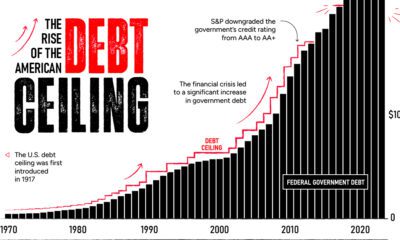

Debt

Visualizing the Snowball of Government Debt

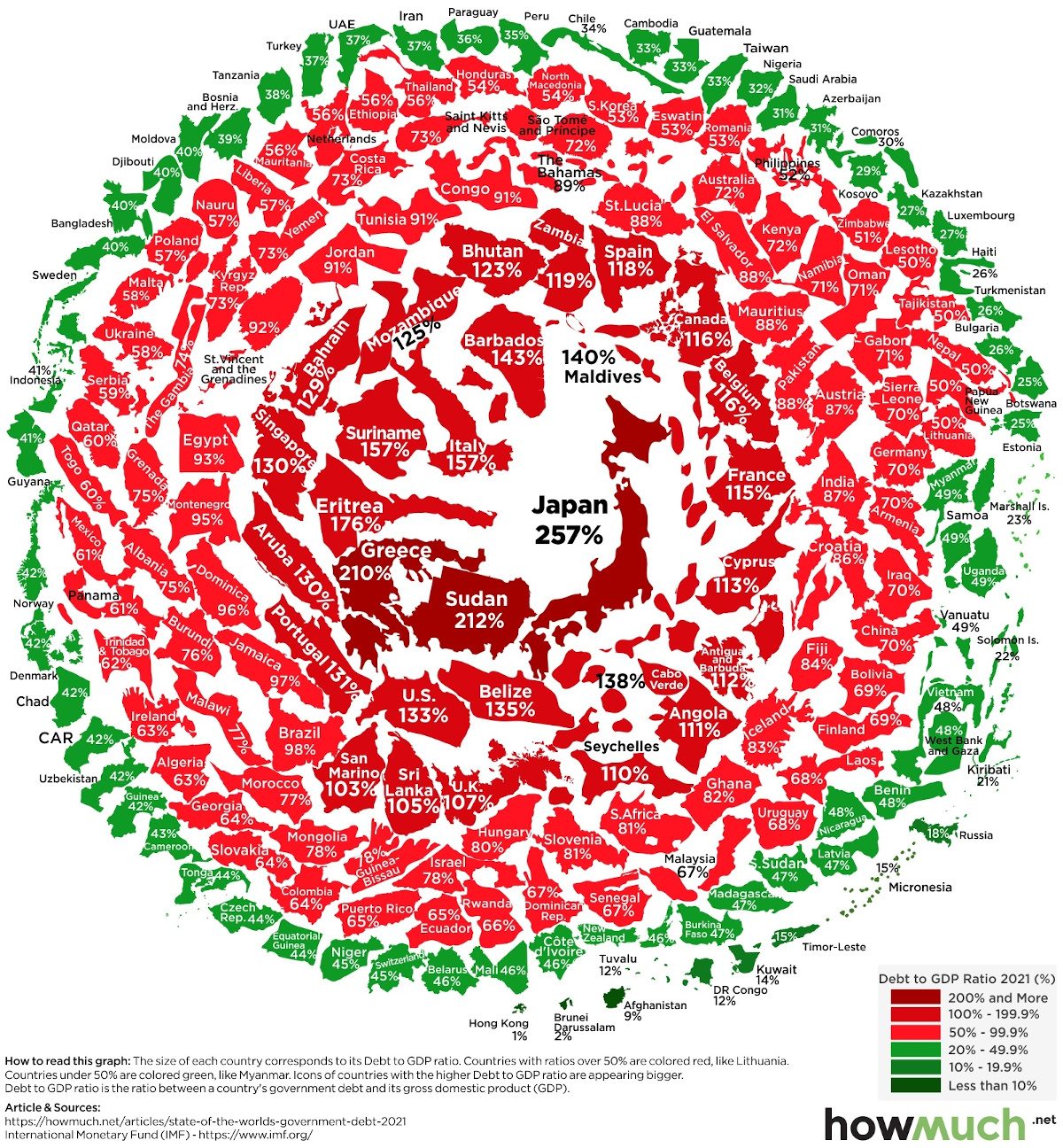

Visualizing the Snowball of Government Debt in 2021

As we approach the second half of 2021, many countries around the world are beginning to relax their COVID-19 restrictions.

And while this signals a return to normalcy for much of the global economy, there’s one subject that’s likely to remain controversial: government debt.

To see how each country is faring in the aftermath of an unprecedented global borrowing spree, this graphic from HowMuch.net visualizes debt-to-GDP ratios using April 2021 data from the International Monetary Fund (IMF).

