Technology

By the Numbers: Are Tech IPOs Worth the Hype?

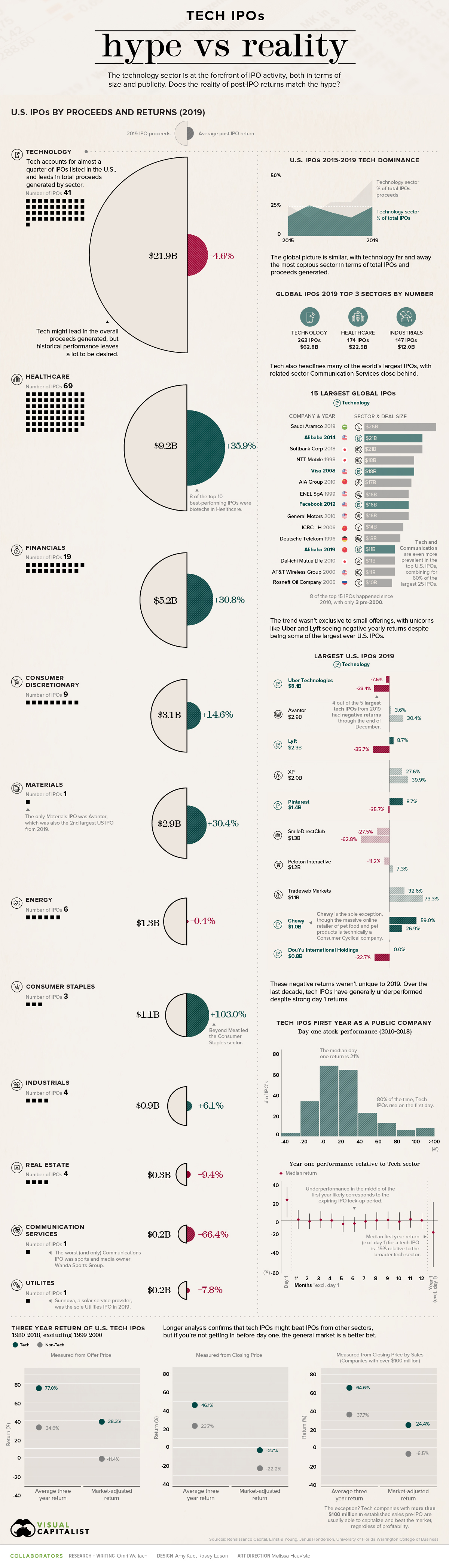

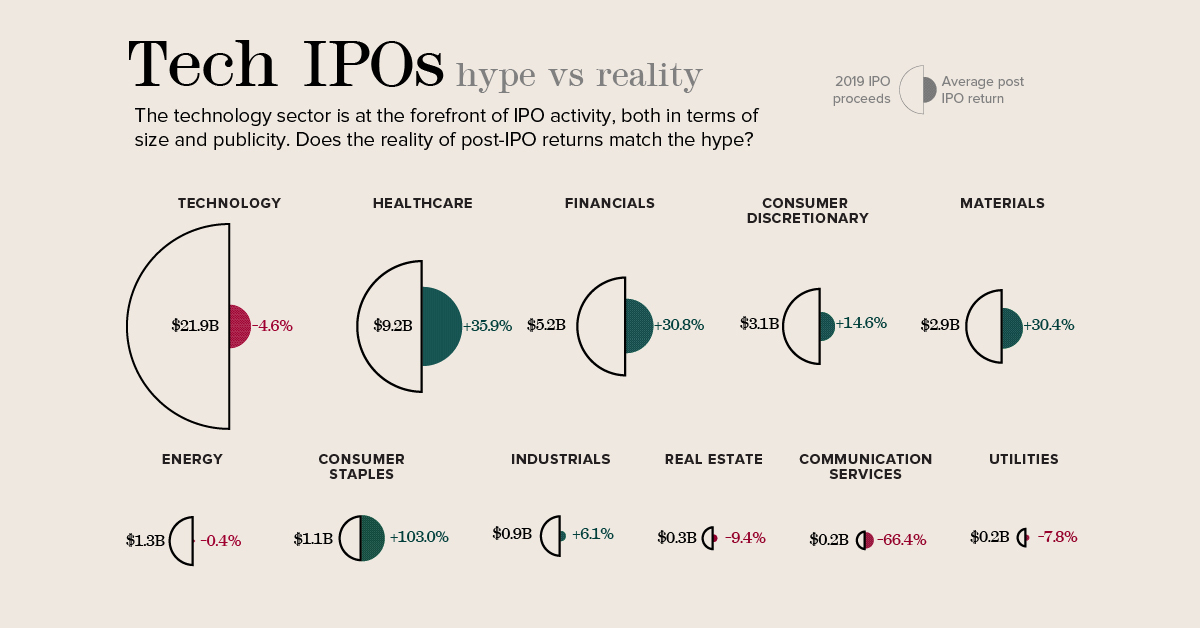

Tech IPOs — Hype vs. Reality

Initial Public Offerings (IPOs) generate massive amounts of attention from investors and media alike, especially for new and fast-rising companies in the technology sector.

On the surface, the attention is warranted. Some of the most well-known tech companies have built their profile by going public, including Facebook by raising $16 billion in 2012.

