Markets

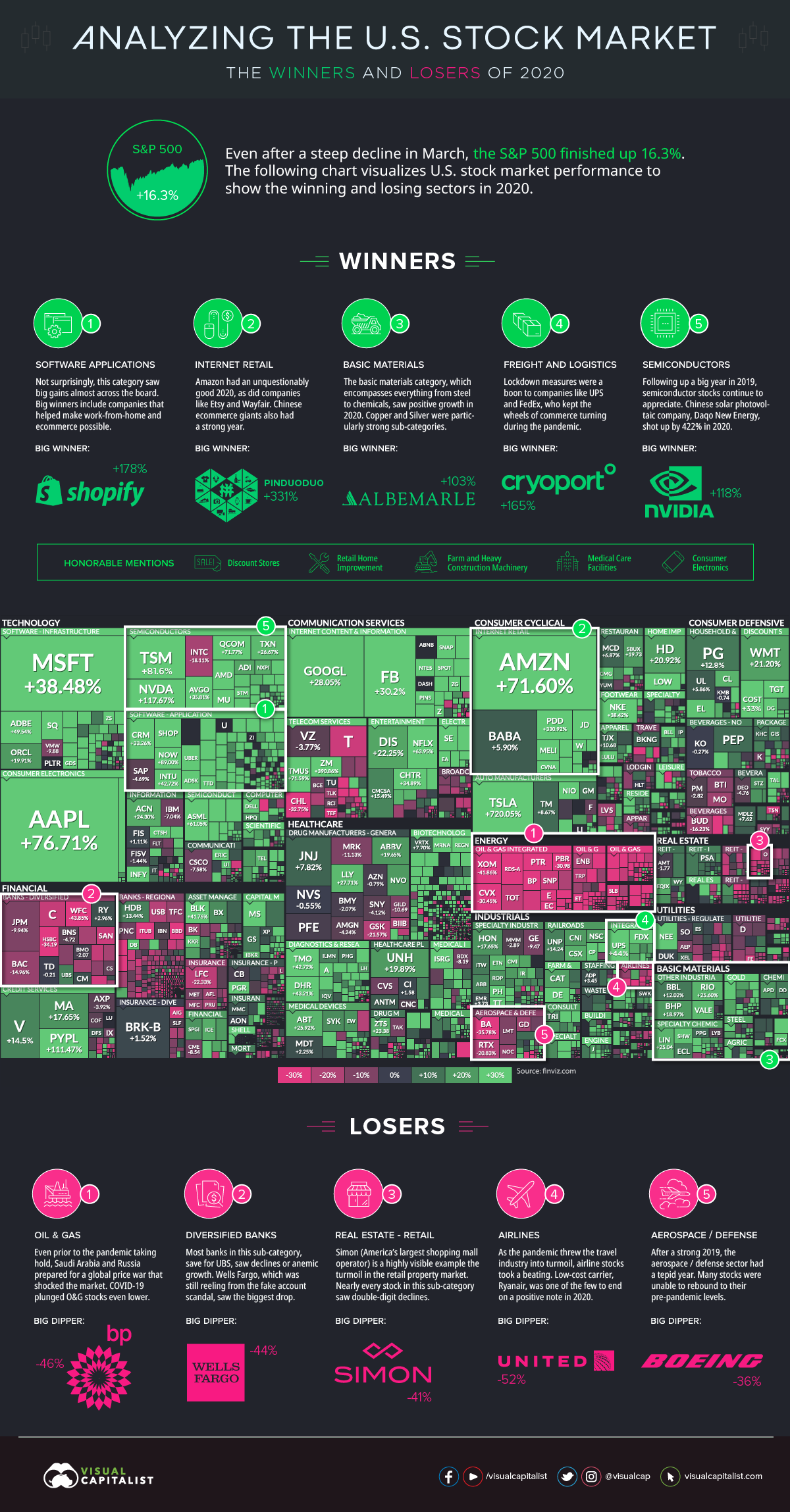

The Best and Worst Performing Sectors of 2020

The Best and Worst Performing Sectors of 2020

To say that 2020 was an unusual year in markets would be a vast understatement.

In 2020, we saw the quickest and deepest bear market decline in history, trillions of dollars of global stimulus, the highest volatility (VIX) on record, negative oil prices, and the fastest recovery from a bear market ever—just to name a few of the abnormalities.

And while the broader economy is still in a state of repair, investors finished the year in the black. The S&P 500, for example, ended with 16.3% gains, which was an above-average outing for the benchmark index.

