Technology

27 Fintech Unicorns, and Where They Were Born

The 27 Fintech Unicorns, and Where They Were Born

Everyone wants faster, cheaper, and more customized financial services – and since technology now makes this possible, the world is embracing the fintech revolution.

In 2015, investments in fintech nearly doubled to $22.3 billion. And although there were 1,108 deals made, there are only 27 companies that can call themselves unicorns – private companies valued at over $1 billion or more.

Locating the Fintech Unicorns

Today’s infographic breaks down data on the 27 fintech unicorns, and it comes from Glance Technologies, a Canadian-based payments company that just IPO’d on the Canadian Securities Exchange.

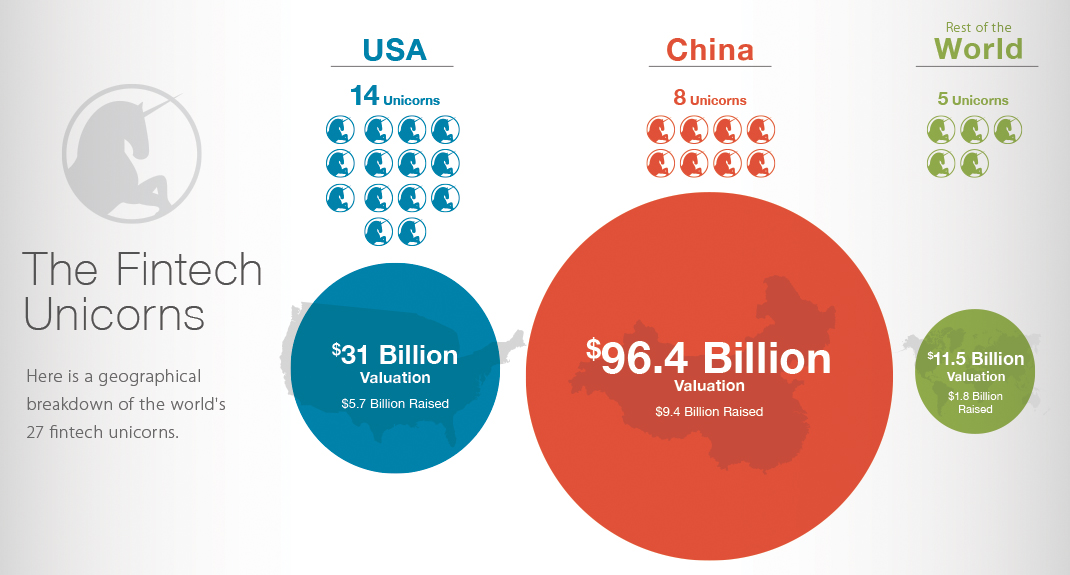

In total, the world’s fintech unicorns add up to a total valuation of $138.9 billion, and here’s how that is distributed by geography:

| Location | Unicorns | Total Value | Raised |

|---|---|---|---|

| United States | 14 | $31.0B | $5.7B |

| China | 8 | $96.4B | $9.4B |

| Rest of World | 5 | $11.5B | $1.8B |

| Total | 27 | $138.9B | $16.9B |

Amazingly, the 27 fintech unicorns have only been born in six countries: United States, China, Sweden, India, the Netherlands, and the UK.

The United States has more than half of all fintech unicorns (14), including nine in Silicon Valley. China has eight unicorns, while the UK has two. Sweden, India, and the Netherlands each have one.

While the U.S. can say it is home to more unicorns, the Chinese ones have far more value so far. The biggest four fintech unicorns worldwide were all born in China: Ant Financial ($60 billion), Lufax ($18.5 billion), JD Finance ($7 billion), and Qufenqi ($5.9 billion). This is because China has more than 500 million smartphone users, with a more evolved market for payments and P2P lending.

Fintech Unicorns by Sub-Sector

Fintech is a broad net that encompasses everything from health insurance apps to robo-advisors. As a result, different sub-sectors within fintech are maturer with more unicorns and success stories (payments, lending), while others do not have any unicorns yet (wealth management, blockchain).

Here are the 27 fintech unicorns, organized by sub-sector:

| Sub-sector | Unicorns | Valuation | % of total |

|---|---|---|---|

| Payments | 7 | $77.9B | 56.1% |

| Lending | 8 | $30.4B | 21.9% |

| Financial Services | 3 | $11.5B | 8.3% |

| Consumer financing | 2 | $7.9B | 5.7% |

| Enterprise/SaaS | 5 | $6.5B | 4.7% |

| Insurance | 2 | $4.7B | 3.4% |

| 27 | $138.9B | 100.0% |

The biggest fintech startups are in payments and lending, which combine for nearly 80% of the value of all unicorns combined. Meanwhile, all other sub-sectors including insurance, enterprise/SaaS, financial services, and consumer financing add up to roughly 20%.

Future Unicorns

Will future fintech unicorns follow similar tracks to their predecessors?

The biggest success stories have come from payments and P2P lending, especially in China. Today, however, the Chinese payments market seems pretty hard to crack, with big dogs like Alibaba, JD.com, and Tencent all having their hands in the cookie jar. Recently, P2P lending has also been under scrutiny by regulators in China, and even U.S. lending champions such as Lending Club are having challenges as of late.

Perhaps the next fintech giant will come from somewhere outside of the status quo.

Technology

Visualizing AI Patents by Country

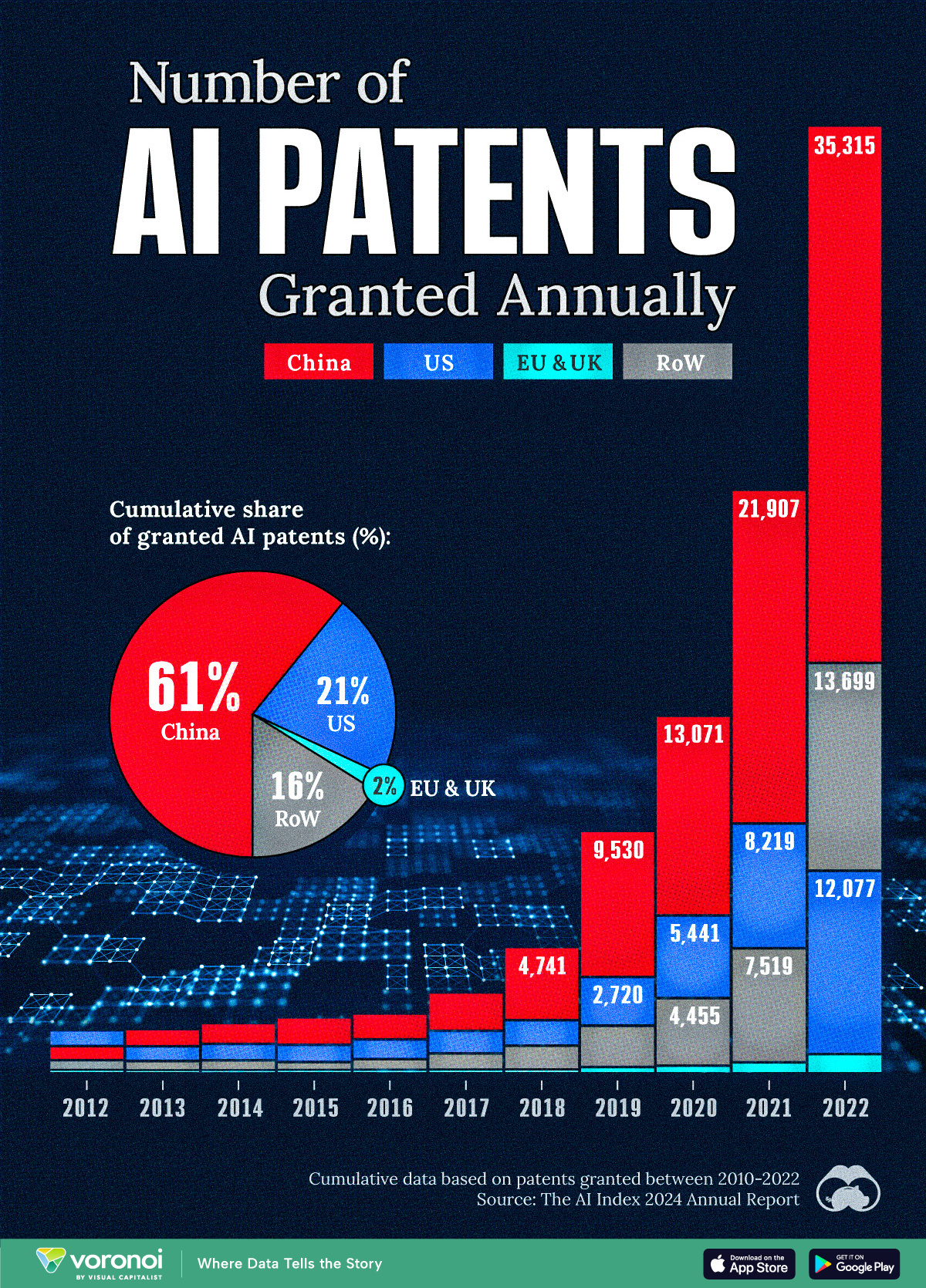

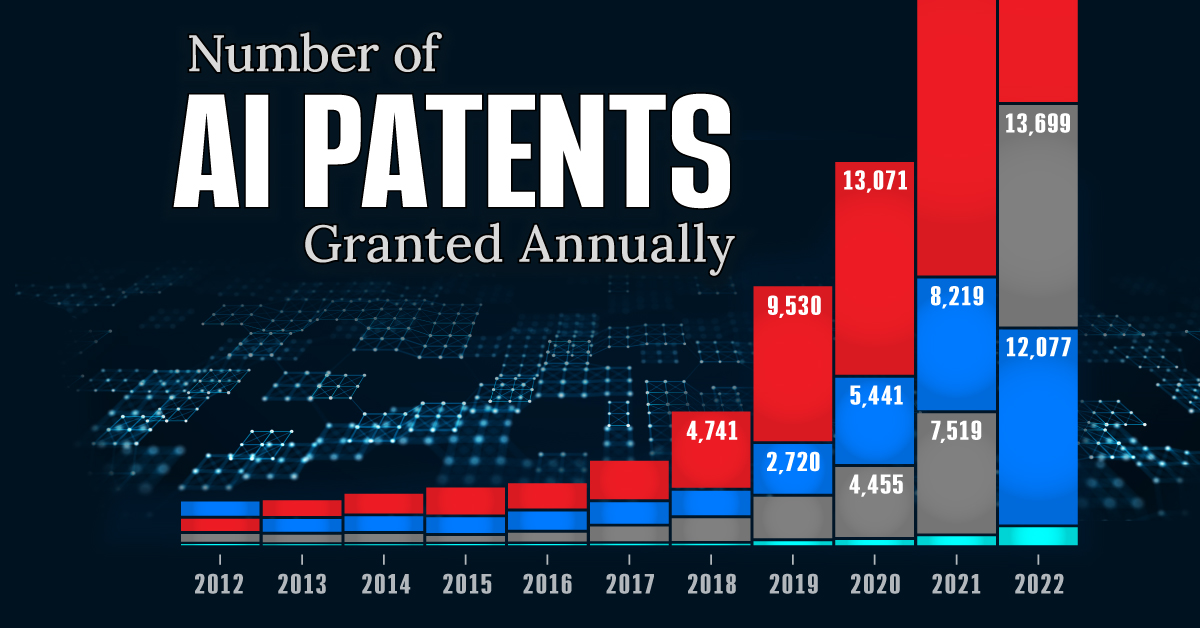

See which countries have been granted the most AI patents each year, from 2012 to 2022.

Visualizing AI Patents by Country

This was originally posted on our Voronoi app. Download the app for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

This infographic shows the number of AI-related patents granted each year from 2010 to 2022 (latest data available). These figures come from the Center for Security and Emerging Technology (CSET), accessed via Stanford University’s 2024 AI Index Report.

From this data, we can see that China first overtook the U.S. in 2013. Since then, the country has seen enormous growth in the number of AI patents granted each year.

| Year | China | EU and UK | U.S. | RoW | Global Total |

|---|---|---|---|---|---|

| 2010 | 307 | 137 | 984 | 571 | 1,999 |

| 2011 | 516 | 129 | 980 | 581 | 2,206 |

| 2012 | 926 | 112 | 950 | 660 | 2,648 |

| 2013 | 1,035 | 91 | 970 | 627 | 2,723 |

| 2014 | 1,278 | 97 | 1,078 | 667 | 3,120 |

| 2015 | 1,721 | 110 | 1,135 | 539 | 3,505 |

| 2016 | 1,621 | 128 | 1,298 | 714 | 3,761 |

| 2017 | 2,428 | 144 | 1,489 | 1,075 | 5,136 |

| 2018 | 4,741 | 155 | 1,674 | 1,574 | 8,144 |

| 2019 | 9,530 | 322 | 3,211 | 2,720 | 15,783 |

| 2020 | 13,071 | 406 | 5,441 | 4,455 | 23,373 |

| 2021 | 21,907 | 623 | 8,219 | 7,519 | 38,268 |

| 2022 | 35,315 | 1,173 | 12,077 | 13,699 | 62,264 |

In 2022, China was granted more patents than every other country combined.

While this suggests that the country is very active in researching the field of artificial intelligence, it doesn’t necessarily mean that China is the farthest in terms of capability.

Key Facts About AI Patents

According to CSET, AI patents relate to mathematical relationships and algorithms, which are considered abstract ideas under patent law. They can also have different meaning, depending on where they are filed.

In the U.S., AI patenting is concentrated amongst large companies including IBM, Microsoft, and Google. On the other hand, AI patenting in China is more distributed across government organizations, universities, and tech firms (e.g. Tencent).

In terms of focus area, China’s patents are typically related to computer vision, a field of AI that enables computers and systems to interpret visual data and inputs. Meanwhile America’s efforts are more evenly distributed across research fields.

Learn More About AI From Visual Capitalist

If you want to see more data visualizations on artificial intelligence, check out this graphic that shows which job departments will be impacted by AI the most.

-

Markets1 week ago

Markets1 week agoU.S. Debt Interest Payments Reach $1 Trillion

-

Markets2 weeks ago

Markets2 weeks agoRanked: The Most Valuable Housing Markets in America

-

Money2 weeks ago

Money2 weeks agoWhich States Have the Highest Minimum Wage in America?

-

AI2 weeks ago

AI2 weeks agoRanked: Semiconductor Companies by Industry Revenue Share

-

Markets2 weeks ago

Markets2 weeks agoRanked: The World’s Top Flight Routes, by Revenue

-

Countries2 weeks ago

Countries2 weeks agoPopulation Projections: The World’s 6 Largest Countries in 2075

-

Markets2 weeks ago

Markets2 weeks agoThe Top 10 States by Real GDP Growth in 2023

-

Money2 weeks ago

Money2 weeks agoThe Smallest Gender Wage Gaps in OECD Countries