Gold

The Global War on Cash

The Global War on Cash

The Money Project is an ongoing collaboration between Visual Capitalist and Texas Precious Metals that seeks to use intuitive visualizations to explore the origins, nature, and use of money.

There is a global push by lawmakers to eliminate the use of physical cash around the world. This movement is often referred to as “The War on Cash”, and there are three major players involved:

1. The Initiators

Who?

Governments, central banks.

Why?

The elimination of cash will make it easier to track all types of transactions – including those made by criminals.

2. The Enemy

Who?

Criminals, terrorists

Why?

Large denominations of bank notes make illegal transactions easier to perform, and increase anonymity.

3. The Crossfire

Who?

Citizens

Why?

The coercive elimination of physical cash will have potential repercussions on the economy and social liberties.

Is Cash Still King?

Cash has always been king – but starting in the late 1990s, the convenience of new technologies have helped make non-cash transactions to become more viable:

- Online banking

- Smartphones

- Payment technologies

- Encryption

By 2015, there were 426 billion cashless transactions worldwide – a 50% increase from five years before.

| Year | # of cashless transactions |

|---|---|

| 2010 | 285.2 billion |

| 2015 | 426.3 billion |

And today, there are multiple ways to pay digitally, including:

- Online banking (Visa, Mastercard, Interac)

- Smartphones (Apple Pay)

- Intermediaries ( Paypal , Square)

- Cryptocurrencies (Bitcoin)

The First Shots Fired

The success of these new technologies have prompted lawmakers to posit that all transactions should now be digital.

Here is their case for a cashless society:

Removing high denominations of bills from circulation makes it harder for terrorists, drug dealers, money launderers, and tax evaders.

- $1 million in $100 bills weighs only one kilogram (2.2 lbs).

- Criminals move $2 trillion per year around the world each year.

- The U.S. $100 bill is the most popular note in the world, with 10 billion of them in circulation.

This also gives regulators more control over the economy.

- More traceable money means higher tax revenues.

- It means there is a third-party for all transactions.

- Central banks can dictate interest rates that encourage (or discourage) spending to try to manage inflation. This includes ZIRP or NIRP policies.

Cashless transactions are faster and more efficient.

- Banks would incur less costs by not having to handle cash.

- It also makes compliance and reporting easier.

- The “burden” of cash can be up to 1.5% of GDP, according to some experts.

But for this to be possible, they say that cash – especially large denomination bills – must be eliminated. After all, cash is still used for about 85% of all transactions worldwide.

A Declaration of War

Governments and central banks have moved swiftly in dozens of countries to start eliminating cash.

Some key examples of this? Australia, Singapore, Venezuela, the U.S., and the European Central Bank have all eliminated (or have proposed to eliminate) high denomination notes. Other countries like France, Sweden and Greece have targeted adding restrictions on the size of cash transactions, reducing the amount of ATMs in the countryside, or limiting the amount of cash that can be held outside of the banking system. Finally, some countries have taken things a full step further – South Korea aims to eliminate paper currency in its entirety by 2020.

But right now, the “War on Cash” can’t be mentioned without invoking images of day-long lineups in India. In November 2016, Indian Prime Minister Narendra Modi demonetized 500 and 1000 rupee notes, eliminating 86% of the country’s notes overnight. While Indians could theoretically exchange 500 and 1,000 rupee notes for higher denominations, it was only up to a limit of 4,000 rupees per person. Sums above that had to be routed through a bank account in a country where only 50% of Indians have such access.

The Hindu has reported that there have now been 112 reported deaths associated with the Indian demonetization. Some people have committed suicide, but most deaths come from elderly people waiting in bank queues for hours or days to exchange money.

Caught in the Crossfire

The shots fired by governments to fight its war on cash may have several unintended casualties:

1. Privacy

- Cashless transactions would always include some intermediary or third-party.

- Increased government access to personal transactions and records.

