless of what other people say.

We know that markets, especially those tied to natural resources, tend to be highly cyclical. With the large capital investments and timelines required to advance projects, massive supply challenges must be corrected in subsequent cycles. This can lead to either a rush to buy or sell, and therefore bull and bear markets.

We also know that investor sentiment is largely a psychological phenomenon that can be tied highly with emotions rather than fundamentals. The media can be a big part in echoing or reinforcing this sentiment.

Take a look at the headlines in bear markets bottoms over the last 35 years – do you think we’ve reached a similar place yet in this cycle?

Lithium

Ranked: The Top 10 EV Battery Manufacturers in 2023

Asia dominates this ranking of the world’s largest EV battery manufacturers in 2023.

The Top 10 EV Battery Manufacturers in 2023

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Despite efforts from the U.S. and EU to secure local domestic supply, all major EV battery manufacturers remain based in Asia.

In this graphic we rank the top 10 EV battery manufacturers by total battery deployment (measured in megawatt-hours) in 2023. The data is from EV Volumes.

Chinese Dominance

Contemporary Amperex Technology Co. Limited (CATL) has swiftly risen in less than a decade to claim the title of the largest global battery group.

The Chinese company now has a 34% share of the market and supplies batteries to a range of made-in-China vehicles, including the Tesla Model Y, SAIC’s MG4/Mulan, and various Li Auto models.

| Company | Country | 2023 Production (megawatt-hour) | Share of Total Production |

|---|---|---|---|

| CATL | 🇨🇳 China | 242,700 | 34% |

| BYD | 🇨🇳 China | 115,917 | 16% |

| LG Energy Solution | 🇰🇷 Korea | 108,487 | 15% |

| Panasonic | 🇯🇵 Japan | 56,560 | 8% |

| SK On | 🇰🇷 Korea | 40,711 | 6% |

| Samsung SDI | 🇰🇷 Korea | 35,703 | 5% |

| CALB | 🇨🇳 China | 23,493 | 3% |

| Farasis Energy | 🇨🇳 China | 16,527 | 2% |

| Envision AESC | 🇨🇳 China | 8,342 | 1% |

| Sunwoda | 🇨🇳 China | 6,979 | 1% |

| Other | - | 56,040 | 8% |

In 2023, BYD surpassed LG Energy Solution to claim second place. This was driven by demand from its own models and growth in third-party deals, including providing batteries for the made-in-Germany Tesla Model Y, Toyota bZ3, Changan UNI-V, Venucia V-Online, as well as several Haval and FAW models.

The top three battery makers (CATL, BYD, LG) collectively account for two-thirds (66%) of total battery deployment.

Once a leader in the EV battery business, Panasonic now holds the fourth position with an 8% market share, down from 9% last year. With its main client, Tesla, now sourcing batteries from multiple suppliers, the Japanese battery maker seems to be losing its competitive edge in the industry.

Overall, the global EV battery market size is projected to grow from $49 billion in 2022 to $98 billion by 2029, according to Fortune Business Insights.

-

Markets1 week ago

Markets1 week agoU.S. Debt Interest Payments Reach $1 Trillion

-

Business2 weeks ago

Business2 weeks agoCharted: Big Four Market Share by S&P 500 Audits

-

Real Estate2 weeks ago

Real Estate2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Demographics2 weeks ago

Demographics2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023