A Golden Future: Visualizing the Economic Case for Gold

The following content is sponsored by Kalo Gold.

Visualizing the Economic Case for Gold

Throughout history, people have revered gold as a sign of wealth and a store of value. Today, gold is not only a precious metal but also a precious investment.

In fact, in 2020, 47% of global gold demand—the largest share—came from investors.

Today’s infographic from Kalo Gold outlines the economic case for gold and highlights some of the main reasons why investors are attracted to it.

Gold as an Investment: A Shield for All Financial Conditions

Gold can protect investors’ wealth during tough times while preserving capital for the long run. Investors add gold to their portfolios because it offers many investment benefits:

- Effective diversification

In a typical portfolio of stocks and bonds, gold’s historically low correlation with major asset classes and negative correlation with the U.S. dollar can reduce risk through diversification.

- Hedge against inflation

Gold is priced in U.S. dollars. Therefore, as the purchasing power of the dollar falls due to inflation, gold becomes more expensive to buy, acting as a hedge against the eroding value of the dollar.

- Long-term returns

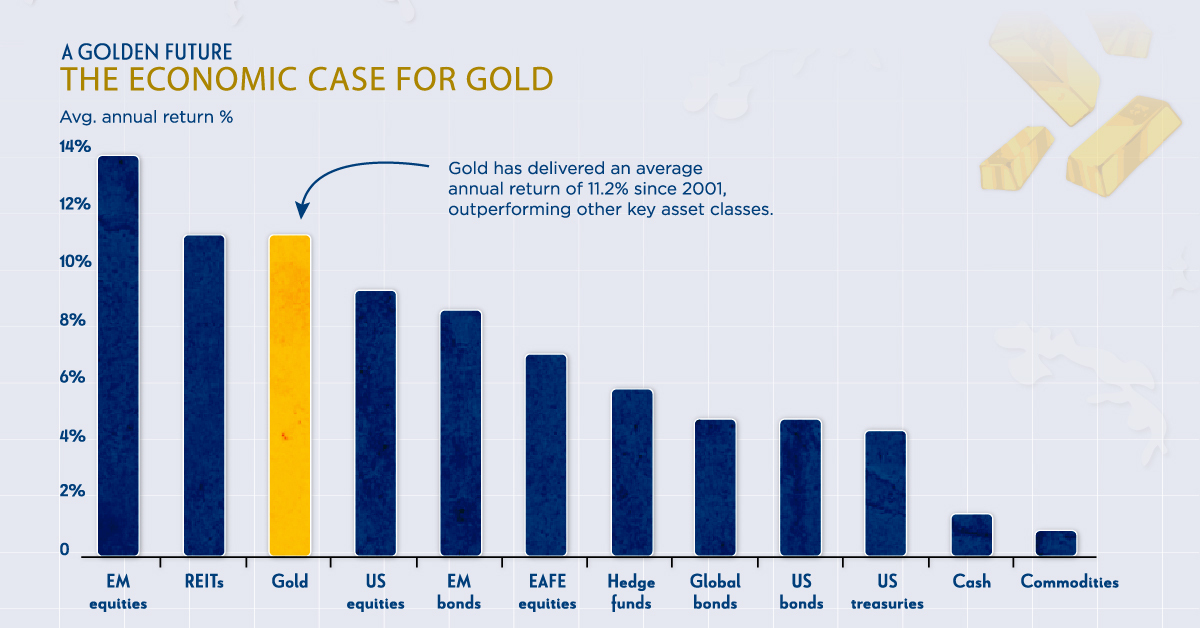

Gold has always maintained its value in the long run. Between 2001 and 2020, gold’s annual return averaged 11.2%, outperforming other key asset classes including U.S. equities, bonds, and treasuries.

Additionally, gold’s low correlation with other assets allows it to outperform during recessionary periods, reducing the downside of stock market downturns. In fact, gold delivered positive returns during the recessions in 2001 and 2008 while the S&P 500 went negative.

Amid the economic turbulence of 2020, investors turned to gold once again, with record-high inflows in gold ETFs. And in turn, gold generated a 25% annual return.

Gold: Precious Today, Tomorrow, and Forever

With rapidly rising money supply and near-zero interest rates in response to the COVID-19 recession, the world is entering an era of quantitative easing, and possibly, higher inflation.

This could create the perfect storm for gold, for three key reasons:

- Gold has historically performed well during periods of high inflation (greater than 3%), delivering an average annual return of 15.4%.

- The price of gold has historically tracked the growth in the global stock of M2 money supply.

- Low interest rates reduce the opportunity cost of gold holding gold. Therefore, gold often outperforms when real interest rates fall.

The economic case for gold is built on its ability to protect investors in downturns and volatile times while preserving wealth for the long term.

Gold does not rust—it will always hold its value, as a precious metal and a precious investment.

-

Sponsored3 years ago

Sponsored3 years agoMore Than Precious: Silver’s Role in the New Energy Era (Part 3 of 3)

Long known as a precious metal, silver in solar and EV technologies will redefine its role and importance to a greener economy.

-

Sponsored7 years ago

Sponsored7 years agoThe History and Evolution of the Video Games Market

Everything from Pong to the rise of mobile gaming and AR/VR. Learn about the $100 billion video games market in this giant infographic.

-

Sponsored8 years ago

Sponsored8 years agoThe Extraordinary Raw Materials in an iPhone 6s

Over 700 million iPhones have now been sold, but the iPhone would not exist if it were not for the raw materials that make the technology...

-

Sponsored8 years ago

Sponsored8 years agoThe Industrial Internet, and How It’s Revolutionizing Mining

The convergence of the global industrial sector with big data and the internet of things, or the Industrial Internet, will revolutionize how mining works.