Winners and Losing Sectors of 2020

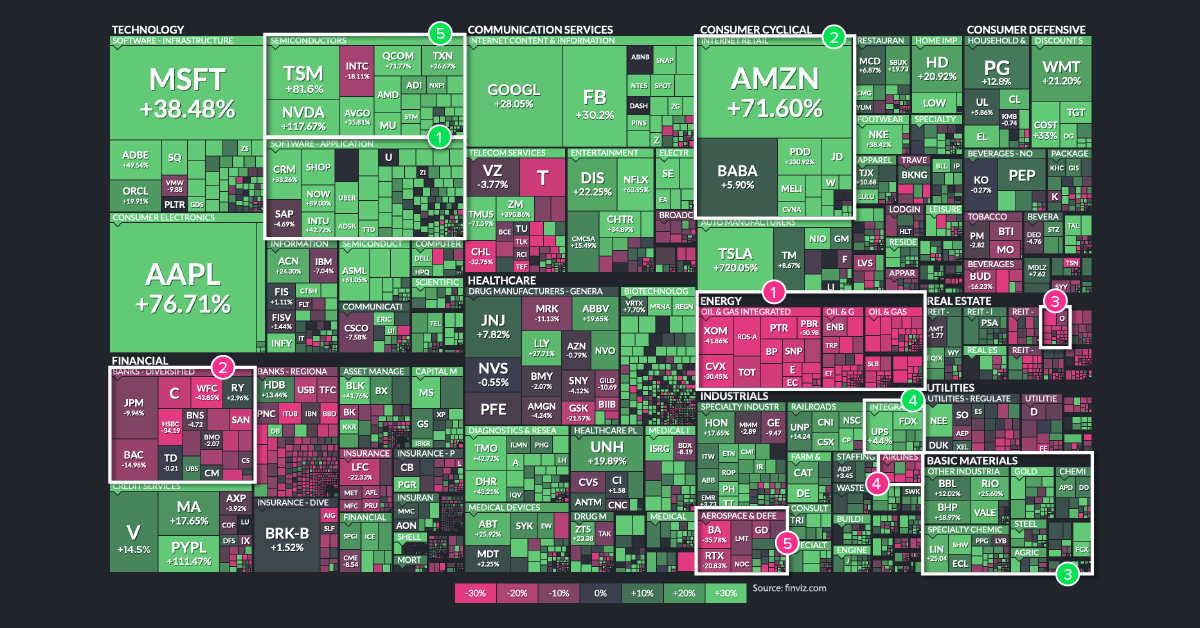

Today’s visualization uses an augmented screenshot of the FinViz treemap, showing the final numbers posted for major U.S.-listed companies, sorted by sector and industry.

As you can see, the best and worst performing sectors generally fall into two categories: those that benefitted from COVID-19, and those that didn’t.

This massive divergence is evident in the numbers. Companies in winning sectors are often up double or triple digits—while their losing counterparts were often down double digits, sometimes even halving in value from how they started the year.

The Winners

1. Software Applications

It was another banner year for Big Tech, but some of the top performing companies were those that acted as enablers to remote working and ecommerce. Perhaps the most notable entry here is Shopify, which rose 178% on the year and is nearly a $150 billion company today.

2. Internet Retail

While Amazon is the undisputed 800-pound gorilla in ecommerce, companies like Etsy and Wayfair also had incredible years—as did many internet retail plays on the opposite side of the Pacific. Chinese company Pinduoduo, described as the fastest growing tech company in the world, gained 331% on the year as it capitalized on emerging trends such as social ecommerce, team purchasing, and consumer-to-manufacturing (C2M) sales.

3. Basic Materials

It’s been a long downtrend in the commodity super cycle, but materials have come back into vogue. Copper prices are at eight-year highs, and gold hit all-time highs in August 2020. Some companies, such as Albemarle—the largest supplier of lithium for electric vehicles—doubled their stock price over the course of the year.

4. Freight and Logistics

The shift to ecommerce has come faster than anticipated, and companies like FedEx and UPS couldn’t be happier. And with the transportation of ultra-refrigerated vaccines lining up to be a key need of 2021, it’s no surprise to see Cryoport up 165% on the year.

5. Semiconductors

For a second straight year, semiconductor companies finished as winners on our list. The world needs more hardware to house and process the ever-expanding datasphere, and companies like Nvidia showed triple-digit gains in 2020, up 117%.

Honorable mentions: Discount stores, retail home improvement, farm and heavy construction machinery, medical care facilities, and consumer electronics

The Losers

1. Oil and Gas

The oil sector was already struggling pre-COVID with price wars and a supply glut, but then lockdowns and the shutdown of non-essential travel provided another blow. BP finished the year at nearly half its market capitalization, falling 46% on the year.

2. Diversified Banks

With record-low interest rates, shuttered physical locations, and credit risks looming from unemployed borrowers, bank stocks struggled in 2020. Wells Fargo, for example, finished down the year 44%.

3. Real Estate – Retail

Many malls have not been collecting rent checks from their tenants, creating a challenging environment for many property owners and managers. Simon, the country’s largest shopping mall operator, felt the pain as its stock dropped 41% in 2020.

4. Airlines

It goes without saying that less flying means less revenue for airlines. But going forward, with web conferencing now the professional norm, it’s also expected that lucrative business passenger numbers will take a hit in the future. United Airlines finished the year at less than half their market capitalization (-54%).

5. Aerospace/Defense

Many aerospace and defense stocks were unable to rebound to pre-pandemic levels. Boeing, for example, finished the year down 36%.

Markets

U.S. Debt Interest Payments Reach $1 Trillion

U.S. debt interest payments have surged past the $1 trillion dollar mark, amid high interest rates and an ever-expanding debt burden.

