Markets

How the World’s Most Elite Growth Investors Pick Stocks

Investing can be extremely psychologically demanding.

Not only are you up against the world’s best investors, but you’re also up against yourself. It’s easy to get caught making irrational decisions based on your own personal blindspots or cognitive biases, and these mistakes can lead to buying when you should sell, and vice versa.

For the above reasons, the most successful investors are often those that have rational and proven systems in place.

Having a method to your madness allows you to have confidence in your decisions, while also taking advantage of the strategies and heuristics that have performed well for the world’s most elite investors.

How to Pick Growth Stocks

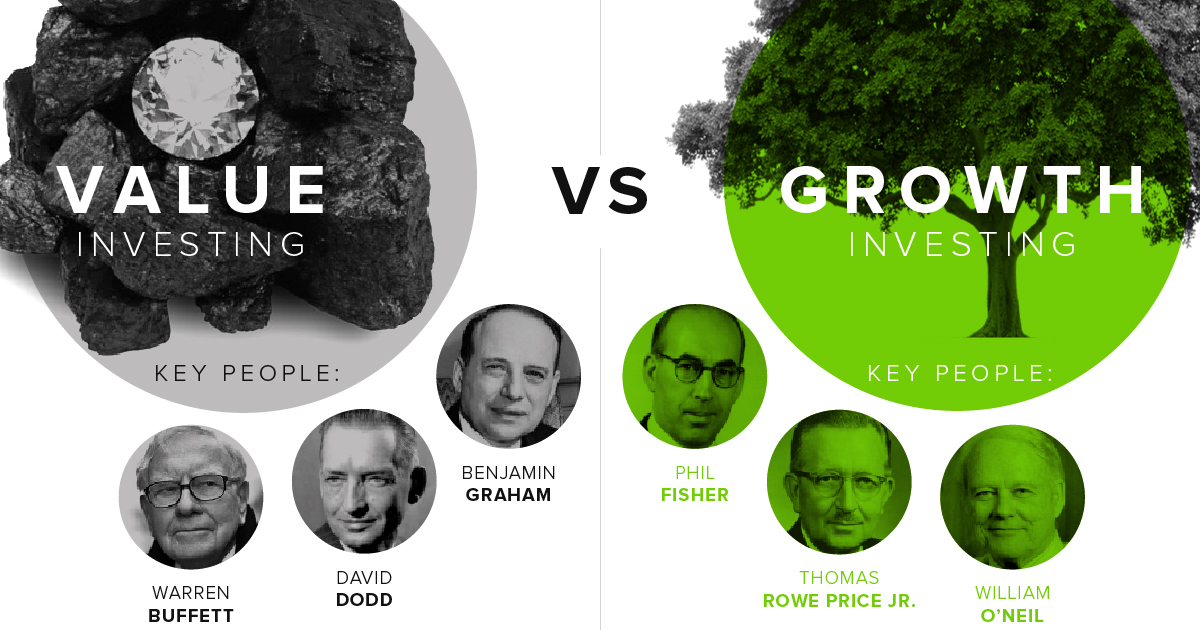

Today’s infographic comes to us from Investor’s Business Daily, and it details the basics around the discipline of growth investing, including the differences the school has with value investing.

More importantly, it also provides a framework for choosing growth stocks used by elite investors such as William J. O’Neil.

Growth investing is all about identifying the companies that are exhibiting behavior that suggests that they will be tomorrow’s leaders.

The benefits to this strategy, if successful, are easy to see. Think about buying Microsoft before it dominated the software industry, or Starbucks before it conquered the United States with its new approach to coffee culture.

The question is: how can these stocks be found reliably?

The CAN SLIM Approach

Fantastic growth stocks don’t just grow on trees – instead, you have to have a system to sift through them.

One easy place to start your search for the next growth leader is with an approach pioneered with investing legend William J. O’Neil. Developed in the 1950s, the CAN SLIM strategy identifies seven characteristics that top-performing stocks often share before making their biggest price gains.

Each characteristic is represented by a letter in the CAN SLIM acronym:

C – Current quarterly earnings

A – Annual earnings growth

N – New product, service, management, or price high

S – Supply and demand

L – Leader or laggard

I – Institutional sponsorship

M – Market direction

Importantly, each of these traits can be a catalyst to influence other traits. When they compound, it can lead to big price movements that beat the rest of the market.

Breaking Down the Factors

Let’s look at each characteristic of the CAN SLIM approach in more detail:

Current quarterly earnings

Look for companies with a minimum earnings-per share (EPS) growth of 25% in the most recent quarter, though 50% or higher is even better. These companies should also have 20% sales growth in the quarter, and a 17% ROE to ensure that growth is sustainable.

Annual earnings growth

Look for companies with annual EPS growth of at least 25% to 50% in each of the previous 3-5 years. This helps confirm that the company is showing long-term growth.

New product, service, management, or price high

What is the company doing that is new or game-changing? To be a market winner, a company must constantly reinvent itself to position itself for higher-than-average profits.

Examples: Consider Google’s monetization of search ads, or McDonald’s novel approach to food. These innovations set the companies up for massive profits and success.

Supply and demand

A stock price increases when more investors demand an increasingly limited supply of shares. Spikes in price, along with volume accumulation, mean that demand is increasing. If this is coming from institutional investors, who tend to buy and hold, it’s even better.

Leader or laggard

The leading companies in leading industries – the best of the best – will be the companies that have the most growth potential.

