The Next Investing Frontier: Liquid Alternative ETFs

The following content is sponsored by IndexIQ.

The Next Investing Frontier: Liquid Alternative ETFs

Think back to your desires five years ago. As you’ve changed and the world around you has shifted, chances are your desires have also evolved. Similar progressions can be seen in the investing realm.

As investors have become more sophisticated, they have sought securities that provide:

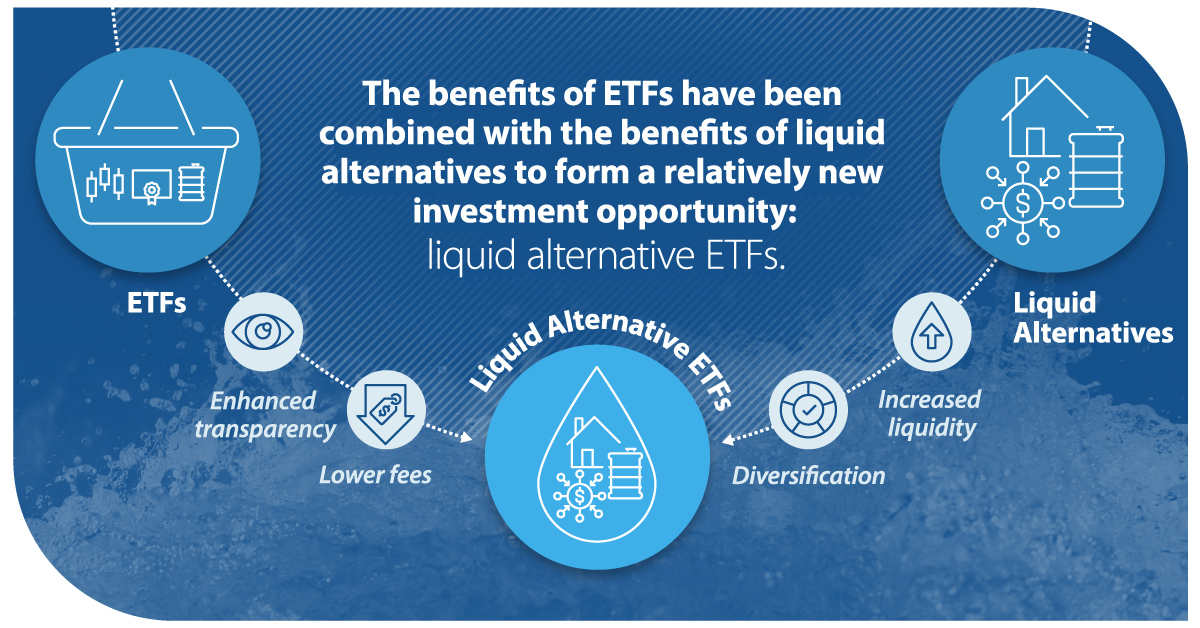

- Enhanced transparency

- Lower fees

- Increased liquidity

- Diversification

This changing behavior paved the way for emerging investment opportunities, including liquid alternative ETFs. In today’s infographic from IndexIQ, we explain what liquid alternative ETFs are, explore their benefits, and discuss how to use them in a portfolio.

What Are Liquid Alternative ETFs?

In order to define liquid alternative ETFs, it’s easier to break the term into two parts: liquid alternatives and ETFs.

Liquid alternatives are baskets of securities with exposure to alternative strategies. They can be accessed through ETFs, mutual funds, or closed-end funds with daily liquidity. Alternative investments are any asset that is not a stock or bond, such as commodities, real estate, or private equity.

ETFs are baskets of securities that trade on an exchange. They can contain various asset classes including stocks, bonds, commodities, or a mixture.

The benefits of ETFs have been combined with the benefits of liquid alternatives to form a relatively new investment opportunity: liquid alternative ETFs.

Liquid alternative ETFs are the subset of liquid alternatives that trade on an exchange. However, they are not widely used yet. In a recent survey, only 8% of institutional investors currently use them, or have used them in the past. Why aren’t more investors adding them to their portfolios?

Misconceptions about Liquidity

Simply put, there’s limited usage because investors lack understanding of the asset class. In fact, institutional investors view “liquidity during market stress” as the #1 disadvantage of liquid alternative ETFs.

In reality, liquid alternative ETFs are sufficiently liquid in most market conditions. ETFs benefit from two layers of liquidity: the liquidity of the ETF itself, and the liquidity of the underlying securities, known as implied liquidity.

Implied liquidity is accessed through market makers, typically large banks, that facilitate investor fund flows. If there is:

- Excess demand: Market makers buy the underlying securities, and sell ETF units.

- Excess supply: Market makers buy ETF units, and sell the underlying securities.

When investors sell ETF units for extended periods of time, market makers have many options at their disposal:

- Sell the individual underlying securities, adjusting their pricing to ensure profitability

- Hold ETF units and their underlying securities until the selling pressure dies down

- Hedge their risk by purchasing derivative instruments or ETFs from other market segments

This range of options ensures liquid alternative ETFs remain liquid, even in volatile markets.

Additional Benefits

Liquid alternative ETFs offer several key benefits for investors looking to branch out from their traditional portfolios.

Lower Fees

The average expense ratio for all 55 U.S. alternative ETFs is just 1.04%. In comparison, hedge funds charge an average management fee of 1.3%—plus a 20-30% performance fee.

Increased Transparency

In contrast to some alternative investments, liquid alternative ETFs provide a high degree of transparency in terms of investment strategy, holdings, reporting, and fees.

Enhanced Diversification

Liquid alternative ETFs have exhibited low correlations with traditional asset classes. Historically, this has provided increased diversification and mitigated risk.

In addition to their many benefits, liquid alternative ETFs are quite versatile in their applications.

Liquid Alternative ETFs in Practice

Institutional investors use this asset class in three main ways.

- Core Component: Investors use liquid alternative ETFs strategically as a long-term, diversifying portfolio component.

- Transition Management: While cash and money market funds are the most common transition vehicles, alternative ETFs provide efficient market exposure at a reasonable cost.

- Fund-of-funds replacement: Many institutional investors use fund-of-funds in their alternative portfolios, but this strategy brings additional fees, a lack of transparency, and potential overdiversification. Liquid alternative ETFs are a compelling replacement.

Whether an investor has short-term or long-term needs, liquid alternative ETFs are a useful tool.

Poised for Growth

With numerous benefits and applications, liquid alternative ETFs are gaining traction. In fact, the market is expected to grow nearly 2.5x by the end of 2020, from $47 billion to $114 billion.

As more institutional investors gain an understanding of this versatile asset class, they will be poised to implement a powerful tool that helps them achieve their clients’ goals.

-

Sponsored3 years ago

Sponsored3 years agoMore Than Precious: Silver’s Role in the New Energy Era (Part 3 of 3)

Long known as a precious metal, silver in solar and EV technologies will redefine its role and importance to a greener economy.

-

Sponsored7 years ago

Sponsored7 years agoThe History and Evolution of the Video Games Market

Everything from Pong to the rise of mobile gaming and AR/VR. Learn about the $100 billion video games market in this giant infographic.

-

Sponsored8 years ago

Sponsored8 years agoThe Extraordinary Raw Materials in an iPhone 6s

Over 700 million iPhones have now been sold, but the iPhone would not exist if it were not for the raw materials that make the technology...

-

Sponsored8 years ago

Sponsored8 years agoThe Industrial Internet, and How It’s Revolutionizing Mining

The convergence of the global industrial sector with big data and the internet of things, or the Industrial Internet, will revolutionize how mining works.