U.S. Debt Interest Payments Reach $1 Trillion

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

The cost of paying for America’s national debt crossed the $1 trillion dollar mark in 2023, driven by high interest rates and a record $34 trillion mountain of debt.

Over the last decade, U.S. debt interest payments have more than doubled amid vast government spending during the pandemic crisis. As debt payments continue to soar, the Congressional Budget Office (CBO) reported that debt servicing costs surpassed defense spending for the first time ever this year.

This graphic shows the sharp rise in U.S. debt payments, based on data from the Federal Reserve.

A $1 Trillion Interest Bill, and Growing

Below, we show how U.S. debt interest payments have risen at a faster pace than at another time in modern history:

| Date | Interest Payments | U.S. National Debt |

|---|---|---|

| 2023 | $1.0T | $34.0T |

| 2022 | $830B | $31.4T |

| 2021 | $612B | $29.6T |

| 2020 | $518B | $27.7T |

| 2019 | $564B | $23.2T |

| 2018 | $571B | $22.0T |

| 2017 | $493B | $20.5T |

| 2016 | $460B | $20.0T |

| 2015 | $435B | $18.9T |

| 2014 | $442B | $18.1T |

| 2013 | $425B | $17.2T |

| 2012 | $417B | $16.4T |

| 2011 | $433B | $15.2T |

| 2010 | $400B | $14.0T |

| 2009 | $354B | $12.3T |

| 2008 | $380B | $10.7T |

| 2007 | $414B | $9.2T |

| 2006 | $387B | $8.7T |

| 2005 | $355B | $8.2T |

| 2004 | $318B | $7.6T |

| 2003 | $294B | $7.0T |

| 2002 | $298B | $6.4T |

| 2001 | $318B | $5.9T |

| 2000 | $353B | $5.7T |

| 1999 | $353B | $5.8T |

| 1998 | $360B | $5.6T |

| 1997 | $368B | $5.5T |

| 1996 | $362B | $5.3T |

| 1995 | $357B | $5.0T |

| 1994 | $334B | $4.8T |

| 1993 | $311B | $4.5T |

| 1992 | $306B | $4.2T |

| 1991 | $308B | $3.8T |

| 1990 | $298B | $3.4T |

| 1989 | $275B | $3.0T |

| 1988 | $254B | $2.7T |

| 1987 | $240B | $2.4T |

| 1986 | $225B | $2.2T |

| 1985 | $219B | $1.9T |

| 1984 | $205B | $1.7T |

| 1983 | $176B | $1.4T |

| 1982 | $157B | $1.2T |

| 1981 | $142B | $1.0T |

| 1980 | $113B | $930.2B |

| 1979 | $96B | $845.1B |

| 1978 | $84B | $789.2B |

| 1977 | $69B | $718.9B |

| 1976 | $61B | $653.5B |

| 1975 | $55B | $576.6B |

| 1974 | $50B | $492.7B |

| 1973 | $45B | $469.1B |

| 1972 | $39B | $448.5B |

| 1971 | $36B | $424.1B |

| 1970 | $35B | $389.2B |

| 1969 | $30B | $368.2B |

| 1968 | $25B | $358.0B |

| 1967 | $23B | $344.7B |

| 1966 | $21B | $329.3B |

Interest payments represent seasonally adjusted annual rate at the end of Q4.

At current rates, the U.S. national debt is growing by a remarkable $1 trillion about every 100 days, equal to roughly $3.6 trillion per year.

As the national debt has ballooned, debt payments even exceeded Medicaid outlays in 2023—one of the government’s largest expenditures. On average, the U.S. spent more than $2 billion per day on interest costs last year. Going further, the U.S. government is projected to spend a historic $12.4 trillion on interest payments over the next decade, averaging about $37,100 per American.

Exacerbating matters is that the U.S. is running a steep deficit, which stood at $1.1 trillion for the first six months of fiscal 2024. This has accelerated due to the 43% increase in debt servicing costs along with a $31 billion dollar increase in defense spending from a year earlier. Additionally, a $30 billion increase in funding for the Federal Deposit Insurance Corporation in light of the regional banking crisis last year was a major contributor to the deficit increase.

Overall, the CBO forecasts that roughly 75% of the federal deficit’s increase will be due to interest costs by 2034.

-

Real Estate2 weeks ago

Real Estate2 weeks agoVisualizing America’s Shortage of Affordable Homes

-

Technology1 week ago

Technology1 week agoRanked: Semiconductor Companies by Industry Revenue Share

-

Money1 week ago

Money1 week agoWhich States Have the Highest Minimum Wage in America?

-

Real Estate1 week ago

Real Estate1 week agoRanked: The Most Valuable Housing Markets in America

-

Business1 week ago

Business1 week agoCharted: Big Four Market Share by S&P 500 Audits

-

AI1 week ago

AI1 week agoThe Stock Performance of U.S. Chipmakers So Far in 2024

-

Misc2 weeks ago

Misc2 weeks agoAlmost Every EV Stock is Down After Q1 2024

-

Money2 weeks ago

Money2 weeks agoWhere Does One U.S. Tax Dollar Go?