Institutional sponsorship

75% of all market activity comes from professional investors, such as mutual funds or pension funds. Not only does the smart money help validate a potential growth stock by being involved, but they can trigger big price increases.

Market direction

CAN SLIM investors believe you should invest with the market, as opposed to against it. That’s because an individual stock moves with the market 75% of the time.

Putting it Together

Understanding how the different CAN SLIM factors work together – and how they can help bring massive bouts of growth for the underlying stock – is key for the successful growth investor.

Using a rational system like this also helps you in overcoming cognitive biases or making other mistakes that may affect your investments, as well.

Markets

U.S. Debt Interest Payments Reach $1 Trillion

U.S. debt interest payments have surged past the $1 trillion dollar mark, amid high interest rates and an ever-expanding debt burden.

U.S. Debt Interest Payments Reach $1 Trillion

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

The cost of paying for America’s national debt crossed the $1 trillion dollar mark in 2023, driven by high interest rates and a record $34 trillion mountain of debt.

Over the last decade, U.S. debt interest payments have more than doubled amid vast government spending during the pandemic crisis. As debt payments continue to soar, the Congressional Budget Office (CBO) reported that debt servicing costs surpassed defense spending for the first time ever this year.

This graphic shows the sharp rise in U.S. debt payments, based on data from the Federal Reserve.

A $1 Trillion Interest Bill, and Growing

Below, we show how U.S. debt interest payments have risen at a faster pace than at another time in modern history:

| Date | Interest Payments | U.S. National Debt |

|---|---|---|

| 2023 | $1.0T | $34.0T |

| 2022 | $830B | $31.4T |

| 2021 | $612B | $29.6T |

| 2020 | $518B | $27.7T |

| 2019 | $564B | $23.2T |

| 2018 | $571B | $22.0T |

| 2017 | $493B | $20.5T |

| 2016 | $460B | $20.0T |

| 2015 | $435B | $18.9T |

| 2014 | $442B | $18.1T |

| 2013 | $425B | $17.2T |

| 2012 | $417B | $16.4T |

| 2011 | $433B | $15.2T |

| 2010 | $400B | $14.0T |

| 2009 | $354B | $12.3T |

| 2008 | $380B | $10.7T |

| 2007 | $414B | $9.2T |

| 2006 | $387B | $8.7T |

| 2005 | $355B | $8.2T |

| 2004 | $318B | $7.6T |

| 2003 | $294B | $7.0T |

| 2002 | $298B | $6.4T |

| 2001 | $318B | $5.9T |

| 2000 | $353B | $5.7T |

| 1999 | $353B | $5.8T |

| 1998 | $360B | $5.6T |

| 1997 | $368B | $5.5T |

| 1996 | $362B | $5.3T |

| 1995 | $357B | $5.0T |

| 1994 | $334B | $4.8T |

| 1993 | $311B | $4.5T |

| 1992 | $306B | $4.2T |

| 1991 | $308B | $3.8T |

| 1990 | $298B | $3.4T |

| 1989 | $275B | $3.0T |

| 1988 | $254B | $2.7T |

| 1987 | $240B | $2.4T |

| 1986 | $225B | $2.2T |

| 1985 | $219B | $1.9T |

| 1984 | $205B | $1.7T |

| 1983 | $176B | $1.4T |

| 1982 | $157B | $1.2T |

| 1981 | $142B | $1.0T |

| 1980 | $113B | $930.2B |

| 1979 | $96B | $845.1B |

| 1978 | $84B | $789.2B |

| 1977 | $69B | $718.9B |

| 1976 | $61B | $653.5B |

| 1975 | $55B | $576.6B |

| 1974 | $50B | $492.7B |

| 1973 | $45B | $469.1B |

| 1972 | $39B | $448.5B |

| 1971 | $36B | $424.1B |

| 1970 | $35B | $389.2B |

| 1969 | $30B | $368.2B |

| 1968 | $25B | $358.0B |

| 1967 | $23B | $344.7B |

| 1966 | $21B | $329.3B |

Interest payments represent seasonally adjusted annual rate at the end of Q4.

At current rates, the U.S. national debt is growing by a remarkable $1 trillion about every 100 days, equal to roughly $3.6 trillion per year.

As the national debt has ballooned, debt payments even exceeded Medicaid outlays in 2023—one of the government’s largest expenditures. On average, the U.S. spent more than $2 billion per day on interest costs last year. Going further, the U.S. government is projected to spend a historic $12.4 trillion on interest payments over the next decade, averaging about $37,100 per American.

Exacerbating matters is that the U.S. is running a steep deficit, which stood at $1.1 trillion for the first six months of fiscal 2024. This has accelerated due to the 43% increase in debt servicing costs along with a $31 billion dollar increase in defense spending from a year earlier. Additionally, a $30 billion increase in funding for the Federal Deposit Insurance Corporation in light of the regional banking crisis last year was a major contributor to the deficit increase.

Overall, the CBO forecasts that roughly 75% of the federal deficit’s increase will be due to interest costs by 2034.

-

Green1 week ago

Green1 week agoRanking the Top 15 Countries by Carbon Tax Revenue

-

Technology2 weeks ago

Technology2 weeks agoThe Stock Performance of U.S. Chipmakers So Far in 2024

-

Markets2 weeks ago

Markets2 weeks agoCharted: Big Four Market Share by S&P 500 Audits

-

Real Estate2 weeks ago

Real Estate2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Travel2 weeks ago

Travel2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Countries2 weeks ago

Countries2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075