Ranking the Top 10 in Government Debt

Government debt is often analyzed through the debt-to-GDP metric because it contextualizes an otherwise massive number.

Take for example the U.S. national debt, which currently sits at over $27 trillion. In isolation this figure sounds daunting, but when expressed as a % of U.S. GDP, it works out to a more relatable 133%. This format also allows us to make a better comparison between countries, especially when their economies differ in size.

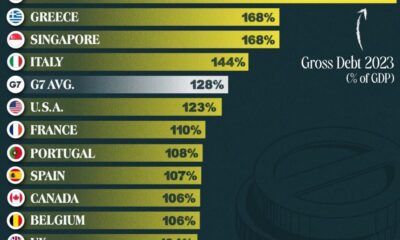

With that being said, here are the top 10 countries in terms of debt-to-GDP. For further context, we’ve included their 2019 and 2020 values as well.

| Rank (2021) | Country | Debt-to-GDP (2019) | Debt-to-GDP (2020) | Debt-to-GDP (April 2021) |

|---|---|---|---|---|

| #1 | 🇯🇵 Japan | 235% | 256% | 257% |

| #2 | 🇸🇩 Sudan | 200% | 262% | 212% |

| #3 | 🇬🇷 Greece | 185% | 213% | 210% |

| #4 | 🇪🇷 Eritrea | 189% | 185% | 176% |

| #5 | 🇸🇷 Suriname | 93% | 166% | 157% |

| #6 | 🇮🇹 Italy | 135% | 156% | 157% |

| #7 | 🇧🇧 Barbados | 127% | 149% | 143% |

| #8 | 🇲🇻 Maldives | 78% | 143% | 140% |

| #9 | 🇨🇻 Cape Verde | 125% | 139% | 138% |

| #10 | 🇧🇿 Belize | 98% | 127% | 135% |

Source: IMF

Japan tops the list with a ratio of 257%, though this isn’t really a surprise—the country’s debt-to-GDP ratio first surpassed 100% in the 1990s, and in 2010, it became the first advanced economy to reach 200%.

Such significant debt burdens are the result of non-traditional monetary policies, many of which were first implemented by Japan, then adopted by others. In the late 1990s, for instance, the Bank of Japan (BoJ) set interest rates at 0% to counter deflation and promote economic growth.

This low cost of borrowing enables businesses and governments to accumulate debt much more freely, and has seen widespread use among other developed nations post-2008.

What are the Risks?

Given that a majority of countries in this visual are red (meaning their debt-to-GDP ratios are over 50%), it’s safe to say that government borrowing is common practice.

But are large government debts a cause for concern?

Some believe that excessive borrowing will lead to higher interest costs in the long run, which could detract from economic growth and public sector investment. This theory is unlikely to become a reality anytime soon, however.

A recent report by RBC Wealth Management reported that the cost of servicing U.S. federal debt actually decreased in 2020, thanks to the low borrowing costs mentioned previously.

Perhaps a more prescient question would be: how long can the world’s central banks keep interest rates at near-zero levels?

Money

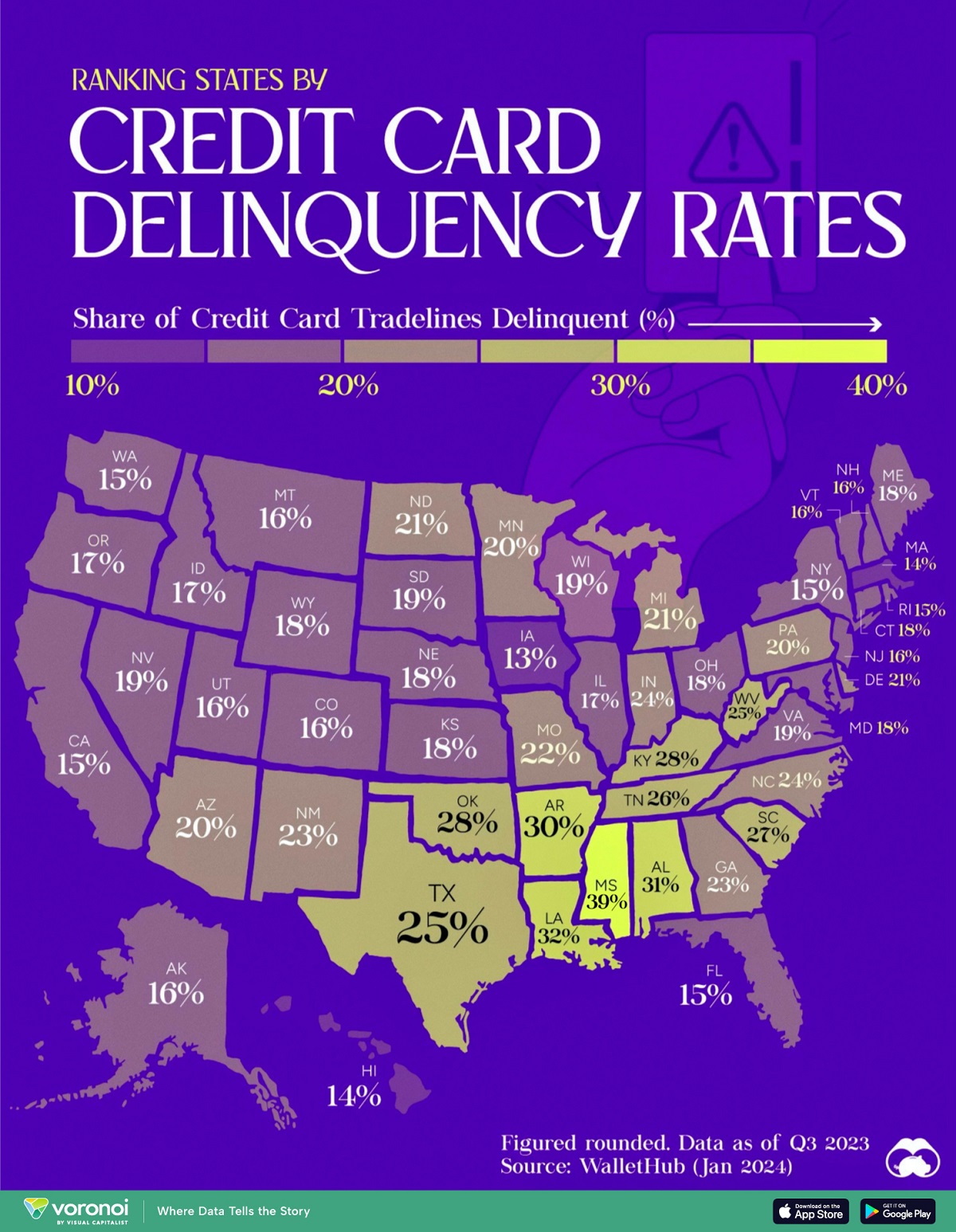

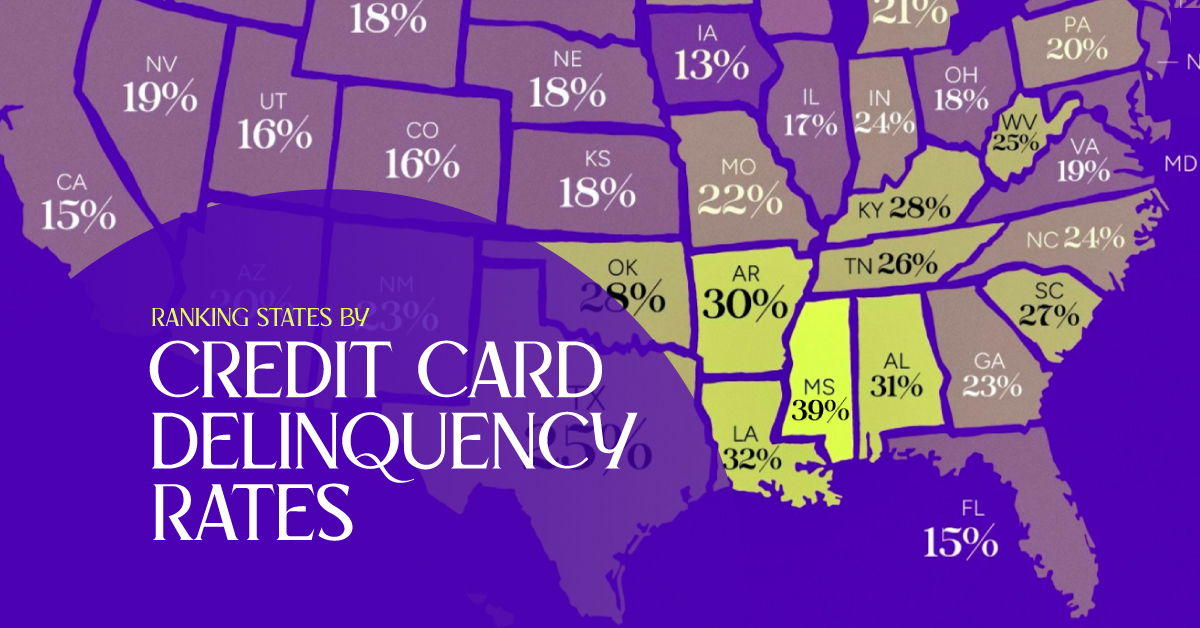

Mapping Credit Card Delinquency Rates in the U.S. by State

Which states have the lowest credit card delinquency rates in America, and which have the highest?