- Certain types of transactions (gambling, etc.) could be barred or frozen by governments.

- Decentralized cryptocurrency could be an alternative for such transactions

2. Savings

- Savers could no longer have the individual freedom to store wealth “outside” of the system.

- Eliminating cash makes negative interest rates (NIRP) a feasible option for policymakers.

- A cashless society also means all savers would be “on the hook” for bank bail-in scenarios.

- Savers would have limited abilities to react to extreme monetary events like deflation or inflation.

3. Human Rights

- Rapid demonetization has violated people’s rights to life and food.

- In India, removing the 500 and 1,000 rupee notes has caused multiple human tragedies, including patients being denied treatment and people not being able to afford food.

- Demonetization also hurts people and small businesses that make their livelihoods in the informal sectors of the economy.

4. Cybersecurity

- With all wealth stored digitally, the potential risk and impact of cybercrime increases.

- Hacking or identity theft could destroy people’s entire life savings.

- The cost of online data breaches is already expected to reach $2.1 trillion by 2019, according to Juniper Research.

As the War on Cash accelerates, many shots will be fired. The question is: who will take the majority of the damage?

Mining

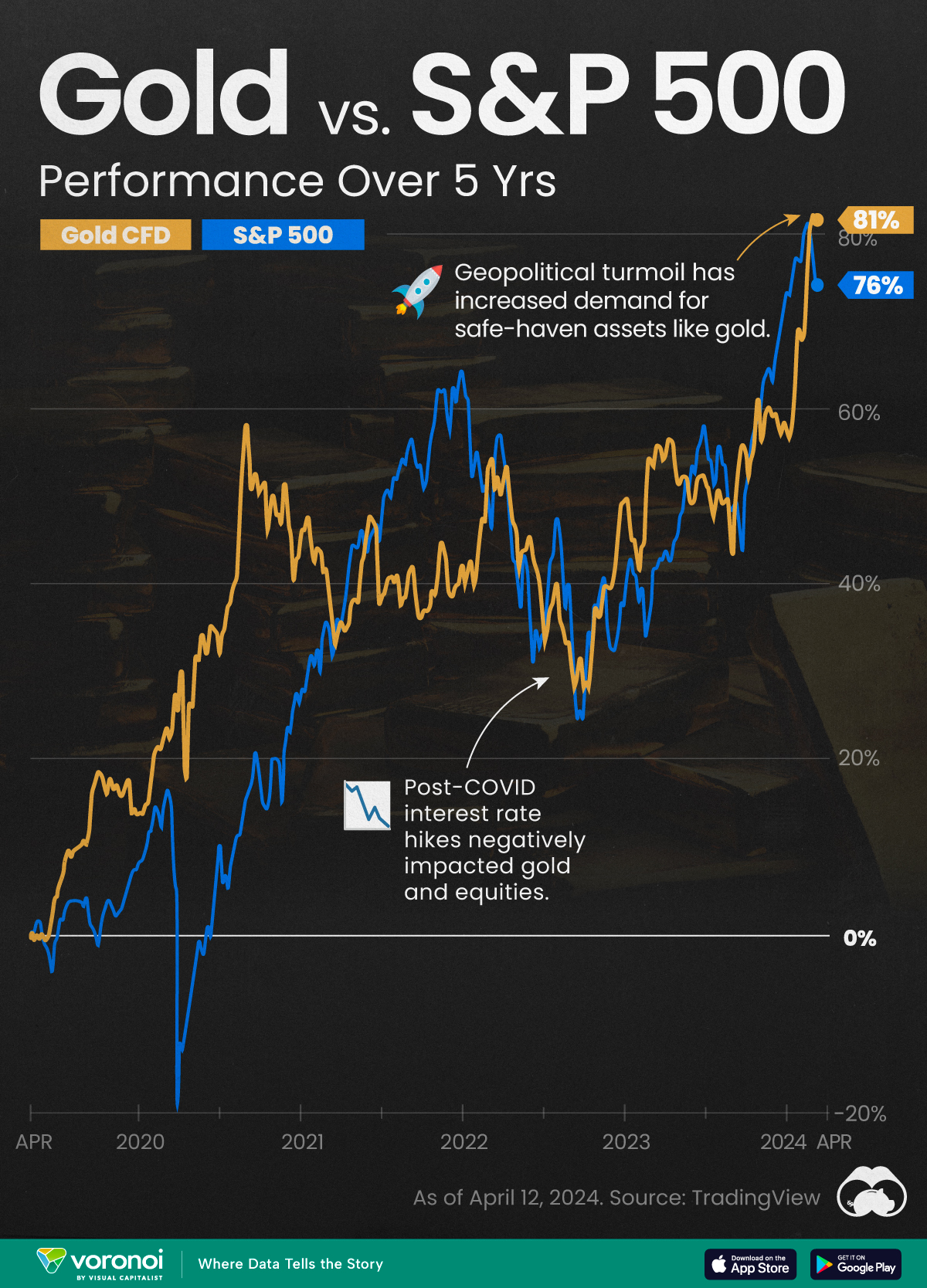

Gold vs. S&P 500: Which Has Grown More Over Five Years?

The price of gold has set record highs in 2024, but how has this precious metal performed relative to the S&P 500?

Gold vs. S&P 500: Which Has Grown More Over Five Years?

This was originally posted on our Voronoi app. Download the app for free on Apple or Android and discover incredible data-driven charts from a variety of trusted sources.

Gold is considered a unique asset due to its enduring value, historical significance, and application in various technologies like computers, spacecraft, and communications equipment.

Commonly regarded as a “safe haven asset”, gold is something investors typically buy to protect themselves during periods of global uncertainty and economic decline.

It is for this reason that gold has performed rather strongly in recent years, and especially in 2024. Persistent inflation combined with multiple wars has driven up demand for gold, helping it set a new all-time high of over $2,400 per ounce.

To put this into perspective, we visualized the performance of gold alongside the S&P 500. See the table below for performance figures as of April 12, 2024.

| Asset/Index | 1 Yr (%) | 5 Yr (%) |

|---|---|---|

| 🏆 Gold | +16.35 | +81.65 |

| 💼 S&P 500 | +25.21 | +76.22 |

Over the five-year period, gold has climbed an impressive 81.65%, outpacing even the S&P 500.

Get Your Gold at Costco

Perhaps a sign of how high the demand for gold is becoming, wholesale giant Costco is reportedly selling up to $200 million worth of gold bars every month in the United States. The year prior, sales only amounted to $100 million per quarter.

Consumers aren’t the only ones buying gold, either. Central banks around the world have been accumulating gold in very large quantities, likely as a hedge against inflation.

According to the World Gold Council, these institutions bought 1,136 metric tons in 2022, marking the highest level since 1950. Figures for 2023 came in at 1,037 metric tons.

See More Graphics on Gold

If you’re fascinated by gold, be sure to check out more Visual Capitalist content including 200 Years of Global Gold Production, by Country or Ranked: The Largest Gold Reserves by Country.

-

Real Estate2 weeks ago

Real Estate2 weeks agoVisualizing America’s Shortage of Affordable Homes

-

Technology1 week ago

Technology1 week agoRanked: Semiconductor Companies by Industry Revenue Share

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

Real Estate2 weeks ago

Real Estate2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Business2 weeks ago

Business2 weeks agoCharted: Big Four Market Share by S&P 500 Audits

-

AI2 weeks ago

AI2 weeks agoThe Stock Performance of U.S. Chipmakers So Far in 2024

-

Misc2 weeks ago

Misc2 weeks agoAlmost Every EV Stock is Down After Q1 2024

-

Money2 weeks ago

Money2 weeks agoWhere Does One U.S. Tax Dollar Go?