But when you peel away the hype and examine investor returns from tech IPOs more closely, the reality can leave a lot to be desired.

The Hype in Numbers

When it comes to the IPOs of companies beginning to sell shares on public stock exchanges, tech offerings have become synonymous with billion-dollar launches.

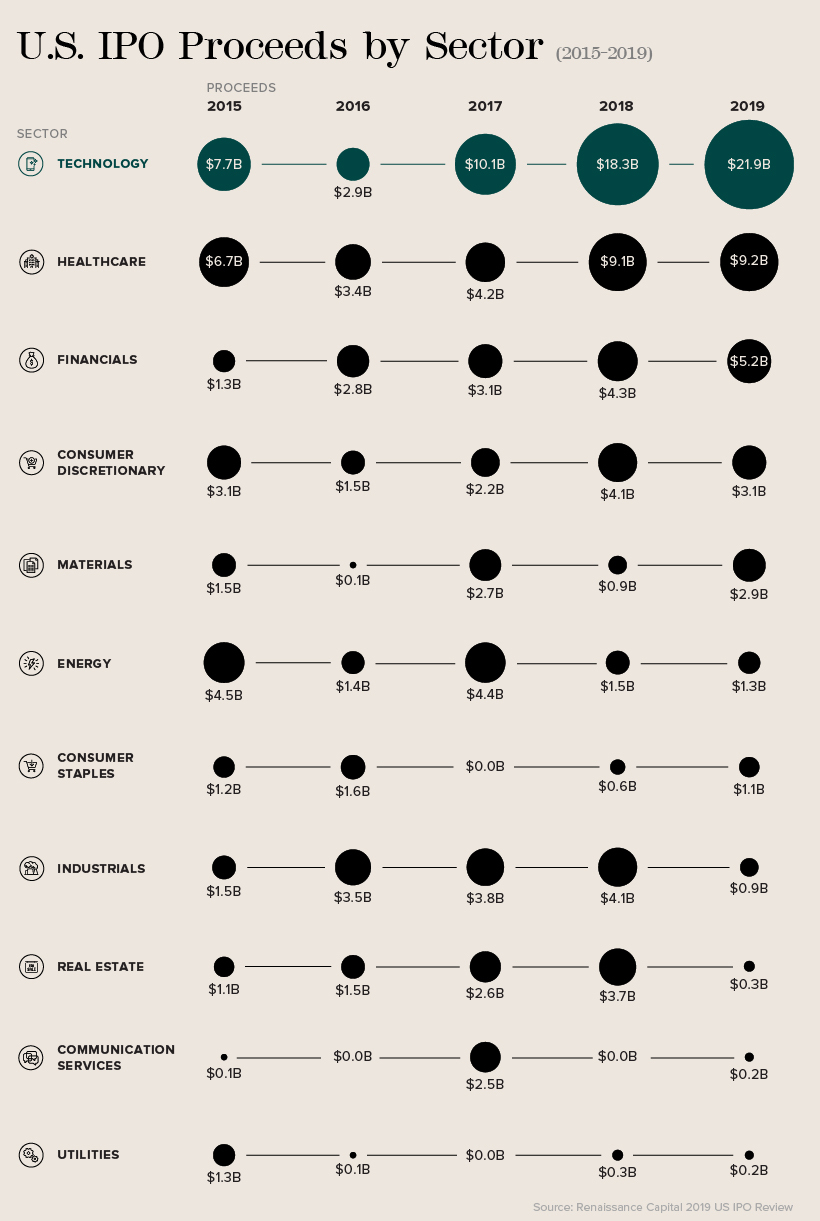

Given the sheer magnitude of IPOs based in the technology sector, it’s easy to understand why. Globally, the technology sector has regularly generated the most IPOs and highest proceeds, as shown in a recent report by Ernst & Young.

