Cryptocurrency

The Blockchain Could Change the Backbone of the Stock Market

Modern technology enables stock markets to be faster and more complex than ever.

But while the speed of order executions are infinitely more impressive across the board, the conceptual backbone behind the stock market itself hasn’t changed much. In fact, the model we use today for settling trades and ensuring proper share ownership is still based on the one initially created in the 17th Century.

A Decentralization of Equities?

Today’s infographic comes to us from Equibit, and it envisions what a decentralized securities platform could look like.

In such a paradigm, the settlement of trades would not occur through centralized transfer agents, but instead through a blockchain with this feature “built in”.

The application of blockchain technology could take the modernization of the stock market one step further. Instead of technology being used simply to speed up more complex transactions, the blockchain could change how the plumbing behind the system works to mitigate current risks and problems.

But to understand how transformative this idea is, we need to look at the history behind the current model first.

The Roots of the Modern Market

The roots of the modern stock market can be traced back to Amsterdam in the year 1602, when the Dutch East India Company became the world’s first “publicly traded” company.

Trade missions to the West Indies were risky and expensive – so shares and bonds in the company were initially sold to a large pool of interested investors to spread the risk. In turn, backers of the company received a guarantee of some future share of profits.

As investors began speculating about the prospects of the Dutch East India Company, a secondary market quickly developed for these securities. People bought and sold stock in high volumes, and a central registrar tracked the transfer of shares between parties.

The Backbone of Today’s Market

Over 400 years later, the stock market is not that much different from the earliest exchange found in Amsterdam.

Modern computing and the internet have sped up transactions so they can be executed in milliseconds, but the conceptual backbone of the market hasn’t changed at all.

Stock Transfer Agents are the centralized registrars in the background that track share ownership for issuers and the stock market. They are a third party that will cancel the share certificate for the investor that sold the shares, and substitute the new owner’s name on the official master shareholder listing.

There are over 130 stock transfer agents in the USA and Canada, maintaining the records of more than 100 million shareholders on behalf of over 15,000 issuers.

New Technology, Old Model

While modern stock transfer agents use today’s technology, the same old model persists – and it creates multiple industry problems:

Centralized and expensive

- Depositories and transfer agents are a single point of failure

- Registration, transfer, distribution, scrutineering, courier fees

- The more widely held, the higher the administration costs

Limited Transparency

- Information asymmetry leads to market advantages

- Forged securities still a concern

- Counterparty risk is systemic

Furthermore, legal ownership rests with transfer agents in most jurisdictions. Investors actually do not have title.

At the same time, the industry is huge – just one company, The Depository Trust & Clearing Corporation (DTCC) is the highest financial value processor in the world with $1.6 quadrillion in transactions in 2016.

The Problem With Centralization

During the Financial Crisis, the problems of increased centralization and limited transparency reared their ugly head.

Companies like Lehman Brothers and MF Global self-destructed – and nobody knew what kind of assets they had off their balance sheets.

If an accurate [blockchain] record of all of Lehman’s transactions had been available in 2008, then Lehman’s prudential regulators could have used data mining tools, smart contracts and other analytical applications to recognize anomalies. Regulators could have reacted sooner to Lehman’s deteriorating creditworthiness.

– J. Christopher Giancarlo, Commodity Futures Trading Commission

This lack of clarity and risk helped drive hysteria, ultimately exacerbating the extent of the crisis. Because no one could quantify the risks, investors liquidated their assets. More selling meant even less liquidity.

Enter the Blockchain

Instead of putting all stock transactions through a centralized hub, the blockchain can be used to directly transfer share ownership between investors.

Here’s how a decentralized securities platform could work:

- Somebody decides to transfer a security.

- The transaction is broadcast to a P2P network consisting of computers known as nodes.

- The network of nodes validates the transaction and user’s status using known algorithms. A valid transaction will transfer the title of the security.

- Once verified, the transaction is combined with other transactions to create a new block of data for the ledger and thus completing the transaction.

In other words, stock exchanges could run using a blockchain under the hood, with no longer any need for a centralized settlement or transfer of share certificates.

This is cheaper, faster, reduces risks, and more secure. It also would be fully transparent.

Even better, such a platform could also serve as the base for other value adds – and fully transform the way we think about equity markets.

Technology

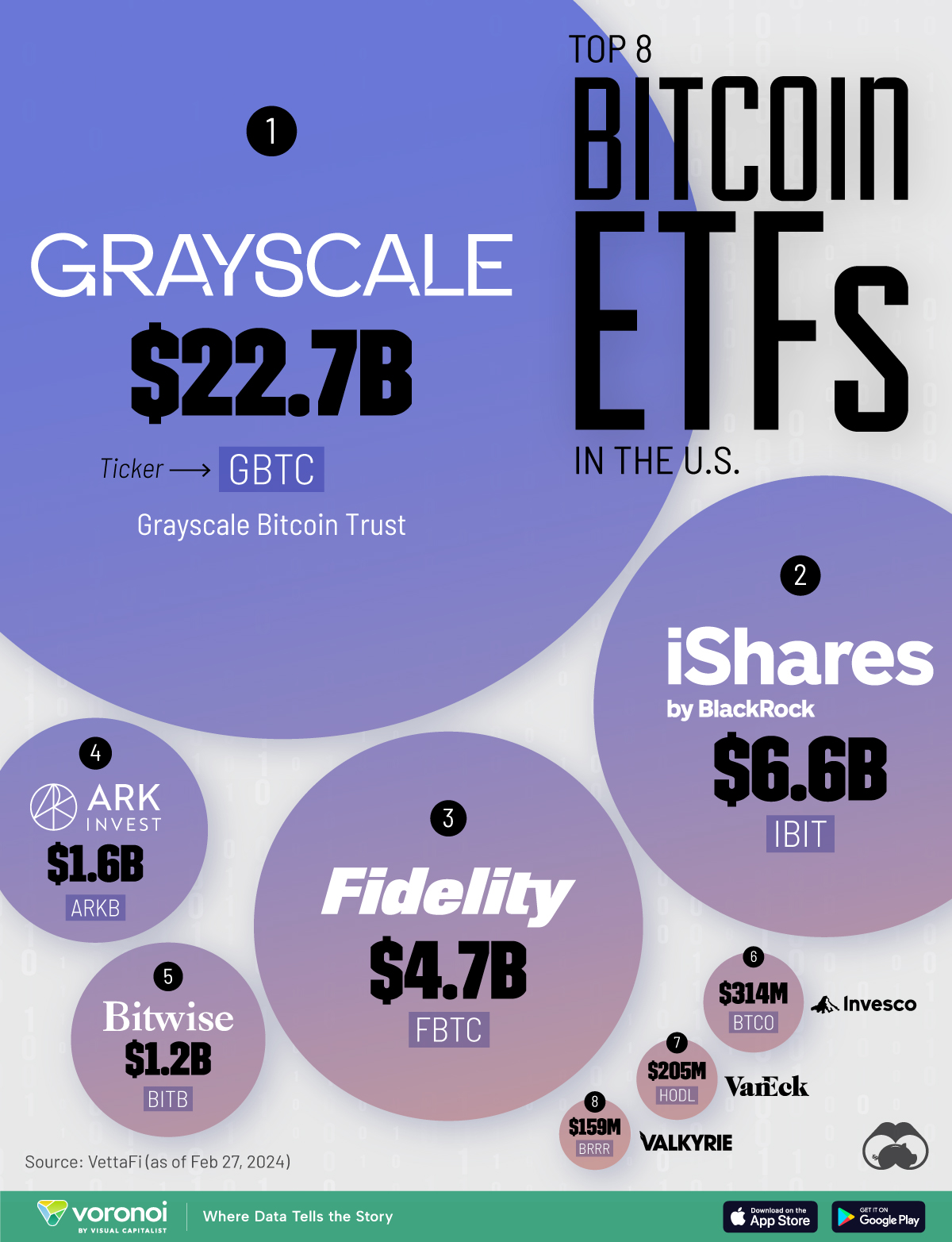

Ranked: The Largest Bitcoin ETFs in the U.S.

In this graphic, we rank the top eight Bitcoin ETFs in the U.S. by their total assets under management (AUM).

Ranking the Largest Bitcoin ETFs in the U.S.

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

In early January 2024, the U.S. Securities and Exchange Commission (U.S. SEC) gave its approval on exchange-traded funds (ETFs) to track Bitcoin, giving investors an alternative pathway to accessing the world’s biggest cryptocurrency.

In this graphic, we’ve shown the eight largest Bitcoin ETFs in the U.S. by assets under management (AUM), as of Feb. 27, 2024. To elaborate, these are ETFs that buy and hold actual Bitcoin, meaning their performance will generally follow that of Bitcoin itself.

The data used to create this graphic was sourced from VettaFi.

| ETF Name | Ticker | AUM |

|---|---|---|

| Grayscale Bitcoin Trust | GBTC | $22.7B |

| iShares Bitcoin Trust Registered | IBIT | $6.6B |

| Fidelity Wise Origin Bitcoin Fund | FBTC | $4.7B |

| ARK 21Shares Bitcoin ETF | ARKB | $1.6B |

| Bitwise Bitcoin ETF Trust | BITB | $1.2B |

| Invesco Galaxy Bitcoin ETF | BTCO | $314M |

| VanEck Bitcoin Trust | HODL | $205M |

| Valkyrie Bitcoin Fund | BRRR | $159M |

From these numbers we can see that Grayscale’s Bitcoin Trust (GBTC) is the largest by a wide margin. As its name implies, GBTC was originally structured as a trust, but was converted to an ETF on Jan. 11, 2024.

Why Buy a Bitcoin ETF?

Bitcoin ETFs simplify the process of buying and storing Bitcoin. This is because they can be purchased within a traditional brokerage account, just like any other ETF or stock.

Instead of having to think about creating a wallet, memorizing a 12-word seed phrase and holding their keys, this product scraps all of that and provides a well-known path: buy an ETF. This will open the digital asset space to a broader investor base.

Rita Martins, former Head of FinTech Partnerships, HSBC

Investors should be aware that these ETFs charge an expense ratio, which could eat into returns. Information on fees can be easily found on each asset manager’s relevant fund page.

For more visualizations related to Bitcoin, consider this graphic which shows how Bitcoin has performed relative to other major asset classes over the past 10 years.

-

Green1 week ago

Green1 week agoRanked: The Countries With the Most Air Pollution in 2023

-

Misc2 weeks ago

Misc2 weeks agoAlmost Every EV Stock is Down After Q1 2024

-

AI2 weeks ago

AI2 weeks agoThe Stock Performance of U.S. Chipmakers So Far in 2024

-

Markets2 weeks ago

Markets2 weeks agoCharted: Big Four Market Share by S&P 500 Audits

-

Real Estate2 weeks ago

Real Estate2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Travel2 weeks ago

Travel2 weeks agoRanked: The World’s Top Flight Routes, by Revenue