Money

The Big Mac Index: A Measure of Purchasing Power Parity & Burger Inflation

Article/Editing:

The Big Mac Index: A Measure of PPP and Burger Inflation

The Big Mac was created in 1967 by Jim Delligati, a McDonald’s franchise owner in Pennsylvania. It was launched throughout the U.S. the following year, and today you can buy one in more than 70 countries. However, the price you pay will vary based on where you are, as evidenced by the Big Mac Index.

Spanning from 2004-2022, this animation from James Eagle shows the U.S. dollar price of a Big Mac in select countries around the world.

What Does the Big Mac Index Show?

The Big Mac Index was invented by The Economist in 1986. It is intended to be a lighthearted way to demonstrate the concept of purchasing power parity. In other words, it helps illustrate the idea that market exchange rates between countries may be “out of whack” when compared to the cost of buying the same basket of goods and services in those places.

Given that McDonald’s is one of the biggest companies in the world and the Big Mac is widely available globally, it means that the famous burger can be used as a basic goods comparison between most countries. It also has the advantage of having the same inputs and distribution system, with a few minor modifications (like chicken patties in India instead of beef).

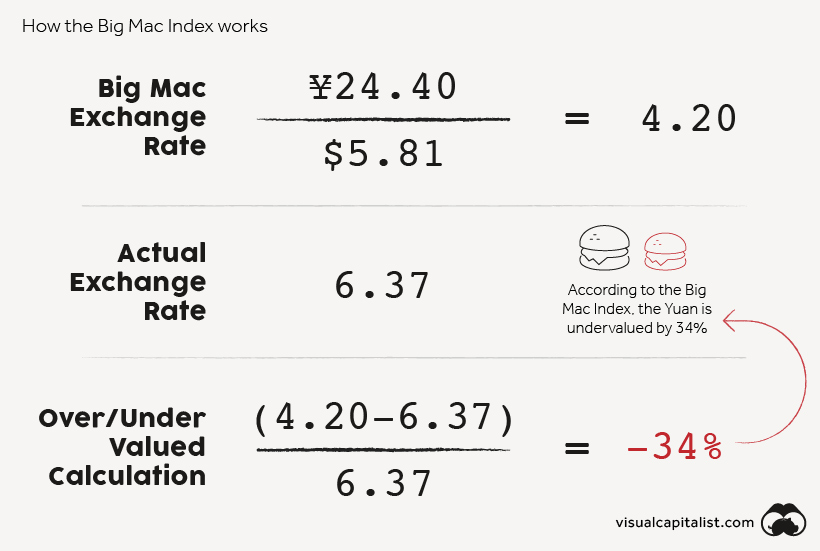

Using the price of a Big Mac in two countries, the index can give an indication as to whether a currency may be over or undervalued. For example, a Big Mac costs ¥24.40 in China and $5.81 in the United States. By comparing the implied exchange rate to the actual exchange rate, we can see whether the Yuan is over or undervalued.

According to the Big Mac Index, the Yuan is undervalued by 34%.

Beyond currency misalignment, the index has other uses. For instance, it shows inflation in burger prices over time. If we compare the price of a Big Mac across countries in the same currency—such as the U.S. dollar—we are also able to see where burgers are cheaper or relatively more expensive.

Burger Costs Around the World

In the animation, all Big Mac prices have been converted from local currency to U.S. dollars based on the actual exchange rate in effect at the time. Below, we show the change in price of a Big Mac in select countries, ordered by January 2022 prices.

