Capturing the Renewable Energy Shift

The following content is sponsored by eToro

Capturing The Renewable Energy Shift

As the impacts of climate change and the importance of decarbonization have started to become clear, it’s hard to ignore the ongoing shift towards embracing renewables.

Today, the renewables energy market has already become the energy industry’s biggest driver of growth, and both governments and businesses have been pressed to solidify their commitments to green energy.

This infographic from eToro highlights the many developments propelling the shift towards renewable energy, and shines a spotlight on what investors should expect in the market.

Renewable Energy’s Growing Market Presence

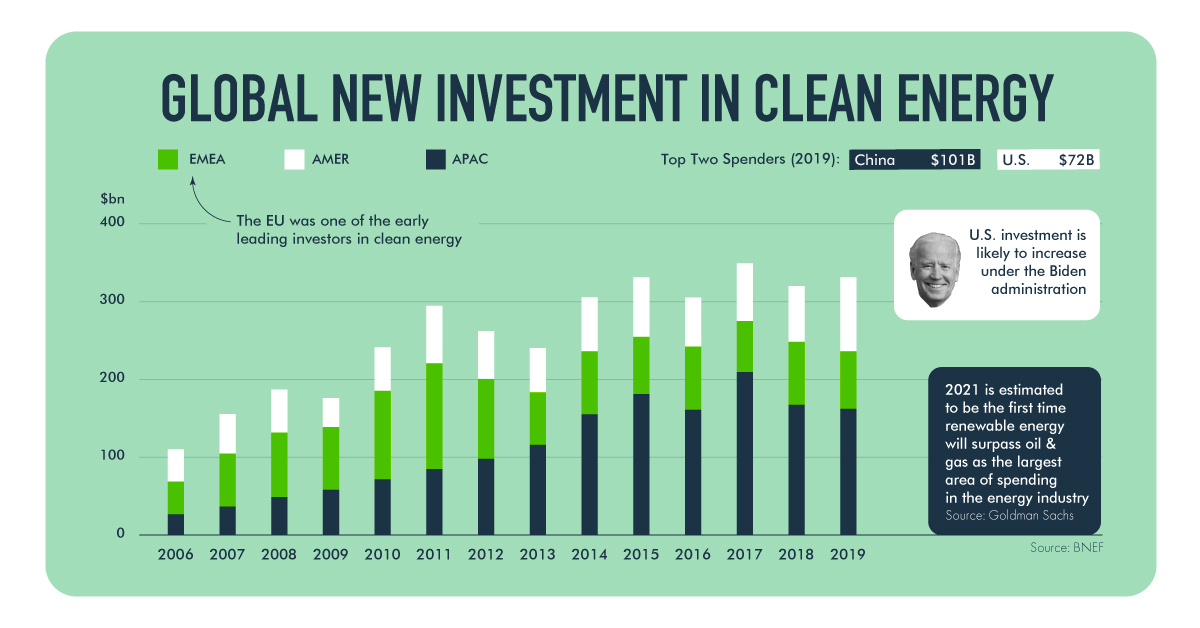

Investments in clean energy have been growing both quickly and consistently.

Before 2010, annual global investment in clean energy climbed from just tens of billions to $177 billion in 2009. But in the following decade, annual investment in renewables regularly surpassed $200 billion, reaching $303.5 billion in 2020.

Early spending in the field was led by the EU, but recently China and the U.S. have become the world’s largest spenders in clean energy.

As interest in renewables has grown, so has the sector’s impact on capital markets. Of the 174 announced M&A deals in the U.S. power and utilities industry slated for 2021, 83% involve renewables.

Combined with increasing pressure from shareholders of public companies (and especially energy producers) for climate-related resolutions, 2021 is expected to be the first time renewable energy surpasses oil & gas as the energy industry’s largest area of spending.

At the same time, governments are feeling pressured to commit to the Paris climate accords beyond mere statements, with many countries signing net-zero emission laws.

| Country | Net-Zero Emissions Target Year |

|---|---|

| Sweden | 2045 |

| Denmark | 2050 |

| France | 2050 |

| Hungary | 2050 |

| Germany | 2050 |

| New Zealand | 2050 |

| Spain | 2050 |

| U.K. | 2050 |

Wind and Solar Lead The Renewable Energy Shift

Knowing where the shift towards clean energy is happening is equally as important.

Early investments in clean energy transitions were spread out across many promising sectors, including hydro, nuclear, and carbon-capture for fossil fuel production. But over the past 10 years, wind and solar energy have been leading the charge.

Levelised costs for solar electricity are already estimated as lower than gas or coal as of 2020, thanks to rapidly dropping output costs.

| Electricity Source | Estimated Levelised Cost per MWh (2019) |

|---|---|

| Solar PV (China & India) | $20-$40 |

Solar PV (U.S. & Europe) | $30-$60 |

| Gas | $50-$90 |

| Coal | $50-$120 |

In terms of capacity, the global installation of wind and solar has already eclipsed hydro electricity, and is expected to pass both gas and coal by 2024.

Expected increases in renewable energy capacity are estimated to almost match the increasing global demand for energy. However, much of that demand is still expected to be met by fossil fuels, especially for regions with massive, scalable demand.

But as the renewable energy shift continues to pressure greater adoption of clean energy measures, further investment in renewable production and cost cutting, the market demand is expected to shift to green as well.

How Can Investors Take Part?

eToro’s RenewableEnergy CopyPortfolio* gives investors direct access to the valuable renewable energy market.

Curated by experienced and proven investment teams, the thematic portfolio offers exposure to both veteran companies and up-and-coming pioneers in the renewable energy space, with no management fees.

*Your capital is at risk.

CopyPortfolios is a portfolio management product, provided by eToro Europe Ltd., which is authorised and regulated by the Cyprus Securities and Exchange Commission.

CopyPortfolios should not be considered as exchange traded funds, nor as hedge funds.

-

Sponsored3 years ago

Sponsored3 years agoMore Than Precious: Silver’s Role in the New Energy Era (Part 3 of 3)

Long known as a precious metal, silver in solar and EV technologies will redefine its role and importance to a greener economy.

-

Sponsored7 years ago

Sponsored7 years agoThe History and Evolution of the Video Games Market

Everything from Pong to the rise of mobile gaming and AR/VR. Learn about the $100 billion video games market in this giant infographic.

-

Sponsored8 years ago

Sponsored8 years agoThe Extraordinary Raw Materials in an iPhone 6s

Over 700 million iPhones have now been sold, but the iPhone would not exist if it were not for the raw materials that make the technology...

-

Sponsored8 years ago

Sponsored8 years agoThe Industrial Internet, and How It’s Revolutionizing Mining

The convergence of the global industrial sector with big data and the internet of things, or the Industrial Internet, will revolutionize how mining works.