Technology

Chart: Why Industrial Robot Sales are Sky High

Chart: Why Industrial Robot Sales are Sky High

The Chart of the Week is a weekly Visual Capitalist feature on Fridays.

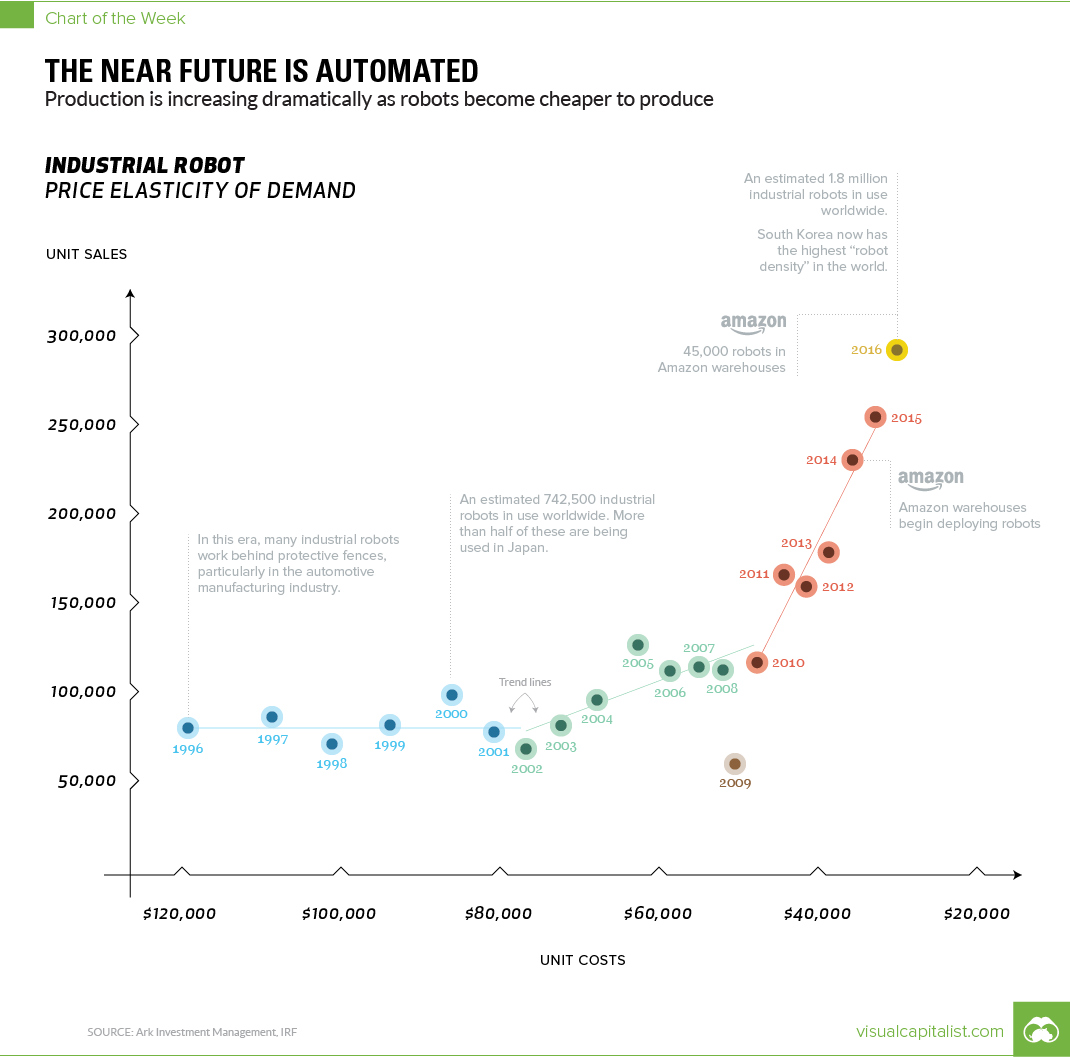

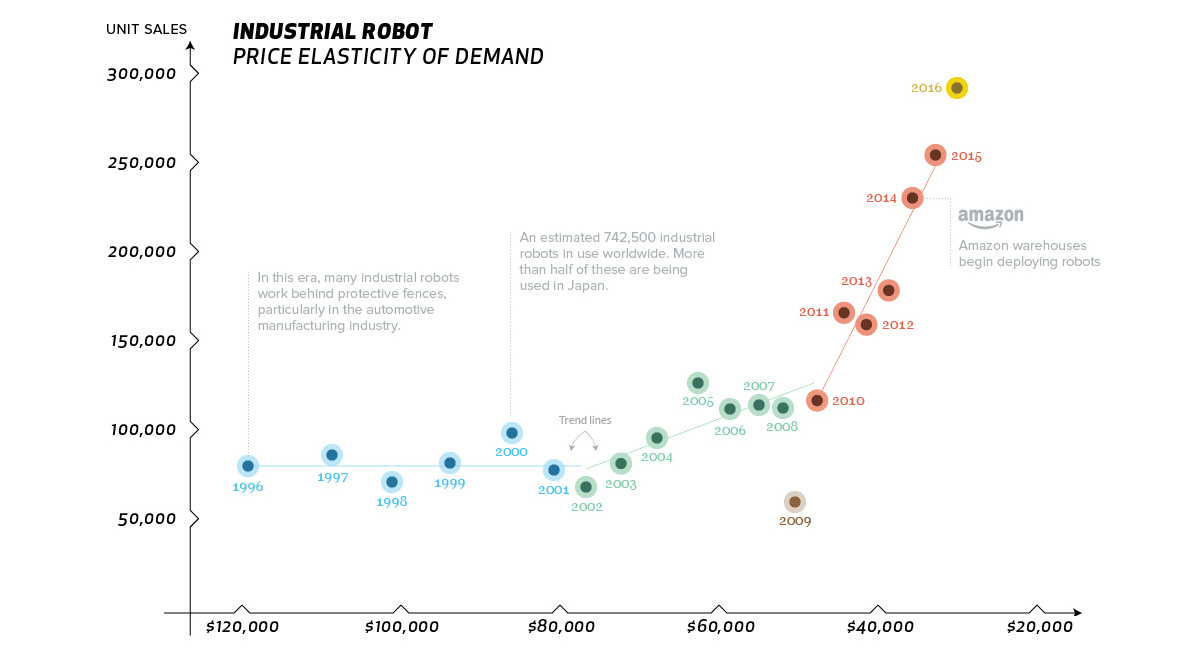

Industrial robots have come a long way since George Devol invented “Unimate” in 1961.

After pitching his idea to Joseph Engelberger at a cocktail party, the two soon saw their new creation become the first mass-produced robotic arm to be used in factory automation.

Today, this robot class is raising the bar of global manufacturing to new heights, striking a seamless mix of strength, speed, and precision. As a result, demand for industrial robots keeps growing at a robust 14% per year, setting the stage for 3.1 million industrial robots in operation globally by 2020.

Drivers of Robot Success

Why are industrial robots flying off the shelves at an unprecedented rate?

Significant factors include advancements in machine learning and computer vision, since the prospect of new functionality leads to more use cases and increased demand. In addition, the maturation of 3D printing technology and the soaring interest in collaborative robots also deserve some of the credit.

What’s interesting though, is that according to experts, the record demand for robots is actually largely in response to the notable decline in unit costs.

ARK Investment Management, a leading researcher in this market, says that industrial robot costs are expected to drop a solid 65% between 2015 and 2025. Impressively, the cost per robot will plunge from $31,000 to $11,000 over that decade of time.

A Sudden Cost Decline

Why are unit costs dropping so fast?

For ARK, such price shifts account for the workings of Wright’s Law, which states: “for every cumulative doubling in number of units produced, costs will decline by a consistent percentage”. In the field of robotics that cost decline, also known as the “learning rate”, has been around 50%.

As industrial robotic operations grow, especially in the automotive industry, the manufacturing sector continues to save millions. Meanwhile, working conditions improve as robots take mundane, repetitive, and dangerous task loads from human workers.

At present, the largest market share of industrial robots is held in the Asia-Pacific region – namely, China, Japan, Korea, and India. But as current trends suggest, these falling prices will only steer further global reach.

Technology

Ranked: Semiconductor Companies by Industry Revenue Share

Nvidia is coming for Intel’s crown. Samsung is losing ground. AI is transforming the space. We break down revenue for semiconductor companies.