In 2019 alone, the world’s public markets saw 263 IPOs in the tech sector with total proceeds of $62.8 billion. That’s far ahead of the second-place healthcare sector, which saw 174 IPOs generate proceeds of $22.5 billion.

The discrepancy is more apparent in the U.S., according to data from Renaissance Capital. In fact, over the last five years, the tech sector has accounted for 23% of total U.S. IPOs and 34% of proceeds generated by U.S. IPOs.

The prevalence of tech is even more apparent when examining history’s largest IPOs. Of the 25 largest IPOs in U.S. history, 60% come from the technology and communication services sectors.

That list includes last year’s well-publicized IPOs for Uber ($8.1 billion) and Lyft ($2.3 billion), as well as a direct public offering from Slack ($7.4 billion). Soon the list might include Airbnb, which plans to list within the communication services sector instead of tech.

The Reality in Returns

But the proof, as they say, is in the pudding.

Uber and Lyft were two of 2019’s largest U.S. IPOs, but they also saw some of the poorest returns. Uber fell 33.4% from its IPO price at year end, while Lyft was down 35.7%.

And they were far from isolated incidents. Tech IPOs averaged a return of -4.6% last year, far behind the top sectors of consumer staples (led by Beyond Meat) and healthcare.

| Sector | Avg. IPO Return (2019) |

|---|---|

| Consumer Staples | 103.0% |

| Healthcare | 35.9% |

| Financials | 30.8% |

| Materials | 30.4% |

| Consumer Discretionary | 14.6% |

| Industrials | 6.1% |

| Energy | -0.4% |

| Technology | -4.6% |

| Utilities | -7.8% |

| Real Estate | -9.4% |

| Communication Services | -66.4% |

While last year was the first time tech IPOs have averaged a negative return in four years, analysis of the last 10 years confirms that tech IPOs have underperformed over the last decade.

A decade-long analysis from investment firm Janus Henderson demonstrated that U.S. tech IPOs start underperforming compared to the broad tech sector about 5-6 months after launching.

This dip likely corresponds to the expiry of an IPO’s lock-up period—the time that a company’s pre-IPO investors are able to sell their stock. By cashing in on strong early performance, investors flood the market and bring share prices down.

Interestingly, most gains for these IPOs tend to happen within the first day of trading. The median first-day performance for tech IPOs was a 21% increase over the offer price. That’s why the median first-year return for a tech IPO, excluding the first day of trading, is -19% when compared with the broader tech sector.

How to Make Money from Tech IPOs

So does that mean that investors should avoid tech IPOs? Not necessarily.

Longer-term analysis from the University of Florida’s Warrington College of Business shows that U.S. tech IPOs offer better returns than other sectors as long as investors get in at the offer price.

U.S. Tech IPO Returns from Offer Price

| Sector | Avg. Three-Year Return | Market-adjusted Return |

|---|---|---|

| Tech | 77.0% | 28.3% |

| Non-Tech | 34.6% | -11.4% |

Even when adjusting for the broader market performance, tech IPOs have been solid in comparison to the offer price.

The challenge is that if investors are buying stock after that first day market bump, they may have already missed out on meaningful gains:

U.S. Tech IPO Returns from First Closing Price

| Sector | Avg. Three-Year Return | Market-adjusted Return |

|---|---|---|

| Tech | 46.1% | -2.7% |

| Non-Tech | 23.7% | -22.2% |

So should investors shy away from tech IPOs unless they’re able to get in early?

Generally speaking, the analysis holds that new tech companies perform relatively well, but not better than the broader market once they’ve started trading.

However, in a world of billion-dollar unicorns, there are always exceptions to the rule. The University of Florida study found that tech companies with a base of over $100 million in sales before going public saw a market-adjusted three-year return of 24.4% from the first closing price.

If you can sift through the hype and properly analyze the right tech IPO to support, the reality can be rewarding.