Credit Card Delinquency Rates in the U.S. by State

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Credit card debt carries a hefty bill in America, and falling behind on payments can be extremely costly for cardholders.

This graphic shows credit card delinquency rates across 50 U.S. states, as of Q3 2023. This data comes from a WalletHub study published in January 2024.

Which States Have the Lowest and Highest Delinquency Rates?

Credit card delinquency is when a cardholder falls behind on required monthly payments. Credit agencies are often notified after two months of delinquent payments.

WalletHub examined proprietary user data on the average number of delinquent credit card tradelines—also known as credit accounts—across states. Here they are from lowest to highest:

| Rank | State | Share of Credit Card Tradelines Delinquent (%) |

|---|---|---|

| 1 | Iowa | 12.9 |

| 2 | Massachusetts | 13.9 |

| 3 | Hawaii | 13.9 |

| 4 | Rhode Island | 14.7 |

| 5 | Washington | 14.7 |

| 6 | Florida | 14.8 |

| 7 | New York | 14.9 |

| 8 | California | 15.1 |

| 9 | New Hampshire | 15.5 |

| 10 | Alaska | 15.6 |

| 11 | New Jersey | 15.6 |

| 12 | Colorado | 15.7 |

| 13 | Utah | 15.8 |

| 14 | Vermont | 16.1 |

| 15 | Montana | 16.1 |

| 16 | Illinois | 16.5 |

| 17 | Oregon | 16.6 |

| 18 | Idaho | 17.0 |

| 19 | Ohio | 17.5 |

| 20 | Connecticut | 17.8 |

| 21 | Maine | 18.0 |

| 22 | Nebraska | 18.1 |

| 23 | Wyoming | 18.1 |

| 24 | Maryland | 18.4 |

| 25 | Kansas | 18.4 |

| 26 | Wisconsin | 18.5 |

| 27 | Virginia | 18.7 |

| 28 | Nevada | 19.1 |

| 29 | South Dakota | 19.3 |

| 30 | Arizona | 19.8 |

| 31 | Minnesota | 19.8 |

| 32 | Pennsylvania | 20.2 |

| 33 | Michigan | 20.9 |

| 34 | North Dakota | 21.3 |

| 35 | Delaware | 21.4 |

| 36 | Missouri | 22.4 |

| 37 | New Mexico | 22.6 |

| 38 | Georgia | 23.1 |

| 39 | North Carolina | 24.0 |

| 40 | Indiana | 24.3 |

| 41 | Texas | 24.7 |

| 42 | West Virginia | 25.2 |

| 43 | Tennessee | 26.2 |

| 44 | South Carolina | 26.9 |

| 45 | Kentucky | 27.6 |

| 46 | Oklahoma | 28.2 |

| 47 | Arkansas | 30.1 |

| 48 | Alabama | 30.5 |

| 49 | Louisiana | 31.7 |

| 50 | Mississippi | 39.1 |

No state had credit delinquency rates of less than 10%, with Iowa coming the closest at 12.9%.

That puts Iowa ahead of wealthier states like Massachusetts (13.9%), Washington (14.7%), and New Hampshire (15.5%).

At the bottom end was Mississippi, which had 39% credit delinquency rates to end 2023. That’s well ahead of the next-lowest states Louisiana (31.7%) and Alabama (30.5%).

It’s notable that the American South had higher rates of delinquency almost across the board. The five states with the highest rates of credit card delinquency are all located in the southeastern region of the country, and Texas had a higher delinquency rate (25%) than other majorly populated states like Florida (14.8%) and New York (14.9%).

-

Mining2 weeks ago

Mining2 weeks agoCharted: The Value Gap Between the Gold Price and Gold Miners

-

Real Estate1 week ago

Real Estate1 week agoRanked: The Most Valuable Housing Markets in America

-

Business1 week ago

Business1 week agoCharted: Big Four Market Share by S&P 500 Audits

-

AI1 week ago

AI1 week agoThe Stock Performance of U.S. Chipmakers So Far in 2024

-

Misc1 week ago

Misc1 week agoAlmost Every EV Stock is Down After Q1 2024

-

Money2 weeks ago

Money2 weeks agoWhere Does One U.S. Tax Dollar Go?

-

Green2 weeks ago

Green2 weeks agoRanked: Top Countries by Total Forest Loss Since 2001

-

Real Estate2 weeks ago

Real Estate2 weeks agoVisualizing America’s Shortage of Affordable Homes