Semiconductor Companies by Industry Revenue Share

This was originally posted on our Voronoi app. Download the app for free on Apple or Android and discover incredible data-driven charts from a variety of trusted sources.

Did you know that some computer chips are now retailing for the price of a new BMW?

As computers invade nearly every sphere of life, so too have the chips that power them, raising the revenues of the businesses dedicated to designing them.

But how did various chipmakers measure against each other last year?

We rank the biggest semiconductor companies by their percentage share of the industry’s revenues in 2023, using data from Omdia research.

Which Chip Company Made the Most Money in 2023?

Market leader and industry-defining veteran Intel still holds the crown for the most revenue in the sector, crossing $50 billion in 2023, or 10% of the broader industry’s topline.

All is not well at Intel, however, with the company’s stock price down over 20% year-to-date after it revealed billion-dollar losses in its foundry business.

| Rank | Company | 2023 Revenue | % of Industry Revenue |

|---|---|---|---|

| 1 | Intel | $51B | 9.4% |

| 2 | NVIDIA | $49B | 9.0% |

| 3 | Samsung Electronics | $44B | 8.1% |

| 4 | Qualcomm | $31B | 5.7% |

| 5 | Broadcom | $28B | 5.2% |

| 6 | SK Hynix | $24B | 4.4% |

| 7 | AMD | $22B | 4.1% |

| 8 | Apple | $19B | 3.4% |

| 9 | Infineon Tech | $17B | 3.2% |

| 10 | STMicroelectronics | $17B | 3.2% |

| 11 | Texas Instruments | $17B | 3.1% |

| 12 | Micron Technology | $16B | 2.9% |

| 13 | MediaTek | $14B | 2.6% |

| 14 | NXP | $13B | 2.4% |

| 15 | Analog Devices | $12B | 2.2% |

| 16 | Renesas Electronics Corporation | $11B | 1.9% |

| 17 | Sony Semiconductor Solutions Corporation | $10B | 1.9% |

| 18 | Microchip Technology | $8B | 1.5% |

| 19 | Onsemi | $8B | 1.4% |

| 20 | KIOXIA Corporation | $7B | 1.3% |

| N/A | Others | $126B | 23.2% |

| N/A | Total | $545B | 100% |

Note: Figures are rounded. Totals and percentages may not sum to 100.

Meanwhile, Nvidia is very close to overtaking Intel, after declaring $49 billion of topline revenue for 2023. This is more than double its 2022 revenue ($21 billion), increasing its share of industry revenues to 9%.

Nvidia’s meteoric rise has gotten a huge thumbs-up from investors. It became a trillion dollar stock last year, and broke the single-day gain record for market capitalization this year.

Other chipmakers haven’t been as successful. Out of the top 20 semiconductor companies by revenue, 12 did not match their 2022 revenues, including big names like Intel, Samsung, and AMD.

The Many Different Types of Chipmakers

All of these companies may belong to the same industry, but they don’t focus on the same niche.

According to Investopedia, there are four major types of chips, depending on their functionality: microprocessors, memory chips, standard chips, and complex systems on a chip.

Nvidia’s core business was once GPUs for computers (graphics processing units), but in recent years this has drastically shifted towards microprocessors for analytics and AI.

These specialized chips seem to be where the majority of growth is occurring within the sector. For example, companies that are largely in the memory segment—Samsung, SK Hynix, and Micron Technology—saw peak revenues in the mid-2010s.

-

Mining2 weeks ago

Mining2 weeks agoCharted: The Value Gap Between the Gold Price and Gold Miners

-

Real Estate1 week ago

Real Estate1 week agoRanked: The Most Valuable Housing Markets in America

-

Business1 week ago

Business1 week agoCharted: Big Four Market Share by S&P 500 Audits

-

AI1 week ago

AI1 week agoThe Stock Performance of U.S. Chipmakers So Far in 2024

-

Misc1 week ago

Misc1 week agoAlmost Every EV Stock is Down After Q1 2024

-

Money2 weeks ago

Money2 weeks agoWhere Does One U.S. Tax Dollar Go?

-

Green2 weeks ago

Green2 weeks agoRanked: Top Countries by Total Forest Loss Since 2001

-

Real Estate2 weeks ago

Real Estate2 weeks agoVisualizing America’s Shortage of Affordable Homes