| Country | May 2004 | January 2022 | % change |

|---|---|---|---|

| Switzerland | $4.88 | $6.98 | 43% |

| Norway | $5.18 | $6.39 | 23% |

| United States | $2.90 | $5.81 | 100% |

| Sweden | $3.94 | $5.79 | 47% |

| Israel | $2.79 | $5.35 | 92% |

| Canada | $2.33 | $5.32 | 129% |

| Venezuela | $1.48 | $5.06 | 243% |

| Euro area | $3.29 | $4.95 | 51% |

| Denmark | $4.46 | $4.82 | 8% |

| Britain | $3.37 | $4.82 | 43% |

| New Zealand | $2.65 | $4.60 | 73% |

| Australia | $2.27 | $4.51 | 98% |

| Singapore | $1.93 | $4.36 | 126% |

| Brazil | $1.70 | $4.31 | 154% |

| Argentina | $1.48 | $4.29 | 190% |

| Sri Lanka | $1.41 | $4.15 | 193% |

| Czech Republic | $2.13 | $4.11 | 93% |

| Chile | $2.18 | $3.88 | 78% |

| Thailand | $1.45 | $3.84 | 166% |

| China | $1.26 | $3.83 | 205% |

| South Korea | $2.72 | $3.82 | 40% |

| Poland | $1.63 | $3.44 | 111% |

| Japan | $2.32 | $3.38 | 46% |

| Peru | $2.58 | $3.36 | 31% |

| Mexico | $2.07 | $3.34 | 62% |

| Hungary | $2.51 | $3.09 | 23% |

| Hong Kong | $1.54 | $2.82 | 83% |

| Philippines | $1.23 | $2.79 | 126% |

| Taiwan | $2.25 | $2.70 | 20% |

| South Africa | $1.86 | $2.58 | 39% |

| Ukraine | $1.36 | $2.43 | 79% |

| Malaysia | $1.33 | $2.39 | 80% |

| Indonesia | $1.77 | $2.36 | 34% |

| Turkey | $2.58 | $1.86 | -28% |

| Russia | $1.45 | $1.74 | 20% |

Switzerland takes the cake for the priciest Big Mac, followed closely behind by Norway. Both countries have relatively high price levels but also enjoy higher wages when compared to other OECD countries.

Venezuela has seen the largest jump in burger prices, with the cost of a Big Mac climbing nearly 250% since 2004. The country has been plagued by hyperinflation for years, so it’s no surprise to see large price swings in the country’s data.

While it appears that the price of a Big Mac has decreased in Turkey, this is because the prices are shown in U.S. dollars. The new Turkish lira has depreciated against the U.S. dollar more than 90% since it was introduced in 2005.

Finally, it’s worth noting that Russia has the cheapest Big Mac, reflecting the country’s lower price levels. Labor costs in Russia are roughly a third of those in Switzerland.

The Limitations of Burgernomics

The Big Mac Index is useful for a number of reasons. Investors can use it to measure inflation over time, and compare this to official records. This can help them value bonds and other securities that are sensitive to inflation. The Big Mac Index also indicates whether a currency may be over or undervalued, and investors can place foreign exchange trades accordingly.

Of course, the index does have shortcomings. Here are some that economists have noted.

- Non-traded services can have different prices across countries. The price of a Big Mac will be influenced by the costs of things like labor, but this is not a reflection of relative currency values. The Economist now releases a GDP-adjusted version of the Big Mac Index to help address this criticism.

- McDonald’s is not in every country in the world. This means the geographic reach of the Big Mac Index has some limitations, particularly in Africa.

- The index lacks diversity. The index is made up of one item: the Big Mac. Because of this, it lacks the diversity of other economic metrics such as the Consumer Price Index.

Despite all of these limitations, the Big Mac Index does act as a good starting place for understanding purchasing power parity. Through the simplicity of burgers, complex economic theory is easier to digest.

This article was published as a part of Visual Capitalist's Creator Program, which features data-driven visuals from some of our favorite Creators around the world.

Money

Charted: Who Has Savings in This Economy?

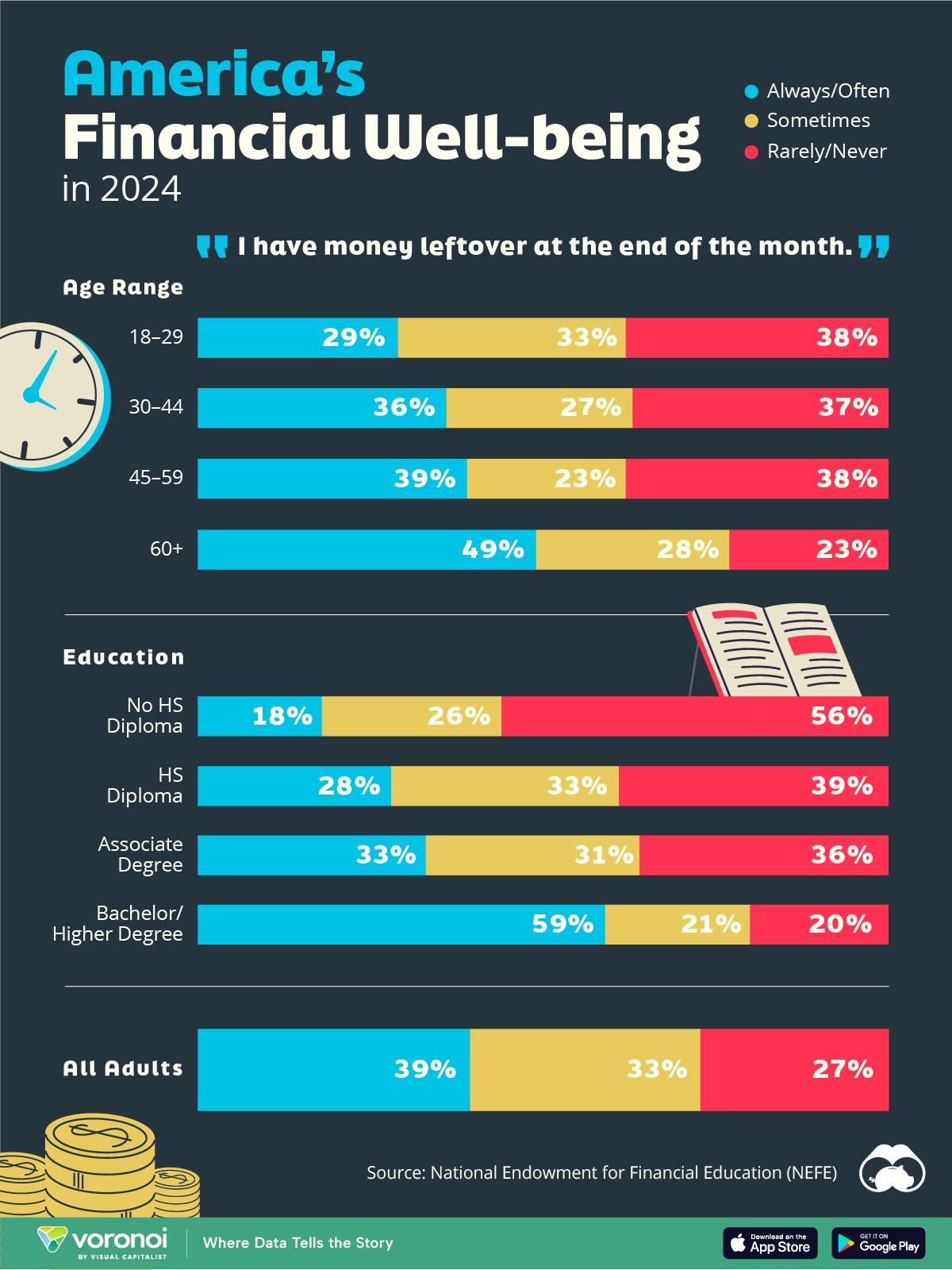

Older, better-educated adults are winning the savings game, reveals a January survey by the National Opinion Research Center at the University of Chicago.

Who Has Savings in This Economy?

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Two full years of inflation have taken their toll on American households. In 2023, the country’s collective credit card debt crossed $1 trillion for the first time. So who is managing to save money in the current economic environment?

We visualize the percentage of respondents to the statement “I have money leftover at the end of the month” categorized by age and education qualifications. Data is sourced from a National Endowment for Financial Education (NEFE) report, published last month.

The survey for NEFE was conducted from January 12-14, 2024, by the National Opinion Research Center at the University of Chicago. It involved 1,222 adults aged 18+ and aimed to be representative of the U.S. population.

Older Americans Save More Than Their Younger Counterparts

General trends from this dataset indicate that as respondents get older, a higher percentage of them are able to save.

| Age | Always/Often | Sometimes | Rarely/Never |

|---|---|---|---|

| 18–29 | 29% | 33% | 38% |

| 30–44 | 36% | 27% | 37% |

| 45–59 | 39% | 23% | 38% |

| Above 60 | 49% | 28% | 23% |

| All Adults | 39% | 33% | 27% |

Note: Percentages are rounded and may not sum to 100.

Perhaps not surprisingly, those aged 60+ are the age group with the highest percentage saying they have leftover money at the end of the month. This age group spent the most time making peak earnings in their careers, are more likely to have investments, and are more likely to have paid off major expenses like a mortgage or raising a family.

The Impact of Higher Education on Earnings and Savings

Based on this survey, higher education dramatically improves one’s ability to save. Shown in the table below, those with a bachelor’s degree or higher are three times more likely to have leftover money than those without a high school diploma.

| Education | Always/Often | Sometimes | Rarely/Never |

|---|---|---|---|

| No HS Diploma | 18% | 26% | 56% |

| HS Diploma | 28% | 33% | 39% |

| Associate Degree | 33% | 31% | 36% |

| Bachelor/Higher Degree | 59% | 21% | 20% |

| All Adults | 39% | 33% | 27% |

Note: Percentages are rounded and may not sum to 100.

As the Bureau of Labor Statistics notes, earnings improve with every level of education completed.

For example, those with a high school diploma made 25% more than those without in 2022. And as the qualifications increase, the effects keep stacking.

Meanwhile, a Federal Reserve study also found that those with more education tended to make financial decisions that contributed to building wealth, of which the first step is to save.

-

Markets1 week ago

Markets1 week agoU.S. Debt Interest Payments Reach $1 Trillion

-

Business2 weeks ago

Business2 weeks agoCharted: Big Four Market Share by S&P 500 Audits

-

Real Estate2 weeks ago

Real Estate2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Demographics2 weeks ago

Demographics2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023