Ethical Supply: The Search for Cobalt Beyond the Congo

The following content is sponsored by Fuse Cobalt.

Ethical Supply: The Search for Cobalt Beyond the Congo

Each new generation finds new uses for materials, and cobalt is no exception.

Historically, potters and painters used cobalt as dye to color their work. Today, a new cobalt supply chain is emerging to build the next generation of clean energy.

However, there is lack of transparency surrounding the current supply chain for cobalt, as the metal is subject to a number of ethical issues from its main country of production—the Democratic Republic of Congo (DRC).

Today’s infographic comes to us from Fuse Cobalt and uncovers the potential for new sources of cobalt beyond the Congo.

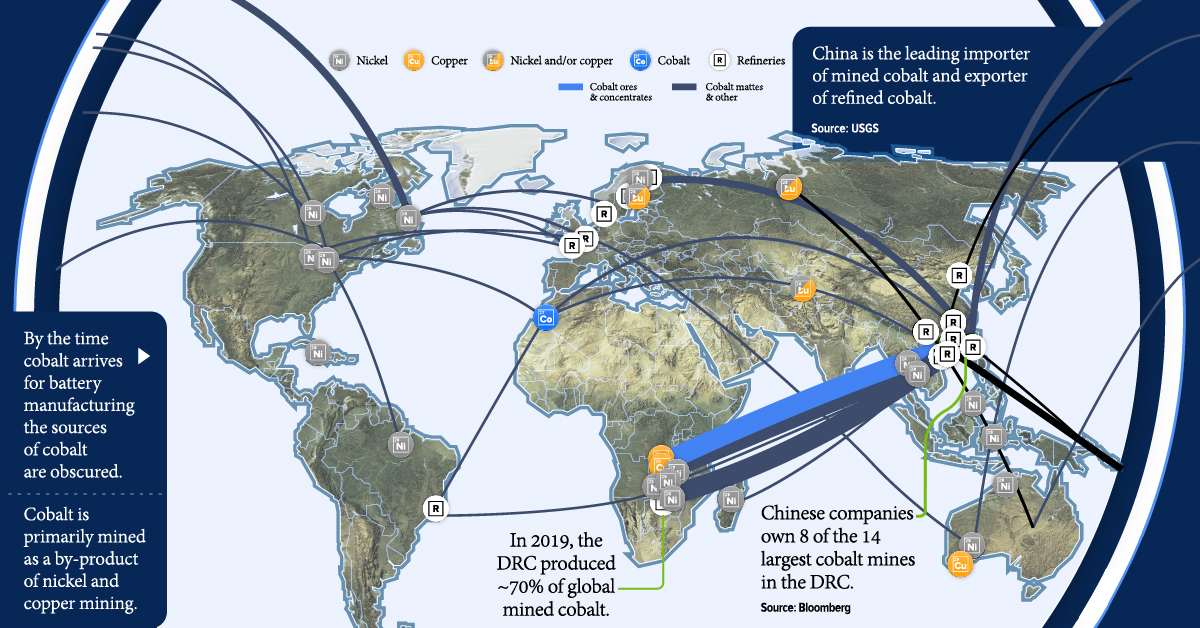

Cobalt’s Growing Demand

Cobalt’s specialized properties make it crucial for rechargeable batteries, metal alloys, and EVs:

- Thermal stability

- High energy storage

- Corrosion resistance

- Aesthetic appeal

As the markets for EVs and rechargeable batteries grow, the demand for cobalt is expected to surge to 220,000 metric tons by 2025, a 63% increase since 2017.

But can industry meet its demand with a supply of ethically mined cobalt?

A Precarious Supply Chain

In 2019, the DRC produced 70% of global mined cobalt—a majority of which went to China, the leading importer of mined cobalt and an exporter of refined cobalt.

Moreover, 8 of the 14 largest cobalt mines in the DRC are owned by Chinese companies, resulting in a highly controlled supply chain.

Why the Democratic Republic of Congo?