Technology

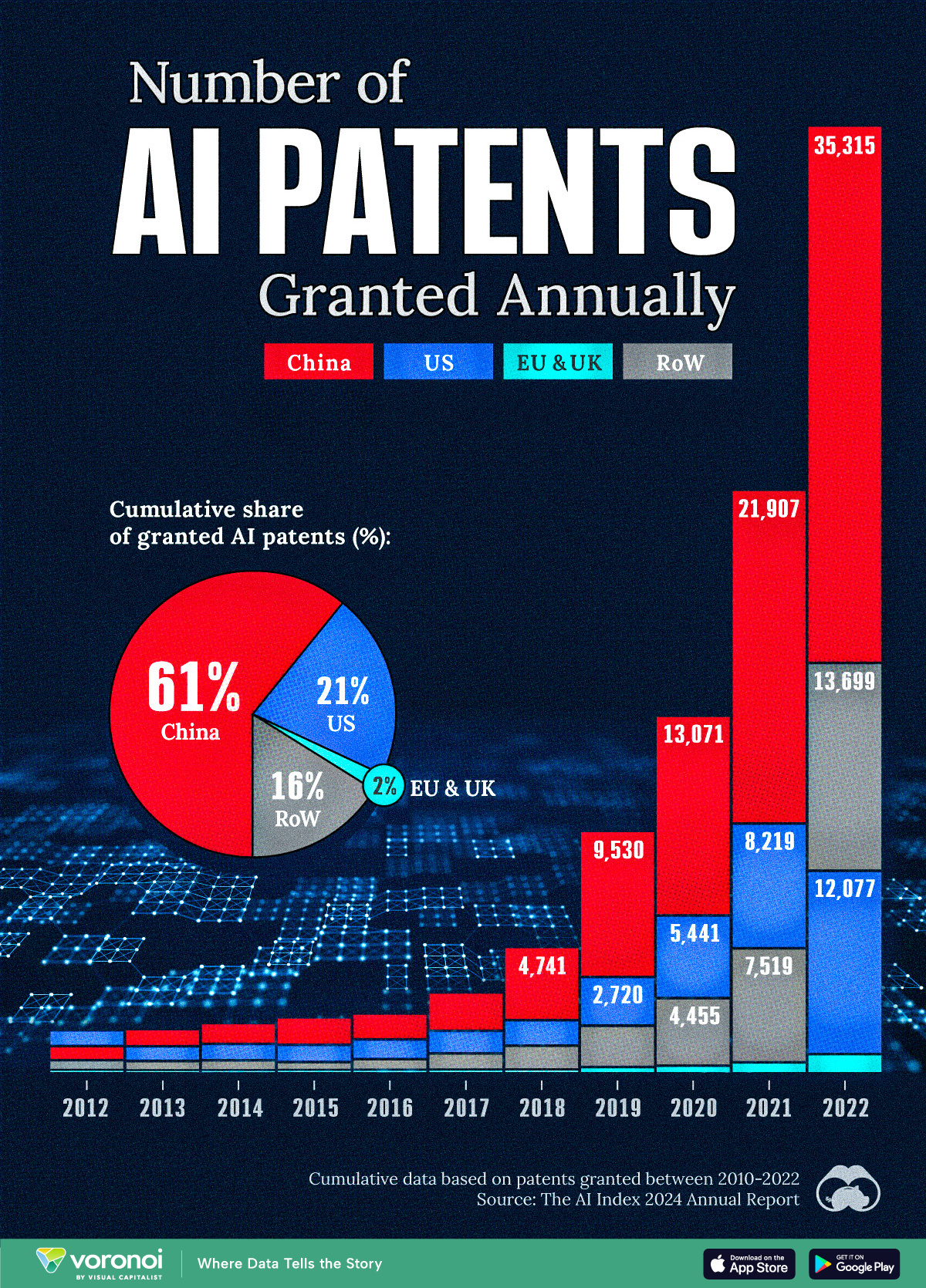

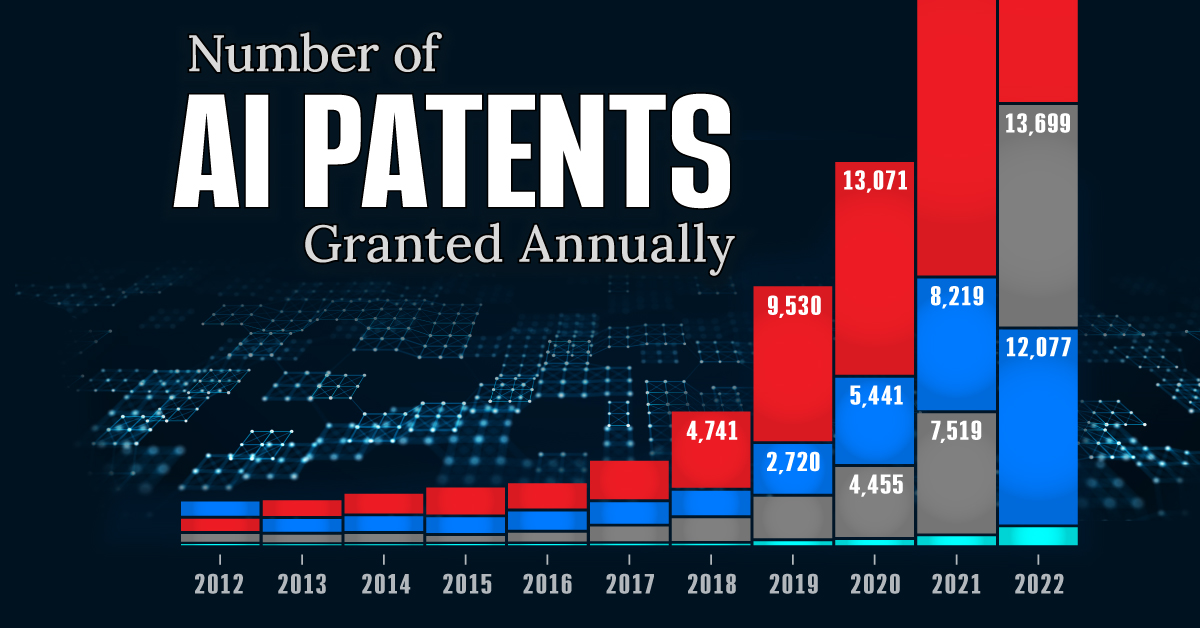

Visualizing AI Patents by Country

See which countries have been granted the most AI patents each year, from 2012 to 2022.

Visualizing AI Patents by Country

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

This infographic shows the number of AI-related patents granted each year from 2010 to 2022 (latest data available). These figures come from the Center for Security and Emerging Technology (CSET), accessed via Stanford University’s 2024 AI Index Report.

From this data, we can see that China first overtook the U.S. in 2013. Since then, the country has seen enormous growth in the number of AI patents granted each year.

| Year | China | EU and UK | U.S. | RoW | Global Total |

|---|---|---|---|---|---|

| 2010 | 307 | 137 | 984 | 571 | 1,999 |

| 2011 | 516 | 129 | 980 | 581 | 2,206 |

| 2012 | 926 | 112 | 950 | 660 | 2,648 |

| 2013 | 1,035 | 91 | 970 | 627 | 2,723 |

| 2014 | 1,278 | 97 | 1,078 | 667 | 3,120 |

| 2015 | 1,721 | 110 | 1,135 | 539 | 3,505 |

| 2016 | 1,621 | 128 | 1,298 | 714 | 3,761 |

| 2017 | 2,428 | 144 | 1,489 | 1,075 | 5,136 |

| 2018 | 4,741 | 155 | 1,674 | 1,574 | 8,144 |

| 2019 | 9,530 | 322 | 3,211 | 2,720 | 15,783 |

| 2020 | 13,071 | 406 | 5,441 | 4,455 | 23,373 |

| 2021 | 21,907 | 623 | 8,219 | 7,519 | 38,268 |

| 2022 | 35,315 | 1,173 | 12,077 | 13,699 | 62,264 |

In 2022, China was granted more patents than every other country combined.

While this suggests that the country is very active in researching the field of artificial intelligence, it doesn’t necessarily mean that China is the farthest in terms of capability.

Key Facts About AI Patents

According to CSET, AI patents relate to mathematical relationships and algorithms, which are considered abstract ideas under patent law. They can also have different meaning, depending on where they are filed.

In the U.S., AI patenting is concentrated amongst large companies including IBM, Microsoft, and Google. On the other hand, AI patenting in China is more distributed across government organizations, universities, and tech firms (e.g. Tencent).

In terms of focus area, China’s patents are typically related to computer vision, a field of AI that enables computers and systems to interpret visual data and inputs. Meanwhile America’s efforts are more evenly distributed across research fields.

Learn More About AI From Visual Capitalist

If you want to see more data visualizations on artificial intelligence, check out this graphic that shows which job departments will be impacted by AI the most.

-

Mining1 week ago

Mining1 week agoGold vs. S&P 500: Which Has Grown More Over Five Years?

-

Markets2 weeks ago

Markets2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Countries2 weeks ago

Countries2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Demographics2 weeks ago

Demographics2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries