Markets

7 Facts That Will Free You From the Fear of Stock Market Crashes

.container {

max-width: 1070px;

}

.button {

display: inline-block;

height: 45px;

color: #ffffff;

text-align: center;

font-family: helvetica;

letter-spacing: .01rem;

text-decoration: none;

white-space: nowrap;

border-radius: 0px;

line-height: 45px;

border: 1px;

font-size: em(13);

cursor: pointer;

box-sizing: border-box;

background: #22255A;

transition-duration: 0.4s;

margin-bottom: 1px;

width: 16.6666%;

}

.button-group {

position: left;

width: 100%;

display: inline-block;

list-style: none;

padding: 0;

margin: 0;

/* IE hacks */

zoom: 1;

*display: inline;

}

.button-group li {

float: left;

padding: 0;

margin: 0;

}

.button-group .button {

display: inline-block;

box-sizing: border-box;

color: white;

}

.button-group > .button:not(:first-child):not(:last-child), .button-group li:not(:first-child):not(:last-child) .button {

border-radius: 0;

}

.button-group > .button:first-child, .button-group li:first-child .button {

margin-left: 0;

border-top-right-radius: 0;

border-bottom-right-radius: 0;

}

.button-group > .button:last-child, .button-group li:last-child > .button {

border-top-left-radius: 0;

border-bottom-left-radius: 0;

border-bottom-right-radius: 0;

}

.button:hover {

background-color: #8E8059;

}

.button.active {

background-color: #8E8059;

}

.button-group :not(:last-child) {

border-right: 1px solid white;

padding-right: 2px;

}

.button-group {

border-right: none;

margin-right: none;

}

@media (max-width: 600px) {

.button {

font-size: 13px;}

}

7 Facts That Will Free You From a Fear of Stock Market Crashes

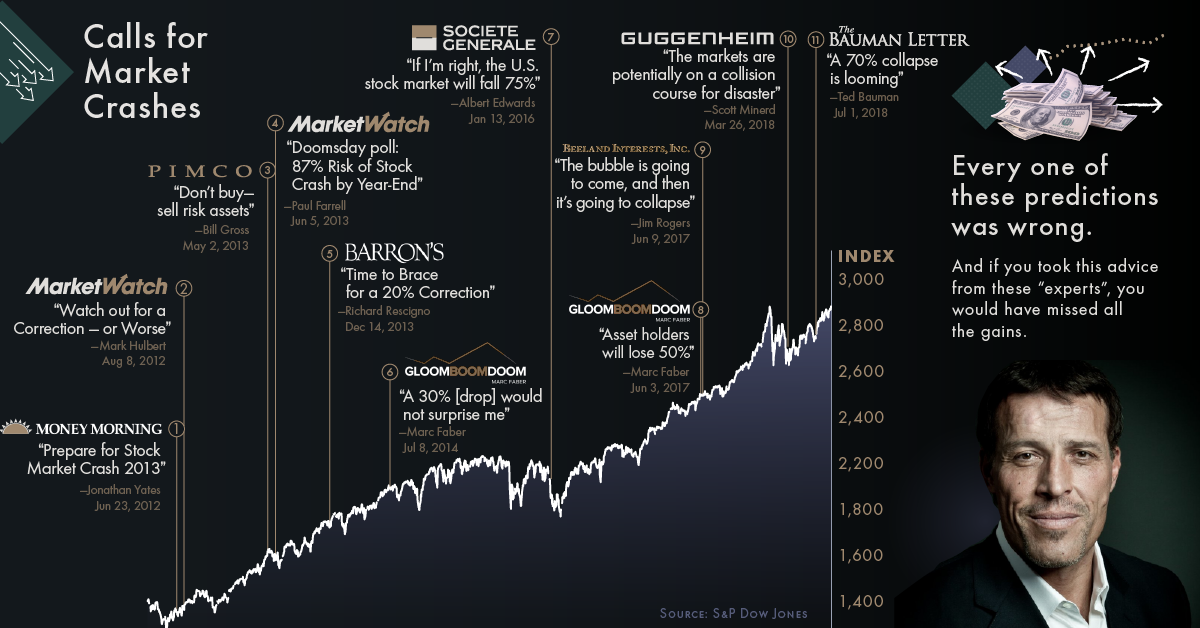

The current bull market in stocks is closing in on an astounding 10 years in length, making it the longest bull market run in all of modern history.

Largest Bull Markets

| Rank | Bull Market | Length |

|---|---|---|

| #1 | 09’-18’ (Current) | 115 months* |

| #2 | ’90-‘00 | 114 months |

| #3 | ’49-‘56 | 86 months |

| #4 | ’74-‘80 | 74 months |

| #5 | ’82-‘87 | 60 months |

*As of September 2018

Understandably, this makes many people very nervous.

Everyone remembers the mayhem of 2008 – and with stock prices at all-time highs, the fear of a market meltdown is a valid concern for many investors.

How to Become Unshakeable

Today’s infographic is from Tony Robbins, leveraging data and talking points from his #1 Best Selling book Unshakeable: Your Financial Freedom Playbook, which is now available on paperback.

It leans on insights from the world’s top investors – like Ray Dalio and John Bogle – to present seven indisputable facts about market crashes, using clear patterns established over decades of data.

By understanding these seven facts, you’ll be able to prepare for the recurring seasons of the financial market, including winter, and it will help give you an enormous edge over even many sophisticated and experienced investors.

Seven Indisputable Facts

Here are the seven facts that will free you from a fear of stock market crashes:

Fact #1: On average, corrections happen once per year

For more than a century, the market has seen close to one correction (a decline of 10% or more) per year. In other words, corrections are a regular part of financial seasons – and you can expect to see as many corrections as birthdays throughout your life.

The average correction looks something like this:

- 54 days long

- 13.5% market decline

- Occurs once per year

The uncertainty of a correction can prompt people to make big mistakes – but in reality, most corrections are over before you know it. If you hold on tight, it’s likely the storm will pass.

Fact #2: Fewer than 20% of all corrections turn into a bear market

When the stock market starts tumbling, it can be tempting to abandon ship by selling assets and moving into cash. However, doing so could be a big mistake.

You would likely be selling all of your assets at a low, right before the market rebounds!

Why? Fewer than 20% of corrections turn into bear markets. Put another way, 80% of corrections are just short breaks in otherwise intact bull markets – meaning that selling early would make you miss the rest of the upward trend.

Fact #3: Nobody can predict consistently whether the market will rise or fall

The media perpetuates a myth that, if you’re smart enough, you can predict the market’s moves and avoid its downdrafts.

But the reality is: no one can time the market.

During the current nine year bull market, there have been dozens of calls for stock market crashes from even very seasoned investors. None of these calls have come true, and if you’d have listened to these experts, you would have missed the upside.

The only value of stock forecasters is to make fortune-tellers look good.

– Warren Buffett

Fact #4: The market has always risen, despite short-term setbacks

Market drops are a very regular occurrence. For example, the S&P 500 – the main index that tracks the U.S. stock market – has fallen on average 14.2% at least one point each year between 1980-2015.

Like winter, these drops are a part of the market’s seasons. Over this same period of time, despite these temporary drops, the market ended up achieving a positive return 27 of 36 years. That’s 75% of the time!

Fact #5: Historically, bear markets have happened every three to five years

In the 115 year span between 1900-2015, there have been 34 bear markets.

But bear markets don’t last. Over that timeframe, they’ve varied in length from 45 days to 694 days, but on average they lasted about a year.

Fact #6: Bear markets become bull markets

Do you remember how fragile the world seemed in 2008 when banks were collapsing and the stock market was in free fall?

When you pictured the future, did it seem dark and dangerous? Or did it seem like the good times were just around the corner and the party was about to begin?

The fact is, once a bear market ends, the following 12 months can see crucial market gains.

The best opportunities come in times of maximum pessimism.

– John Templeton

Fact #7: The greatest danger is being out of the market

From 1996 through 2015, the S&P 500 returned an average of 8.2% a year.

But if you missed out on the top 10 trading days during that period, your returns dwindled to just 4.5% a year.

It gets worse! If you missed out on the top 20 trading days, your returns were just 2.1%.

And if you missed out on the top 30 trading days? Your returns vanished into thin air, falling all the way to zero!

You can’t win by sitting on the bench. You have to be in the game. To put it another way, fear isn’t rewarded. Courage is.

– Tony Robbins

Markets

U.S. Debt Interest Payments Reach $1 Trillion

U.S. debt interest payments have surged past the $1 trillion dollar mark, amid high interest rates and an ever-expanding debt burden.

U.S. Debt Interest Payments Reach $1 Trillion

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

The cost of paying for America’s national debt crossed the $1 trillion dollar mark in 2023, driven by high interest rates and a record $34 trillion mountain of debt.

Over the last decade, U.S. debt interest payments have more than doubled amid vast government spending during the pandemic crisis. As debt payments continue to soar, the Congressional Budget Office (CBO) reported that debt servicing costs surpassed defense spending for the first time ever this year.

This graphic shows the sharp rise in U.S. debt payments, based on data from the Federal Reserve.

A $1 Trillion Interest Bill, and Growing

Below, we show how U.S. debt interest payments have risen at a faster pace than at another time in modern history:

| Date | Interest Payments | U.S. National Debt |

|---|---|---|

| 2023 | $1.0T | $34.0T |

| 2022 | $830B | $31.4T |

| 2021 | $612B | $29.6T |

| 2020 | $518B | $27.7T |

| 2019 | $564B | $23.2T |

| 2018 | $571B | $22.0T |

| 2017 | $493B | $20.5T |

| 2016 | $460B | $20.0T |

| 2015 | $435B | $18.9T |

| 2014 | $442B | $18.1T |

| 2013 | $425B | $17.2T |

| 2012 | $417B | $16.4T |

| 2011 | $433B | $15.2T |

| 2010 | $400B | $14.0T |

| 2009 | $354B | $12.3T |

| 2008 | $380B | $10.7T |

| 2007 | $414B | $9.2T |

| 2006 | $387B | $8.7T |

| 2005 | $355B | $8.2T |

| 2004 | $318B | $7.6T |

| 2003 | $294B | $7.0T |

| 2002 | $298B | $6.4T |

| 2001 | $318B | $5.9T |

| 2000 | $353B | $5.7T |

| 1999 | $353B | $5.8T |

| 1998 | $360B | $5.6T |

| 1997 | $368B | $5.5T |

| 1996 | $362B | $5.3T |

| 1995 | $357B | $5.0T |

| 1994 | $334B | $4.8T |

| 1993 | $311B | $4.5T |

| 1992 | $306B | $4.2T |

| 1991 | $308B | $3.8T |

| 1990 | $298B | $3.4T |

| 1989 | $275B | $3.0T |

| 1988 | $254B | $2.7T |

| 1987 | $240B | $2.4T |

| 1986 | $225B | $2.2T |

| 1985 | $219B | $1.9T |

| 1984 | $205B | $1.7T |

| 1983 | $176B | $1.4T |

| 1982 | $157B | $1.2T |

| 1981 | $142B | $1.0T |

| 1980 | $113B | $930.2B |

| 1979 | $96B | $845.1B |

| 1978 | $84B | $789.2B |

| 1977 | $69B | $718.9B |

| 1976 | $61B | $653.5B |

| 1975 | $55B | $576.6B |

| 1974 | $50B | $492.7B |

| 1973 | $45B | $469.1B |

| 1972 | $39B | $448.5B |

| 1971 | $36B | $424.1B |

| 1970 | $35B | $389.2B |

| 1969 | $30B | $368.2B |

| 1968 | $25B | $358.0B |

| 1967 | $23B | $344.7B |

| 1966 | $21B | $329.3B |

Interest payments represent seasonally adjusted annual rate at the end of Q4.

At current rates, the U.S. national debt is growing by a remarkable $1 trillion about every 100 days, equal to roughly $3.6 trillion per year.

As the national debt has ballooned, debt payments even exceeded Medicaid outlays in 2023—one of the government’s largest expenditures. On average, the U.S. spent more than $2 billion per day on interest costs last year. Going further, the U.S. government is projected to spend a historic $12.4 trillion on interest payments over the next decade, averaging about $37,100 per American.

Exacerbating matters is that the U.S. is running a steep deficit, which stood at $1.1 trillion for the first six months of fiscal 2024. This has accelerated due to the 43% increase in debt servicing costs along with a $31 billion dollar increase in defense spending from a year earlier. Additionally, a $30 billion increase in funding for the Federal Deposit Insurance Corporation in light of the regional banking crisis last year was a major contributor to the deficit increase.

Overall, the CBO forecasts that roughly 75% of the federal deficit’s increase will be due to interest costs by 2034.

-

Technology2 weeks ago

Technology2 weeks agoRanked: The Most Popular Smartphone Brands in the U.S.

-

Automotive1 week ago

Automotive1 week agoAlmost Every EV Stock is Down After Q1 2024

-

Money1 week ago

Money1 week agoWhere Does One U.S. Tax Dollar Go?

-

Green2 weeks ago

Green2 weeks agoRanked: Top Countries by Total Forest Loss Since 2001

-

Real Estate2 weeks ago

Real Estate2 weeks agoVisualizing America’s Shortage of Affordable Homes

-

Maps2 weeks ago

Maps2 weeks agoMapped: Average Wages Across Europe

-

Mining2 weeks ago

Mining2 weeks agoCharted: The Value Gap Between the Gold Price and Gold Miners

-

Demographics2 weeks ago

Demographics2 weeks agoVisualizing the Size of the Global Senior Population