When it comes to cobalt reserves and concentrations, DRC looms over the rest of the world as a clear leader.

| Country | Cobalt reserves as of 2019 (tons) |

|---|---|

| Congo (Kinshasa) | 3,600,000 |

| Australia | 1,200,000 |

| Cuba | 500,000 |

| Philippines | 260,000 |

| Russia | 250,000 |

| Canada | 230,000 |

| Madagascar | 120,000 |

| China | 80,000 |

| Papua New Guinea | 56,000 |

| United States | 55,000 |

| South Africa | 50,000 |

| Morocco | 18,000 |

| Rest of the World | 500,000 |

| World total (rounded) | 7,000,000 |

The African Copper Belt hosts the majority of the DRC’s cobalt deposits, where it is primarily mined as a by-product of copper and nickel mining.

Low labor costs, loose regulations, and poor governance in the DRC allow for the flourishing of artisanal mining and cheap sources of cobalt.

However, cobalt from the DRC is tainted by ethical and humanitarian issues, including:

- Child labor

- Corruption

- Crime

- Poverty

- Hazardous artisanal mining

With the current supply chain of cobalt facing scrutiny and criticism, a transformation in the cobalt universe is well underway.

Cobalt’s Changing Landscape

As consumers become aware of the dirty costs of cobalt mining in the DRC, battery and EV manufacturing companies are looking for ethical sources.

Tesla, BMW, Ford, and Volkswagen are part of more than 380 companies that have committed to responsible sourcing through the Responsible Minerals Initiative. Responsible sourcing entails increasing supply chain transparency and searching for sources of cobalt outside the DRC.

Here’s how some companies are leading the way:

- Ford, Huayou Cobalt, IBM, LG Chem, and RCS Global are using blockchain technology to improve transparency and trace the sources of cobalt.

- BMW signed a $110 million deal for cobalt from Morocco’s Bou Azzar Mine, in an effort to avoid cobalt sourced from the DRC.

- Tesla agreed to buy 6,000 tonnes of cobalt annually from Glencore, a multinational company financing North America’s first cobalt refinery.

The U.S. recently added cobalt to its list of critical minerals—minerals for which it seeks independence from imports. The effort aims to reduce its net import reliance of 78% for cobalt, encouraging more localized and reliable production.

As a result of these shifts, the entire supply chain is beginning to reconsider cobalt sources in better-managed jurisdictions.

Cobalt Beyond the Congo: Why Not North America?

North America has comparable sources of cobalt to what is found in the Congo. As of 2019, Canada had 230,000 tons in cobalt reserves, whereas the U.S. had 55,000 tons.

Canadian Opportunity

Ontario hosts some high-grade cobalt deposits such as the Cobalt Silver Queen, Nova Scotia, Drummond, Nipissing, and Cobalt Lode mines.

In fact, Bill Gates, Jeff Bezos, and other billionaires from the Breakthrough Energy Fund are already fueling the exploration and development of cobalt deposits in North America.

Unsung North American Potential

The United States is home to 60 identified deposits of cobalt. These sources along with Canada’s deposits, should provide explorers and miners with a massive opportunity to develop cobalt mining in North America.

As the EV industry booms with gigafactories in construction, will North American carmakers and other battery makers be able to pivot to ethical, local raw materials?

-

Sponsored3 years ago

Sponsored3 years agoMore Than Precious: Silver’s Role in the New Energy Era (Part 3 of 3)

Long known as a precious metal, silver in solar and EV technologies will redefine its role and importance to a greener economy.

-

Sponsored7 years ago

Sponsored7 years agoThe History and Evolution of the Video Games Market

Everything from Pong to the rise of mobile gaming and AR/VR. Learn about the $100 billion video games market in this giant infographic.

-

Sponsored8 years ago

Sponsored8 years agoThe Extraordinary Raw Materials in an iPhone 6s

Over 700 million iPhones have now been sold, but the iPhone would not exist if it were not for the raw materials that make the technology...

-

Sponsored8 years ago

Sponsored8 years agoThe Industrial Internet, and How It’s Revolutionizing Mining

The convergence of the global industrial sector with big data and the internet of things, or the Industrial Internet, will revolutionize how mining works.