Markets

A Tale of Two Banking Sectors: Canada vs. U.S.

A Tale of Two Banking Sectors: Canada vs. U.S.

Regardless of which side of the 49th parallel you are on, banking sectors play a crucial role in both the financial system and the economy.

But while banks on each side of the border perform many similar functions, and have comparable economic impacts, the fact is that the U.S. and Canadian banking systems are very different.

Comparing Canadian and U.S. Banks

Today’s infographic comes to us from RBC Global Asset Management and it compares Canadian and U.S. banks directly based on a variety of factors.

The histories of both banking sectors are contrasted, but subjects such as the regulatory environments, market forces, the number and size of banks, and post-crisis landscapes are also compared. An outlook for investors on both sectors is also provided.

The end result is an interesting depiction of two banking sectors that are related in many ways, but that also have distinct differences and ways of doing business.

General Differences:

Historically, the Canadian banking system favors a limited quantity of banks, and many branches. It also carries the British influence of valuing stability over experimentation. Meanwhile, U.S. banking is more decentralized and localized, and more open to experimentation. This has led to trial and error, but also the world’s largest bank system.

Regulatory Focuses

Canada’s banking system tends to promote safety and soundness, while the American system keys in on privacy, anti-money laundering, banking access, and consumer protection measures.

Market Environment

The Canadian market is worth C$142 billion (US$111 billion) per year, while the U.S. market is over 10x bigger at US$1.4 trillion. Interestingly, these market sizes explain why Canadian banks often seek growth opportunities in the U.S. market, while U.S. banks just focus on the massive domestic sector for growth.

Number of Banks

There are 85 banks in Canada, and 4,938 in the United States.

Market Share

Canada’s five biggest banks hold a whopping 89% of market share, while America’s five biggest banks only hold 35% of market share.

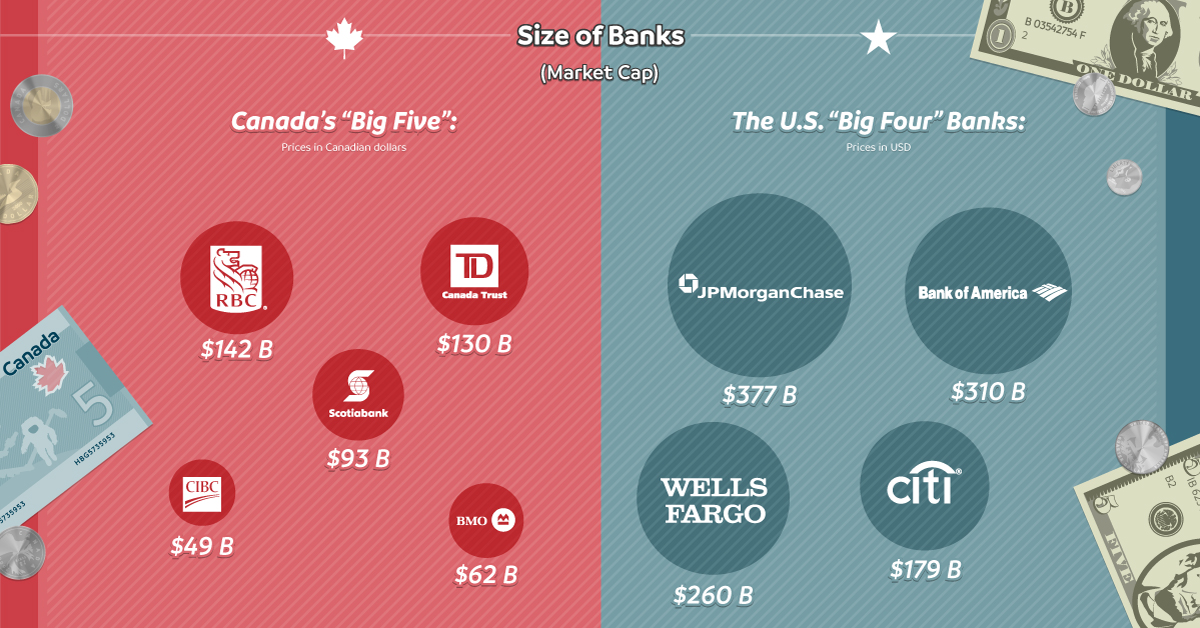

Biggest Banks

Canada’s “Big Five” Banks:

RBC: C$142 billion

TD: C$130 billion

Scotia: C$93 billion

BMO: C$62 billion

CIBC: C$49 billion

The Biggest Four Banks in the U.S.:

JPMorgan Chase: US$377 billion

Bank of America: US$310 billion

Wells Fargo: US$260 billion

Citigroup: US$179 billion

In Canada, there are no other institutions worth over C$25 billion, but in the States there are eight that are worth between US$50-$100 billion.

Outlook for Investors

Not only are the two banking environments quite different in terms of character – but Canadian and U.S. banks are at different points in their market cycles, as well.

Post-2008 Reaction

Banks in Canada were minimally impacted by the Financial Crisis, and have been permitted to use lower risk weights than U.S. Banks. As a result, they’ve been able to hold less capital for each loan (i.e. higher leverage)

Banks in the U.S. have spent the past number of years building capital. Regulators required U.S. banks to be conservative in their approach post-crisis. As a result, U.S. banks have lower leverage than Canadian peers.

Leverage (Asset/Equity)

Canada’s “Big Five”:

18.3

Five Biggest U.S. Banks:

9.3

Dividend Yield

Canadian Banks: 3.9%

S&P/TSX Composite: 2.9%

Top 15 U.S. Banks: 2.5%

S&P 500: 2.1%

Which Sector Should Investors Choose?

There are compelling reasons to consider the financial institutions of either country:

Canada

- Canadian banks have a proven track-record of delivering steady dividends that have grown over time.

- Canadian banks have a strong global reputation for reliability and safety due to Canada’s sound regulatory framework and their relatively risk-averse approach.

- Canadian bank stocks can also be a good source of consistent income, with dividends that pay higher than the market. Canadians also doubly benefit, since to the Canadian dividend tax credit.

United States

- U.S. banks have significantly improved their balance sheets and capital structure over the past decade to be better positioned for future market cycles.

- Stronger U.S. economic growth combined with changing monetary policy creates a positive environment for U.S. banks to benefit from increased business and consumer demand and wider interest rate spreads.

- Recent tax cuts and deregulation are likely to benefit U.S. banks, as savings stand to contribute to earnings per share, and potentially lead to higher dividend payouts along with share buybacks.

Canadian and U.S. banks are similar in many ways – but their differing histories, competitive frameworks, and economic environments each provide unique exposure for investors.

Economy

Economic Growth Forecasts for G7 and BRICS Countries in 2024

The IMF has released its economic growth forecasts for 2024. How do the G7 and BRICS countries compare?

G7 & BRICS Real GDP Growth Forecasts for 2024

The International Monetary Fund’s (IMF) has released its real gross domestic product (GDP) growth forecasts for 2024, and while global growth is projected to stay steady at 3.2%, various major nations are seeing declining forecasts.

This chart visualizes the 2024 real GDP growth forecasts using data from the IMF’s 2024 World Economic Outlook for G7 and BRICS member nations along with Saudi Arabia, which is still considering an invitation to join the bloc.

Get the Key Insights of the IMF’s World Economic Outlook

Want a visual breakdown of the insights from the IMF’s 2024 World Economic Outlook report?

This visual is part of a special dispatch of the key takeaways exclusively for VC+ members.

Get the full dispatch of charts by signing up to VC+.

Mixed Economic Growth Prospects for Major Nations in 2024

Economic growth projections by the IMF for major nations are mixed, with the majority of G7 and BRICS countries forecasted to have slower growth in 2024 compared to 2023.

Only three BRICS-invited or member countries, Saudi Arabia, the UAE, and South Africa, have higher projected real GDP growth rates in 2024 than last year.

| Group | Country | Real GDP Growth (2023) | Real GDP Growth (2024P) |

|---|---|---|---|

| G7 | 🇺🇸 U.S. | 2.5% | 2.7% |

| G7 | 🇨🇦 Canada | 1.1% | 1.2% |

| G7 | 🇯🇵 Japan | 1.9% | 0.9% |

| G7 | 🇫🇷 France | 0.9% | 0.7% |

| G7 | 🇮🇹 Italy | 0.9% | 0.7% |

| G7 | 🇬🇧 UK | 0.1% | 0.5% |

| G7 | 🇩🇪 Germany | -0.3% | 0.2% |

| BRICS | 🇮🇳 India | 7.8% | 6.8% |

| BRICS | 🇨🇳 China | 5.2% | 4.6% |

| BRICS | 🇦🇪 UAE | 3.4% | 3.5% |

| BRICS | 🇮🇷 Iran | 4.7% | 3.3% |

| BRICS | 🇷🇺 Russia | 3.6% | 3.2% |

| BRICS | 🇪🇬 Egypt | 3.8% | 3.0% |

| BRICS-invited | 🇸🇦 Saudi Arabia | -0.8% | 2.6% |

| BRICS | 🇧🇷 Brazil | 2.9% | 2.2% |

| BRICS | 🇿🇦 South Africa | 0.6% | 0.9% |

| BRICS | 🇪🇹 Ethiopia | 7.2% | 6.2% |

| 🌍 World | 3.2% | 3.2% |

China and India are forecasted to maintain relatively high growth rates in 2024 at 4.6% and 6.8% respectively, but compared to the previous year, China is growing 0.6 percentage points slower while India is an entire percentage point slower.

On the other hand, four G7 nations are set to grow faster than last year, which includes Germany making its comeback from its negative real GDP growth of -0.3% in 2023.

Faster Growth for BRICS than G7 Nations

Despite mostly lower growth forecasts in 2024 compared to 2023, BRICS nations still have a significantly higher average growth forecast at 3.6% compared to the G7 average of 1%.

While the G7 countries’ combined GDP is around $15 trillion greater than the BRICS nations, with continued higher growth rates and the potential to add more members, BRICS looks likely to overtake the G7 in economic size within two decades.

BRICS Expansion Stutters Before October 2024 Summit

BRICS’ recent expansion has stuttered slightly, as Argentina’s newly-elected president Javier Milei declined its invitation and Saudi Arabia clarified that the country is still considering its invitation and has not joined BRICS yet.

Even with these initial growing pains, South Africa’s Foreign Minister Naledi Pandor told reporters in February that 34 different countries have submitted applications to join the growing BRICS bloc.

Any changes to the group are likely to be announced leading up to or at the 2024 BRICS summit which takes place October 22-24 in Kazan, Russia.

Get the Full Analysis of the IMF’s Outlook on VC+

This visual is part of an exclusive special dispatch for VC+ members which breaks down the key takeaways from the IMF’s 2024 World Economic Outlook.

For the full set of charts and analysis, sign up for VC+.

-

Markets1 week ago

Markets1 week agoU.S. Debt Interest Payments Reach $1 Trillion

-

Markets2 weeks ago

Markets2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Demographics2 weeks ago

Demographics2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Money2 weeks ago

Money2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries