Mining

9 Reasons Mining Investors are Looking at Yukon Companies

In the mining industry, location is paramount.

Invest your capital in a jurisdiction that doesn’t respect that investment, or in a place with little geological potential, and it’s possible that it will end up going to waste.

That’s why, when there’s a place on the map that has world-class geology and also a plan for working with miners and new explorers, the money begins to flow to take advantage of that potential.

Why Investors are Looking at the Yukon

Today’s infographic comes to us from the Yukon Mining Alliance and it shows nine reasons on why people are investing in Yukon mining and exploration companies today.

For resource investors, it is rare to see variables like government investment, jurisdiction, geological potential, and investment from major mining companies all aligning.

However, in the Yukon, it seems this may be the case.

9 Reasons for the Yukon

Here are nine reasons the Yukon is starting to attract more investment capital:

1. Rich History

Mining was central to the Yukon even over a century ago, when over 100,000 fortune-seekers stampeded into the Yukon with the goal of striking it rich in the famous Klondike Gold Rush.

2. Geological Profile

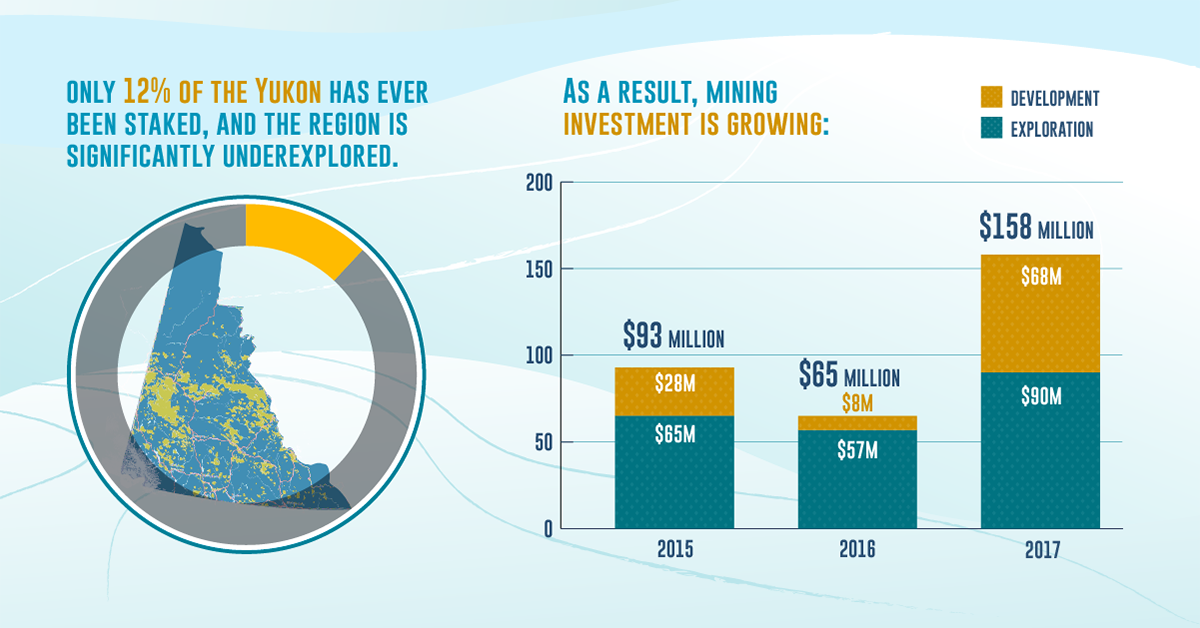

In the last decade, there have been major discoveries of gold, silver, copper, zinc, and lead in the Yukon – but perhaps most interestingly, only 12% of the Yukon has been staked, making the region highly under-explored. Spending on exploration and development rose from $93 million to $158 million from 2015-2017.

3. Major Investment

Major mining companies now have a stake in the polymetallic rush. Recent companies to foray into the Yukon include Agnico-Eagle, Barrick, Couer Mining, Goldcorp, Kinross, and Newmont.

4. Leaders in Exploration and Mining

Juniors in the region are working on new geological ideas as well as new technology to unlock the vast potential of the region.

5. Progressive Partnerships

First Nations and the Government of Yukon have recently championed a new government-to-government relationship that enables them to be on the exact same page when it comes to mineral projects.

6. Government Investment

The Yukon government is investing in new infrastructure (via the Resource Gateway Project). It also offers the Yukon Mineral Exploration Program (YMEP), which provides a portion of risk capital to explore and develop mineral projects to an advanced stage.

7. Made in Yukon Process

The Yukon government also tries to foster regulatory certainty to create clarity for companies and investors, by its customized tri-party process.

8. Infrastructure

The jurisdiction has 5,000km of government maintained roads, receives 95% of power from clean hydro, has international and local airports, and has access to three deep-water, ice-free ports.

9. Geopolitical Stability

Canada offers geopolitical stability to start with – but with unprecedented cooperation between the territorial government and First Nations, the Yukon is arguably a step above the rest of the country.

Copper

Brass Rods: The Secure Choice

This graphic shows why brass rods are the secure choice for precision-machined and forged parts.

Brass Rods: The Secure Choice

The unique combination of machinability and recyclability makes brass rods the secure choice for manufacturers seeking future-proof raw material solutions.

This infographic, from the Copper Development Association, shows three ways brass rods give manufacturers greater control and a license to grow in the competitive market for precision-machined and forged products.

Future-Proof Investments in New Machine Tools

A material’s machinability directly impacts machine throughput, which typically has the largest impact on machine shop profitability.

The high-speed machining capabilities of brass rods maximize machine tool performance, allowing manufacturers to run the material faster and longer without sacrificing tool life, chip formation, or surface quality.

The high machining efficiency of brass leads to reduced per-part costs, quicker return on investment (ROI) for new machine tools, and expanded production capacity for new projects.

Supply Security Through Closed Loop Recycling

Brass, like its parent element copper, can be infinitely recycled.

In 2022, brass- and wire-rod mills accounted for the majority of the 830,000 tonnes of copper recycled from scrap in the United States.

Given that scrap ratios for machined parts typically range from 60-70% by weight, producing mills benefit from a secure and steady supply of clean scrap returned directly from customers, which is recycled to create new brass rods.

The high residual value of brass scrap creates a strong recycling incentive. Scrap buy back programs give manufacturers greater control over raw material net costs as scrap value is often factored into supplier purchase agreements.

Next Generation Alloys for a Lead-Free Future

Increasingly stringent global regulations continue to pressure manufacturers to minimize the use of materials containing trace amounts of lead and other harmful impurities.

The latest generation of brass-rod alloys is engineered to meet the most demanding criteria for lead leaching in drinking water and other sensitive applications.

Seven brass-rod alloys passed rigorous testing to become the only ‘Acceptable Materials’ against lower lead leaching criteria recently adopted in the national U.S. drinking water quality standard, NSF 61.

Learn more about the advantages of brass rods solutions.

-

Base Metals1 year ago

Base Metals1 year agoRanked: The World’s Largest Copper Producers

Many new technologies critical to the energy transition rely on copper. Here are the world’s largest copper producers.

-

Silver2 years ago

Silver2 years agoMapped: Solar Power by Country in 2021

In 2020, solar power saw its largest-ever annual capacity expansion at 127 gigawatts. Here’s a snapshot of solar power capacity by country.

-

Batteries5 years ago

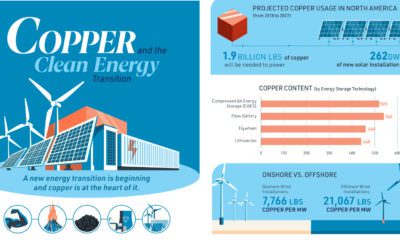

Batteries5 years agoVisualizing Copper’s Role in the Transition to Clean Energy

A clean energy transition is underway as wind, solar, and batteries take center stage. Here’s how copper plays the critical role in these technologies.

-

Science5 years ago

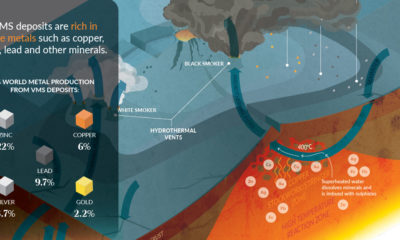

Science5 years agoEverything You Need to Know on VMS Deposits

Deep below the ocean’s waves, VMS deposits spew out massive amounts of minerals like copper, zinc, and gold, making them a key source of the metals…

-

Copper5 years ago

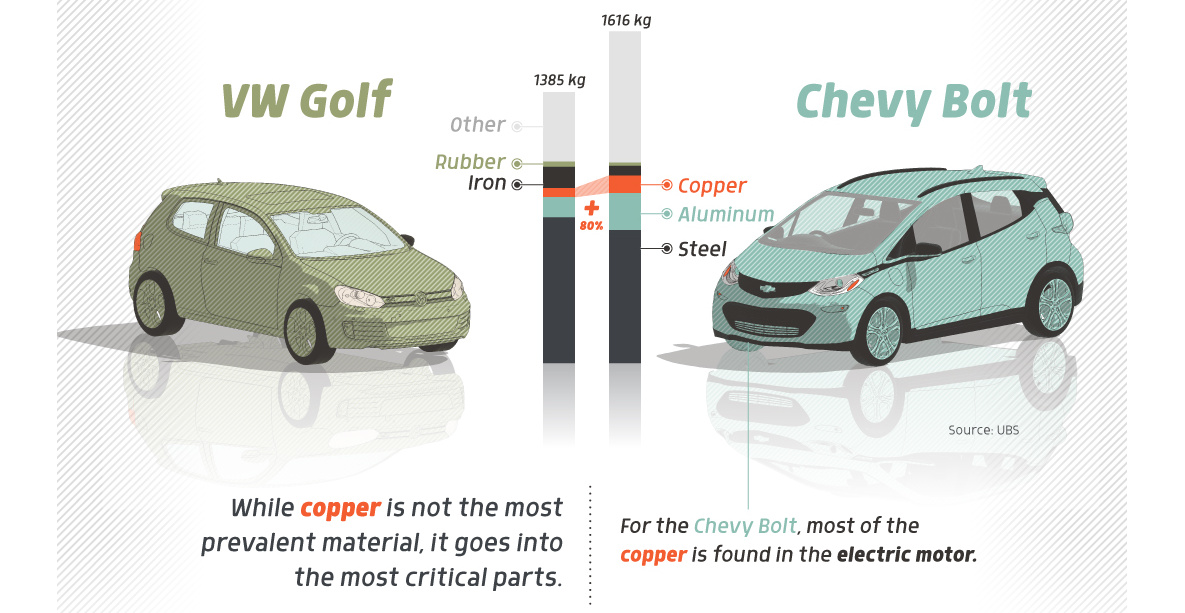

Copper5 years agoHow Much Copper is in an Electric Vehicle?

Have you ever wondered how much copper is in an electric vehicle? This infographic shows the metal’s properties as well as the quantity of copper used.

-

Copper6 years ago

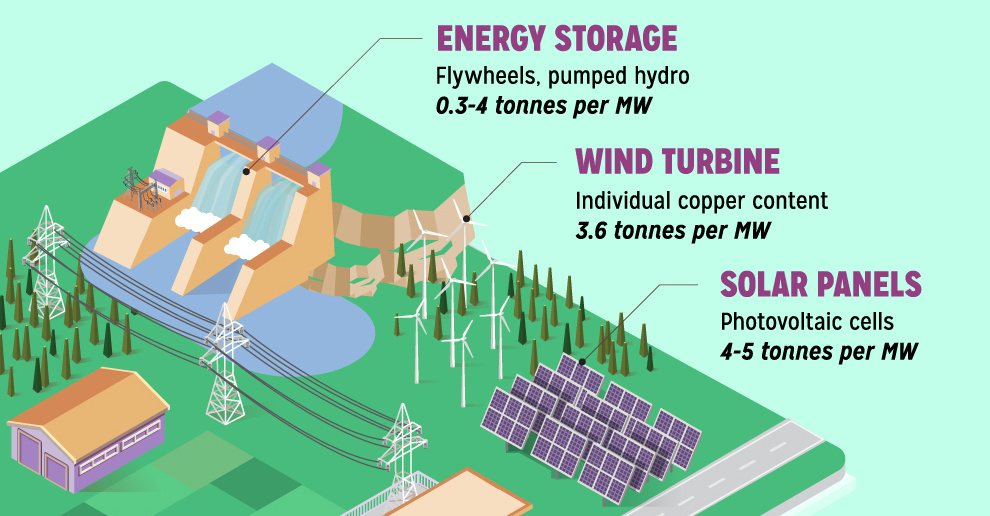

Copper6 years agoCopper: Driving the Green Energy Revolution

Renewable energy is set to fuel a new era of copper demand – here’s how much copper is used in green applications from EVs to photovoltaics.

-

Green2 weeks ago

Green2 weeks agoRanked: Top Countries by Total Forest Loss Since 2001

-

Travel1 week ago

Travel1 week agoRanked: The World’s Top Flight Routes, by Revenue

-

Technology1 week ago

Technology1 week agoRanked: Semiconductor Companies by Industry Revenue Share

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

Real Estate2 weeks ago

Real Estate2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Markets2 weeks ago

Markets2 weeks agoCharted: Big Four Market Share by S&P 500 Audits

-

AI2 weeks ago

AI2 weeks agoThe Stock Performance of U.S. Chipmakers So Far in 2024

-

Automotive2 weeks ago

Automotive2 weeks agoAlmost Every EV Stock is Down After Q1 2024